Showing posts with label Inclusive Growth. Show all posts

Thursday, December 22, 2016

Monetary Policy and Inequality

Do the actions of central banks affect inequality? Leading central bankers have been discussing the issue (e.g., Yellen 2014; Bernanke 2015, Draghi 2016) but there is little consensus about the sign and magnitude of the effect. Our new paper documents how monetary policy affects income inequality in 32 advanced economies and emerging market countries over the period of 1990-2013. We find that decline of 100 basis points in the policy interest rate lowers inequality by about 1¼ percent in the short term and by about 2¼ percent in the medium term. The effect is significant and holds for different measures of inequality (Gini coefficient, top income shares and labor share of income). To identify the causal effect of monetary policy shocks on inequality, we borrow from the recent literature on fiscal policy (Auerbach and Gorodnichenko 2013) and construct unexpected changes in policy rates that are orthogonal to innovations in economic activity.

Do the actions of central banks affect inequality? Leading central bankers have been discussing the issue (e.g., Yellen 2014; Bernanke 2015, Draghi 2016) but there is little consensus about the sign and magnitude of the effect. Our new paper documents how monetary policy affects income inequality in 32 advanced economies and emerging market countries over the period of 1990-2013. We find that decline of 100 basis points in the policy interest rate lowers inequality by about 1¼ percent in the short term and by about 2¼ percent in the medium term.

Posted by at 4:55 PM

Labels: Inclusive Growth

Tuesday, December 20, 2016

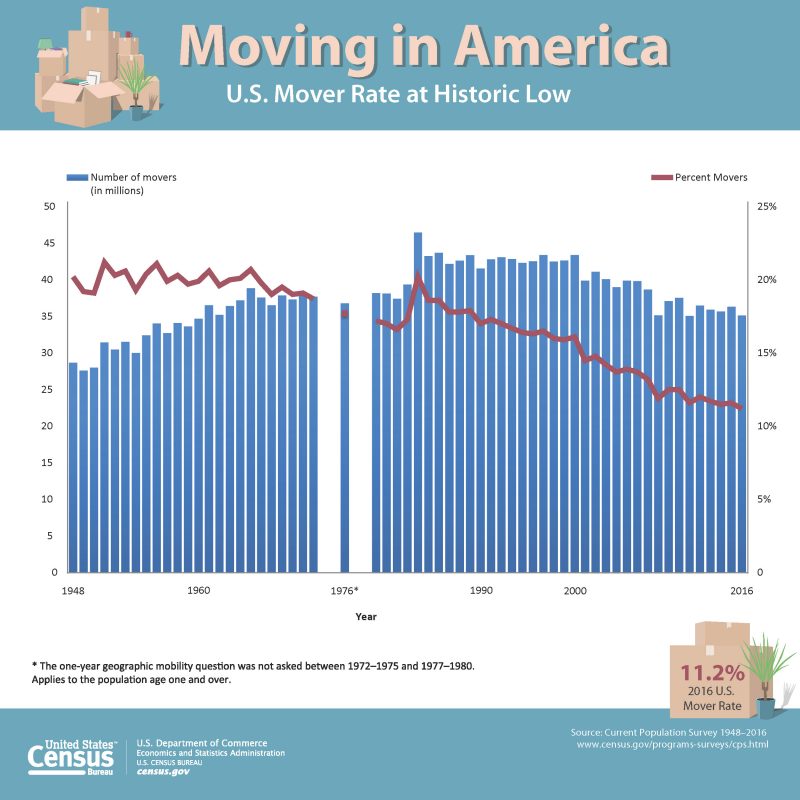

(Not) On The Road Again: Americans Are Moving Less

A nice update by Timothy Taylor on declining labor mobility in the United States and the possible reasons, a topic I have written on as well.

