Showing posts with label Inclusive Growth. Show all posts

Tuesday, May 22, 2018

Yes, we should fear the robot revolution

From a new IMF working paper by Andrew Berg, Edward Buffie, and Luis-Felipe Zanna:

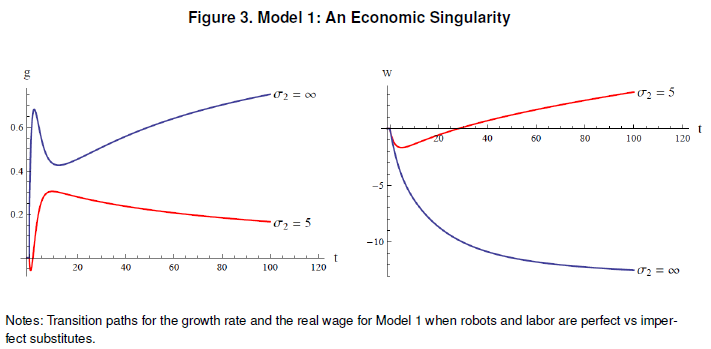

“Advances in artificial intelligence and robotics may be leading to a new industrial revolution. This paper presents a model with the minimum necessary features to analyze the implications for inequality and output. Two assumptions are key: “robot” capital is distinct from traditional capital in its degree of substitutability with human labor; and only capitalists and skilled workers save. We analyze a range of variants that reflect widely different views of how automation may transform the labor market. Our main results are surprisingly robust: automation is good for growth and bad for equality; in the benchmark model real wages fall in the short run and eventually rise, but “eventually” can easily take generations.”

“Figure 3 plots the transition paths [when robots and labor are perfect vs. imperfect substitutes, when all other parameters take their base case bales.] Perfect substitution of robot for human labor delivers perpetual growth. But the rich become richer and the poor poorer with every passing year. In the long run, the real wage decreases 13.4% while capitalists’ income rises without limit.”

From a new IMF working paper by Andrew Berg, Edward Buffie, and Luis-Felipe Zanna:

“Advances in artificial intelligence and robotics may be leading to a new industrial revolution. This paper presents a model with the minimum necessary features to analyze the implications for inequality and output. Two assumptions are key: “robot” capital is distinct from traditional capital in its degree of substitutability with human labor; and only capitalists and skilled workers save.

Posted by at 10:59 AM

Labels: Inclusive Growth

Labor Force Participation in U.S. States and Metropolitan Areas

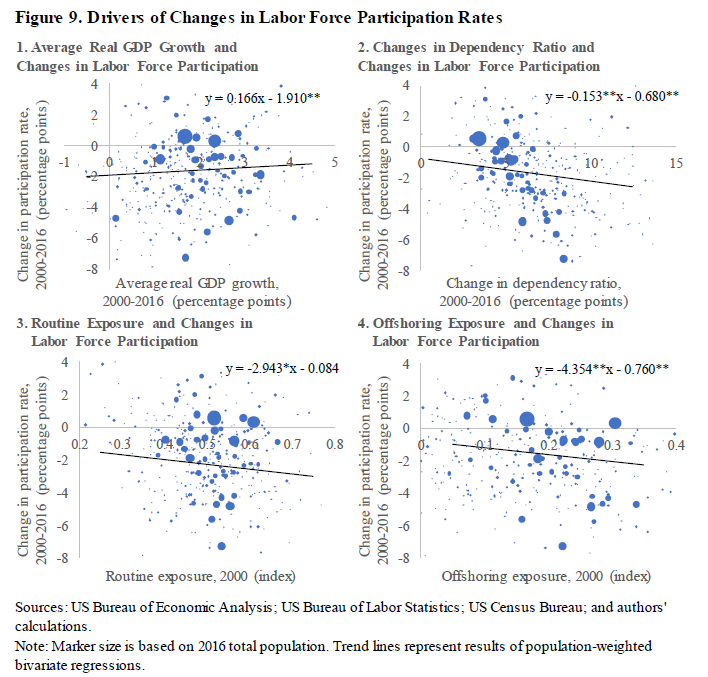

A new IMF working paper “explores regional differences to shed light on drivers of participation rates at the state and metropolitan area levels. It documents a broad-based decline, especially pronounced outside metropolitan areas. Using novel measures of local vulnerability to trade and technology it finds that metropolitan areas with higher exposures to routinization and offshoring experienced larger drops in participation in 2000-2016. Thus, areas with different occupational mixes can experience divergent labor market trajectories as a result of trade and technology.”

A new IMF working paper “explores regional differences to shed light on drivers of participation rates at the state and metropolitan area levels. It documents a broad-based decline, especially pronounced outside metropolitan areas. Using novel measures of local vulnerability to trade and technology it finds that metropolitan areas with higher exposures to routinization and offshoring experienced larger drops in participation in 2000-2016. Thus, areas with different occupational mixes can experience divergent labor market trajectories as a result of trade and technology.”

