Showing posts with label Inclusive Growth. Show all posts

Friday, March 30, 2018

Fostering Incentives for Women to Work to Promote Long-Term Growth in Iran

From a new IMF report on Iran’s female labor force participation:

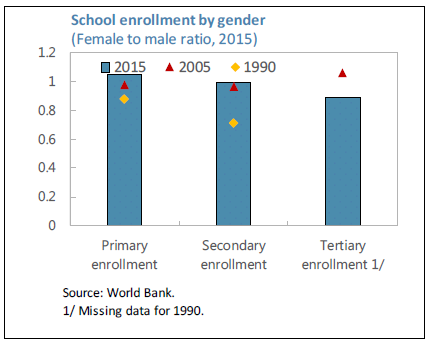

“Iran has made tremendous strides in eliminating gender gaps in education and health indicators. For about a decade now, there has been virtually no gap between male and female enrollment in primary and secondary education. The gender gap in tertiary education enrollment is small and, in some fields of studies such as engineering and science, women are now in the majority (IMF, 2016a). Years of schooling attained by women have expanded by 40 percent within in one generation (World Bank, 2016a) to reach an average of 9 years. The fertility rate in Iran has fallen sharply in the last 30 years and has been below two children per woman since the 2000s, and on par with the average of advanced economies. Life expectancy at birth for women is higher than men by 2 years (76.7 versus 74.5 years).

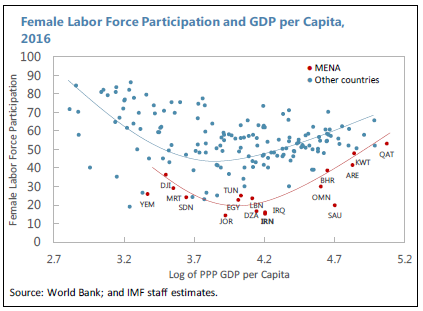

Despite these laudable achievements, female participation in the labor force is low. Female labor force participation (FLFP) was 16.2 percent in 2016, lower than countries with similar income per capita, including within the MENAP region. Some 83.8 percent of all females over the age of 10 are inactive and out of the labor force—the fourth highest rate in the world—3.2 percent of women were unemployed, and only 13 percent were working. Women represent 13.3 percent of legislators, senior officials and managers and hold 3.1 percent of seats in the parliament. Iran has two Vice Presidents who are women.

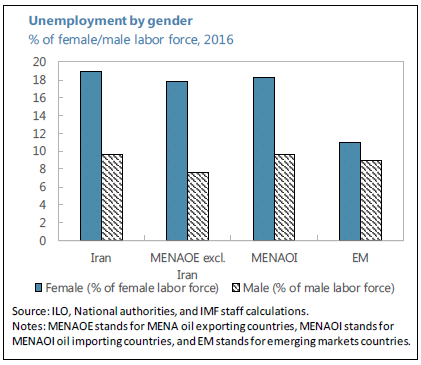

Once in the labor force, women in Iran are also more likely to be unemployed. In 2016, the female unemployment rate of 18.9 percent was twice as high as males. Although the average male and female unemployment rates are broadly in line with the MENAP region average, the female unemployment rate exceeds the emerging market average (EM) of 11 percent. Furthermore, a woman in Iran is likely to remain unemployed longer. While 30 percent of men remain unemployed for less than 3 months (versus only 11 percent of women), almost 48 percent of women remain unemployed for more than 19 months (versus only 28 percent of men).

Iran’s highly educated female population represents an untapped source growth and productivity gains. Increasing FLFP can significantly boost GDP, productivity, tax collections and alleviate the expected burden of aging (see IMF, 2016b). Section B presents several factors contributing to the low rate of FLFP in Iran. Section C analyzes the macroeconomic impact of reforms to reduce gender gaps in the labor market using an overlapping generations model. It examines the macroeconomic impact of three reforms: reducing the gender wage gap, reducing the obstacles for women to join the labor force, and subsidizing childcare costs to low- and mid-income female workers in the formal sector.”

Continue reading here.

From a new IMF report on Iran’s female labor force participation:

“Iran has made tremendous strides in eliminating gender gaps in education and health indicators. For about a decade now, there has been virtually no gap between male and female enrollment in primary and secondary education. The gender gap in tertiary education enrollment is small and, in some fields of studies such as engineering and science, women are now in the majority (IMF,

Posted by at 11:11 AM

Labels: Inclusive Growth

Thursday, March 29, 2018

Monetary Policy, Labour Income, and Inequality

A new paper from the Bank of England finds that in UK, the impact of monetary policy on inequality depends on existing difference in income and wealth.“[…] younger households are estimated to have benefited most from higher income in cash terms, while older households gained more from higher wealth.”