Posted by at 8:44 AM

Labels: Inclusive Growth

Tuesday, December 13, 2016

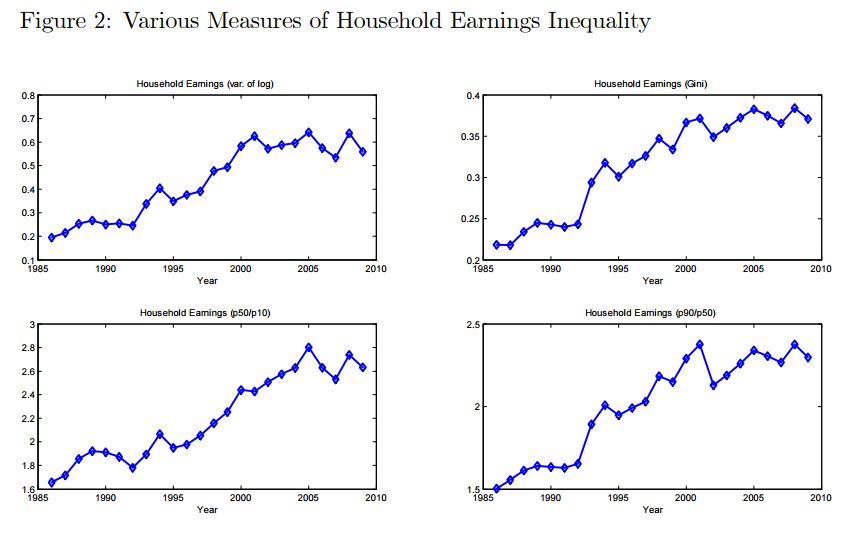

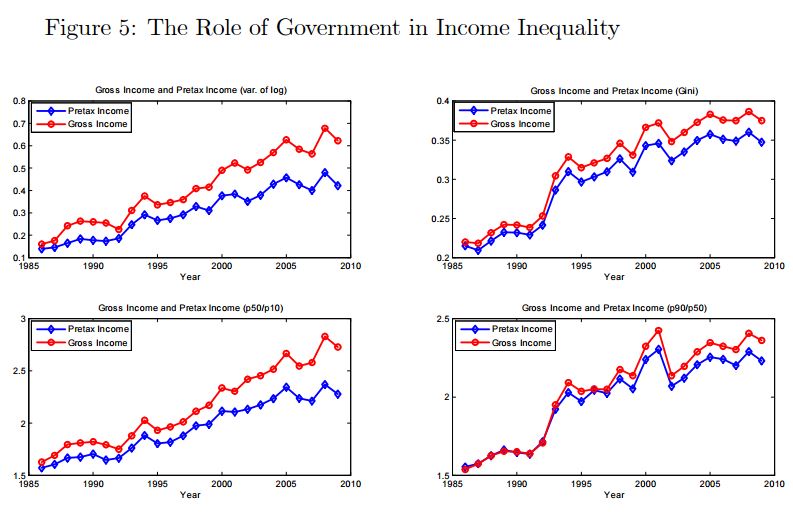

A Tale of Transition : An Empirical Analysis of Economic Inequality in Urban China

A new IMF working paper is the first comprehensive empirical study of earnings, income, and consumption inequality in urban China from 1986 to 2009, using unique micro-level data from the Urban Household Survey (UHS). The paper documents a drastic increase in economic inequality for the sample period. The paper finds that consumption inequality closely tracks income inequality, both over time and over the life cycle. The paper believes that the main driver of this co-movement could be a dramatic increase in noninsurable idiosyncratic permanent income shocks after the early 1990s, associated with the economic transition in urban China.

A new IMF working paper is the first comprehensive empirical study of earnings, income, and consumption inequality in urban China from 1986 to 2009, using unique micro-level data from the Urban Household Survey (UHS). The paper documents a drastic increase in economic inequality for the sample period. The paper finds that consumption inequality closely tracks income inequality, both over time and over the life cycle. The paper believes that the main driver of this co-movement could be a dramatic increase in noninsurable idiosyncratic permanent income shocks after the early 1990s,

Posted by at 3:10 PM

Labels: Inclusive Growth

Monday, December 12, 2016

The IMF is Not Asking Greece for More Austerity

Greece is once again in the headlines as discussions for the second review of its European Stability Mechanism (ESM) program are gaining pace. Unfortunately, the discussions have also spurred some misinformation about the role and the views of the IMF. Above all, the IMF is being criticized for demanding more fiscal austerity, in particular for making this a condition for urgently needed debt relief. This is not true, and clarifications are in order.

