Showing posts with label Inclusive Growth. Show all posts

Wednesday, September 27, 2017

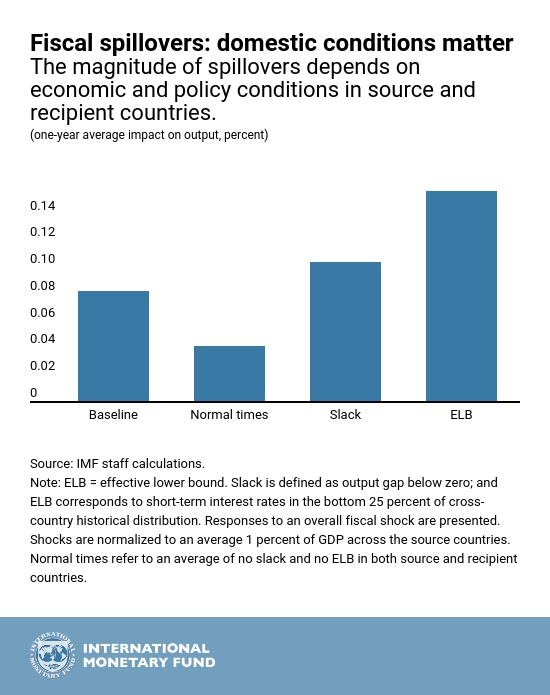

Better thy Neighbor? Cross-border Effects of Fiscal Actions

From a new IMF blog: “Our analysis provides information on potential cross-country effects from domestic fiscal policies. For example, fiscal stimulus in Germany through higher public investment would generate meaningful spillovers to neighboring countries in Europe where output remains below potential and interest rates are exceptionally low. Spending on public investment is also likely to produce greater cross-border dividends than tax cuts. Conversely, given cyclical conditions in the United States, a U.S. fiscal stimulus would likely have modest spillovers, especially if implemented through tax policy measures.”

Continue reading here.

From a new IMF blog: “Our analysis provides information on potential cross-country effects from domestic fiscal policies. For example, fiscal stimulus in Germany through higher public investment would generate meaningful spillovers to neighboring countries in Europe where output remains below potential and interest rates are exceptionally low. Spending on public investment is also likely to produce greater cross-border dividends than tax cuts. Conversely, given cyclical conditions in the United States, a U.S.

Posted by at 10:46 AM

Labels: Inclusive Growth

Thursday, September 21, 2017

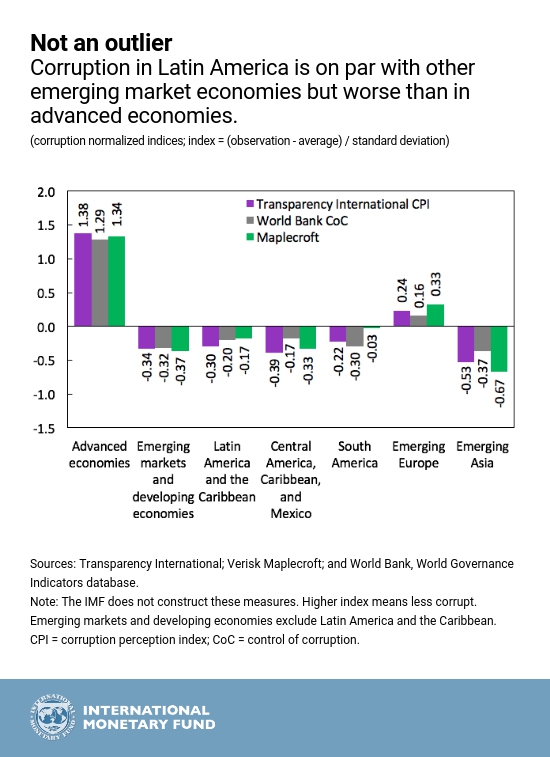

Corruption in Latin America: Taking Stock

A new IMF blog by David Lipton, Alejandro Werner, and Carlos Gonçalves says that “Corruption continues to make headlines in Latin America. From a scheme to shelter assets leaked by documents in Panama, to the Petrobras and Odebrecht scandals that have spread beyond Brazil, to eight former Mexican state governors facing charges or being convicted, the region has seen its share of economic and political fallout from corruption. Latin Americans are showing increasing signs of discontent and demanding that their governments tackle corruption more aggressively.”

Continue reading here.

A new IMF blog by David Lipton, Alejandro Werner, and Carlos Gonçalves says that “Corruption continues to make headlines in Latin America. From a scheme to shelter assets leaked by documents in Panama, to the Petrobras and Odebrecht scandals that have spread beyond Brazil, to eight former Mexican state governors facing charges or being convicted, the region has seen its share of economic and political fallout from corruption.