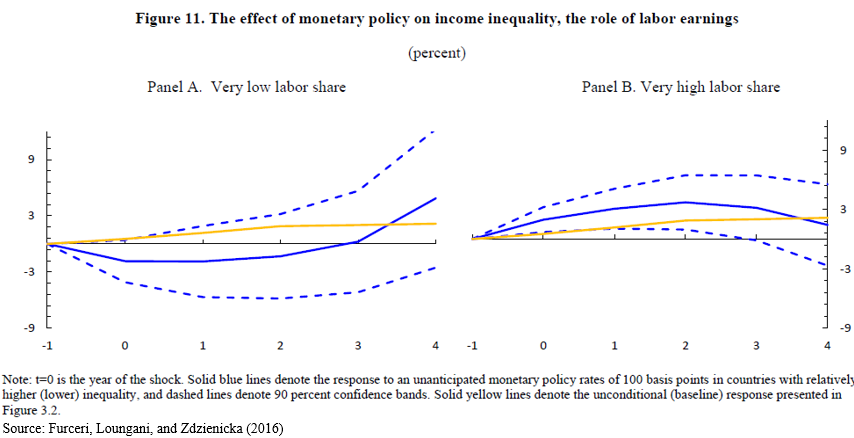

The paper notes that “Furceri, Loungani, and Zdzienicka (2016) emphasise the importance of heterogeneity in the response of labour income to monetary policy as a key channel, noting evidence that those at the bottom of the income distribution are most affected by changes in economic activity.” Continue reading here.

See my previous post on monetary policy and inequality here. The Furceri, Loungani, and Zdzienicka (2016) paper is available here.

A new paper from the Bank of England finds that in UK, the impact of monetary policy on inequality depends on existing difference in income and wealth.“[…] younger households are estimated to have benefited most from higher income in cash terms, while older households gained more from higher wealth.”

The paper notes that “Furceri, Loungani, and Zdzienicka (2016) emphasise the importance of heterogeneity in the response of labour income to monetary policy as a key channel,

Posted by at 2:22 PM

Labels: Inclusive Growth

Tuesday, March 27, 2018

The Gains from (Services) Trade

A new paper from the Bank of England says that “liberalising services trade, levelling up to the liberalisation seen in goods trade, could reduce excess global imbalances by around 40%. […] The potential rewards [of services trade liberalisation] are much broader. The great prize could be reinvigorating global growth.”

The paper notes that “seminal work by Baumol (1967) underpinned the ‘classical view’ of the contribution of services to growth. This view was unambiguously negative, indicating that services were largely non-tradable and exhibited little scope for productivity improvements. But services have changed significantly since then and evidence today suggests that services are widely traded across borders (Loungani et al (2017)) and that, when services productivity is correctly measured, historical services productivity growth has been as strong as manufacturing (Young (2014)). Many studies confirm positive linkages between service sector liberalisation and economic growth. There are three aspects to this: direct benefits for the services sector, downstream benefits for production in other sectors which use services, and the potential distribution benefits from services growth.” Continue reading here.

The Loungani et al paper and our new data set on services trade are available here.

Source: Loungani et al (2017).

A new paper from the Bank of England says that “liberalising services trade, levelling up to the liberalisation seen in goods trade, could reduce excess global imbalances by around 40%. […] The potential rewards [of services trade liberalisation] are much broader. The great prize could be reinvigorating global growth.”

The paper notes that “seminal work by Baumol (1967) underpinned the ‘classical view’ of the contribution of services to growth. This view was unambiguously negative,

Posted by at 8:25 PM

Labels: Inclusive Growth

Wednesday, March 14, 2018

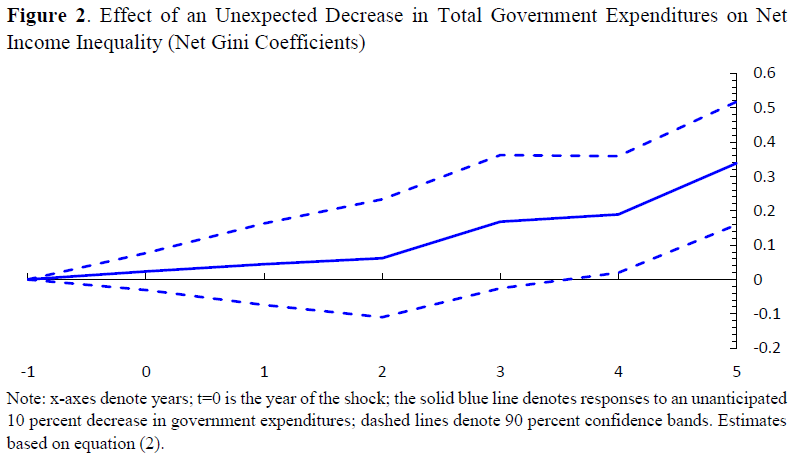

The Distributional Effects of Government Spending Shocks in Developing Economies

From my latest IMF working paper with Davide Furceri, Jun Ge, and Giovanni Melina:

“We construct unanticipated government spending shocks for 103 developing countries from 1990 to 2015 and study their effects on income distribution. We find that unanticipated fiscal consolidations lead to a long-lasting increase in income inequality, while fiscal expansions lower inequality. The results are robust to several measures of income distribution and size of the fiscal shocks, to an alternative identification strategy, across expansions and recessions and across country groups (low-income countries versus emerging markets). An additional contribution of the paper is the computation of the medium-term inequality multiplier. This is on average about 1 in our sample, meaning that a cumulative decrease in government spending of 1 percent of GDP over 5 years is associated with a cumulative increase in the Gini coefficient over the same period of about 1 percentage point. The multiplier is larger for total government expenditure than for public investment and consumption (with the former having larger effect), likely due to the redistributive role of transfers. Finally, we find that (unanticipated) fiscal consolidations lead to an increase in poverty.”

From my latest IMF working paper with Davide Furceri, Jun Ge, and Giovanni Melina:

“We construct unanticipated government spending shocks for 103 developing countries from 1990 to 2015 and study their effects on income distribution. We find that unanticipated fiscal consolidations lead to a long-lasting increase in income inequality, while fiscal expansions lower inequality. The results are robust to several measures of income distribution and size of the fiscal shocks,

Posted by at 4:52 PM

Labels: Inclusive Growth

Tuesday, March 13, 2018

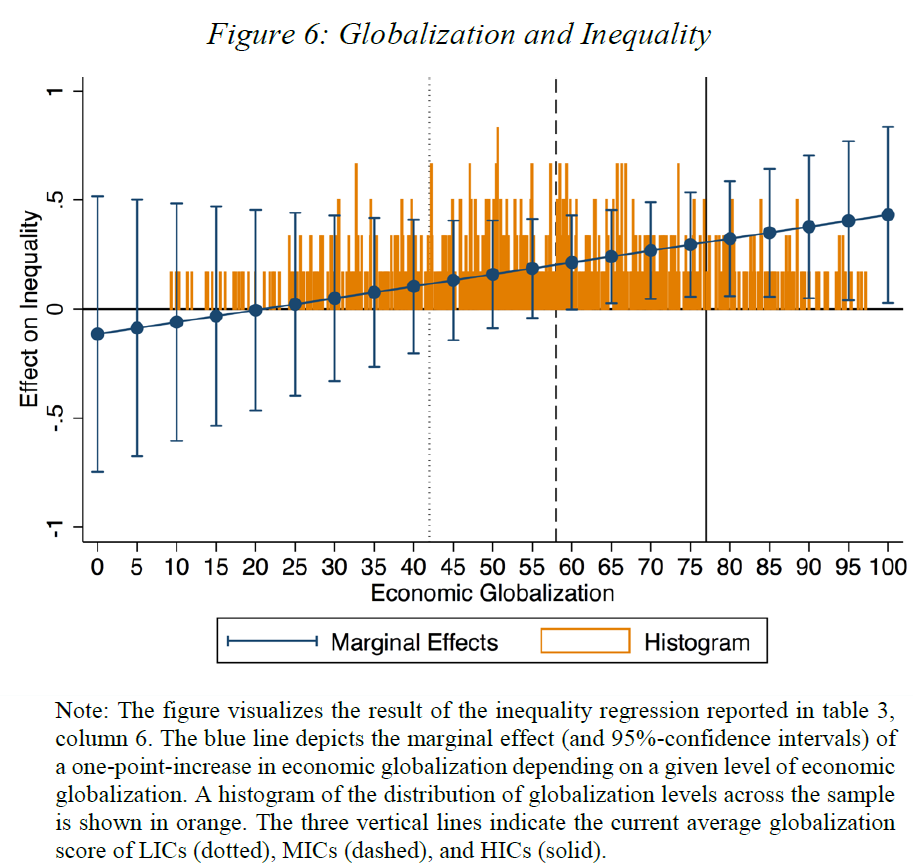

The Distribution of Gains from Globalization

From a new IMF working paper:

“We study economic globalization as a multidimensional process and investigate its effect on incomes. In a panel of 147 countries during 1970-2014, we apply a new instrumental variable, exploiting globalization’s geographically diffusive character, and find differential gains from globalization both across and within countries: Income gains are substantial for countries at early and medium stages of the globalization process, but the marginal returns diminish as globalization rises, eventually becoming insignificant. Within countries, these gains are concentrated at the top of national income distributions, resulting in rising inequality. We find that domestic policies can mitigate the adverse distributional effects of globalization.”

From a new IMF working paper:

“We study economic globalization as a multidimensional process and investigate its effect on incomes. In a panel of 147 countries during 1970-2014, we apply a new instrumental variable, exploiting globalization’s geographically diffusive character, and find differential gains from globalization both across and within countries: Income gains are substantial for countries at early and medium stages of the globalization process, but the marginal returns diminish as globalization rises,

Posted by at 8:12 PM

Labels: Inclusive Growth

Subscribe to: Posts