The IMF is not demanding more austerity. On the contrary, when the Greek Government agreed with its European partners in the context of the ESM program to push the Greek economy to a primary fiscal surplus of 3.5 percent by 2018, we warned that this would generate a degree of austerity that could prevent the nascent recovery from taking hold. We projected that the measures in the ESM program will deliver a surplus of only 1.5 percent of GDP, and said this would be enough for us to support a program. We did not call for additional measures to achieve a higher surplus. But contrary to our advice, the Greek Government agreed with the European institutions to temporarily compress spending further if needed to ensure that the surplus would reach 3.5 percent of GDP.

We have not changed our view that Greece does not need more austerity at this time. Claiming that it is the IMF who is calling for this turns the truth upside down.

Continue reading here.

Greece is once again in the headlines as discussions for the second review of its European Stability Mechanism (ESM) program are gaining pace. Unfortunately, the discussions have also spurred some misinformation about the role and the views of the IMF. Above all, the IMF is being criticized for demanding more fiscal austerity, in particular for making this a condition for urgently needed debt relief. This is not true,

Posted by at 5:07 PM

Labels: Inclusive Growth

Tuesday, December 6, 2016

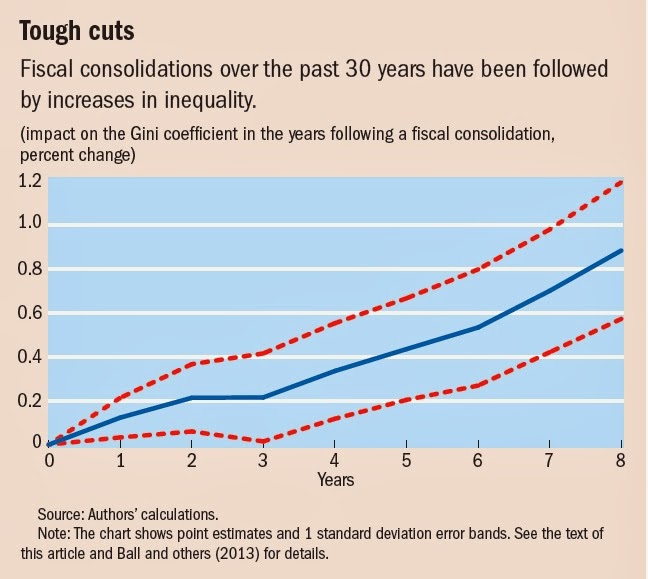

Austerity and Inequality: New Evidence from the IMF

The IMF Economic Review just published a paper that looks into the “distributional consequences of fiscal austerity measures” for 17 OECD countries over the last 30 years. This new paper adds to the stock of IMF papers on the impacts of fiscal consolidation of inequality. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits; and the long-term unemployed are affected more than short-term unemployed.

2) The Distributional Effects of Fiscal Consolidation: A wonkish version of the “Painful Medicine” article, with the additional result that, between 1978 and 2009, fiscal consolidations in advanced economies increased the Gini measure on income inequality.

3) Distributional Consequences of Fiscal Consolidation and the Role of Fiscal Policy: In addition to confirming the results in the previous papers, this paper brings in evidence from emerging markets. It also discusses how policies can be designed to mitigate the impacts of fiscal policy on inequality.

4) Who Let the Gini Out?: A (non-wonkish) summary of some of the previous papers.

5) Fiscal Policy and Inequality: A key finding of the paper is that fiscal consolidations during the Great Recession did not lead to increases in inequality.

6) Distributional Consequences of Fiscal Adjustments: What Do the Data Say?: “The paper shows that fiscal adjustments are likely to raise inequality through various channels including their effects on unemployment. Spending-based adjustments tend to worsen inequality more significantly, relative to tax-based adjustments. The composition of austerity measures also matters: progressive taxation and targeted social benefits and subsidies introduced in the context of a broader decline in spending can help offset some of the adverse distributional impact of fiscal adjustments.”

The IMF Economic Review just published a paper that looks into the “distributional consequences of fiscal austerity measures” for 17 OECD countries over the last 30 years. This new paper adds to the stock of IMF papers on the impacts of fiscal consolidation of inequality. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits;

Posted by at 10:22 AM

Labels: Inclusive Growth

Subscribe to: Posts