Posted by at 1:05 PM

Labels: Inclusive Growth

Growth That Reaches Everyone: Facts, Factors, Tools

A new IMF blog says that “Over the past few decades, growth has raised living standards and provided job opportunities, lifting millions out of extreme poverty. But, we have also seen a flip side. Inequality has risen in several advanced economies and remains stubbornly high in many that are still developing. This worries policymakers everywhere for good reason. Research at the IMF and elsewhere makes it clear that persistent lack of inclusion—defined as broadly shared benefits and opportunities for economic growth—can fray social cohesion and undermine the sustainability of growth itself.”

Continue reading here.

A new IMF blog says that “Over the past few decades, growth has raised living standards and provided job opportunities, lifting millions out of extreme poverty. But, we have also seen a flip side. Inequality has risen in several advanced economies and remains stubbornly high in many that are still developing. This worries policymakers everywhere for good reason. Research at the IMF and elsewhere makes it clear that persistent lack of inclusion—defined as broadly shared benefits and opportunities for economic growth—can fray social cohesion and undermine the sustainability of growth itself.”

Posted by at 10:03 AM

Labels: Inclusive Growth

Monday, September 18, 2017

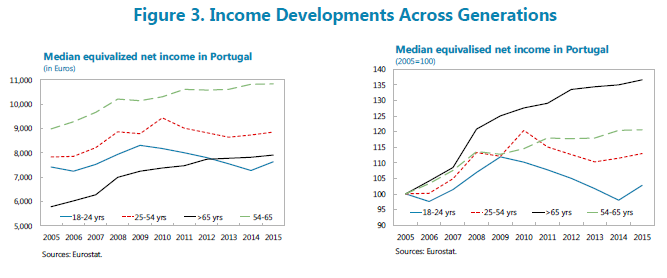

The Youth in Portugal through the Crisis

A new IMF report says that “Inequality and poverty in Europe during the financial crisis has received widespread attention, but somewhat less discussed has been the social impact of the crisis across generations. In a context where Portugal’s convergence toward lower European poverty and inequality standards has stalled over the last five years, the youth (aged 15-24 years) were especially affected by the downturn and adverse labor market developments. Their income has not yet fully recovered to pre-crisis levels, and their risk of poverty is the highest of all age groups. The youth are disproportionally unemployed or in precarious forms of employment in the context of strong market duality. The social security system has better protected the elderly from the impact of the crisis, with the youth less well covered against unemployment and poverty risks. Going forward, policies should focus on further reducing labor market duality to improve job prospects for young adults, and rebalancing fiscal redistribution to combat poverty in young adults.”

A new IMF report says that “Inequality and poverty in Europe during the financial crisis has received widespread attention, but somewhat less discussed has been the social impact of the crisis across generations. In a context where Portugal’s convergence toward lower European poverty and inequality standards has stalled over the last five years, the youth (aged 15-24 years) were especially affected by the downturn and adverse labor market developments. Their income has not yet fully recovered to pre-crisis levels,

Posted by at 2:28 PM

Labels: Inclusive Growth

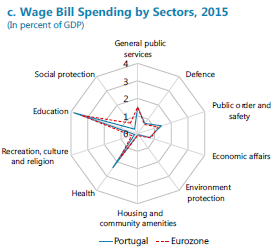

The Public Sector Wage Bill in Portugal

A new IMF report says that “Portugal achieved an impressive consolidation of its public wage bill during the adjustment program, with large efficiency gains and savings generated in the education and health sectors. As in many European countries, these efforts relied on blunt but quick measures such as across-the-board attrition and temporary wage cuts, which could not be sustained over the medium-term. From 2015, these measures were reversed or unwound, and structural reforms lost momentum. Going forward, Portugal projects a large reduction in the wage bill from 2017-2021 (-1.3 percentage points of GDP) that needs to be supported by specific reforms. This will prove challenging, as wage and public employment policies show evidence of procyclicality. To prevent adverse impact on public service provision, targeted reduction in public employment will require adjusting employment levels across sectors. Finally, containing public compensation will require structural wage measures to gradually address large public wage premium relative to the private sector.”

A new IMF report says that “Portugal achieved an impressive consolidation of its public wage bill during the adjustment program, with large efficiency gains and savings generated in the education and health sectors. As in many European countries, these efforts relied on blunt but quick measures such as across-the-board attrition and temporary wage cuts, which could not be sustained over the medium-term. From 2015, these measures were reversed or unwound, and structural reforms lost momentum.

Posted by at 2:25 PM

Labels: Inclusive Growth

Subscribe to: Posts