Posted by at 10:40 AM

Labels: Inclusive Growth

Uber and the labor market

A new report by Lawrence Mishel says that “Uber, and gig work more broadly, [does not] represent the future of work.” “Uber drivers earn low wages and compensation and the total hours and compensation in the gig economy represent a very small share of total hours and compensation in the overall economy. These findings—and the fact that many Uber and other workers who provide personal services via a digital platform do so on a part-time basis primarily as a way to earn supplementary income—argue for a change in perspective. There has been much hype around Uber and the gig economy. But in our assessment, in any conference on the future of work, Uber and the gig economy deserve at most a workshop, not a plenary.”

A new report by Lawrence Mishel says that “Uber, and gig work more broadly, [does not] represent the future of work.” “Uber drivers earn low wages and compensation and the total hours and compensation in the gig economy represent a very small share of total hours and compensation in the overall economy. These findings—and the fact that many Uber and other workers who provide personal services via a digital platform do so on a part-time basis primarily as a way to earn supplementary income—argue for a change in perspective.

Posted by at 10:35 AM

Labels: Inclusive Growth

Thursday, May 17, 2018

IEO Releases an Update to its 2007 evaluation of Structural Conditionality in IMF-Supported Programs

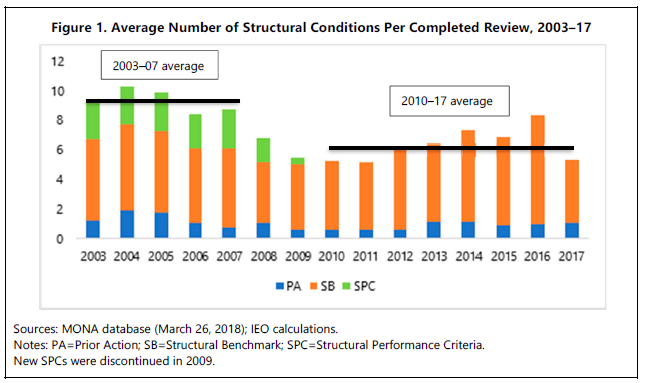

The IEO just released an Evaluation Update Report revisiting its 2007 evaluation of Structural Conditionality in IMF-Supported Programs. The report was published along with a statement by the Managing Director.

“The evaluation found that, notwithstanding the streamlining initiative launched in 2000, structural conditionality was still used extensively and program documents were not sufficiently clear about the criticality of structural conditions. Moreover, the report concluded that most structural conditions had little structural depth, only about half were implemented on time, and compliance was only weakly correlated with subsequent progress in structural reforms.”

“Following the evaluation, use of IMF lending surged in the context of the global financial crisis in 2008 and the euro area crisis in 2010. Use of structural conditionality in euro area crisis programs raised issues related to working with regional partners. Fund program design and implementation over this period was informed by revisions to staff guidance in 2008, 2010, and 2014, and the Review of Conditionality completed in 2012.”

The IEO just released an Evaluation Update Report revisiting its 2007 evaluation of Structural Conditionality in IMF-Supported Programs. The report was published along with a statement by the Managing Director.

“The evaluation found that, notwithstanding the streamlining initiative launched in 2000, structural conditionality was still used extensively and program documents were not sufficiently clear about the criticality of structural conditions. Moreover, the report concluded that most structural conditions had little structural depth,

Posted by at 10:54 AM

Labels: Inclusive Growth

Tuesday, May 15, 2018

Poverty and inequality in Latin America

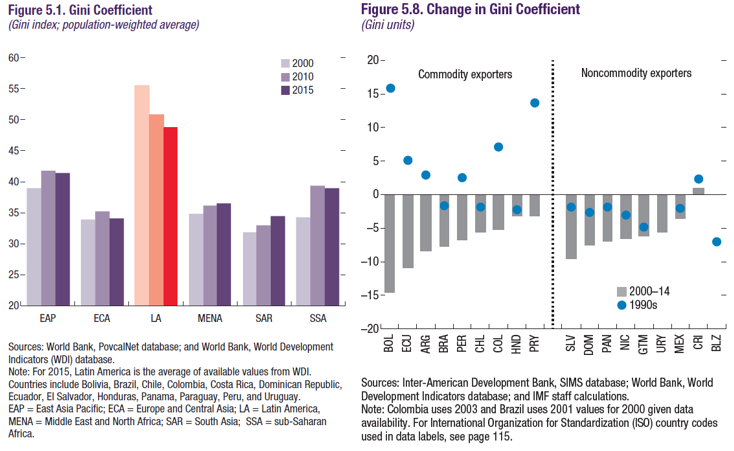

The new IMF Regional Economic Outlook says that “Latin America has made impressive progress in reducing inequality and poverty since the turn of the century, although it remains the most unequal region in the world. The declines in inequality and poverty were particularly pronounced for commodity exporters during the commodity boom. Much of the progress reflected real labor income gains for lower-skilled workers, especially in services, with a smaller but positive role for government transfers. With the commodity boom over, a tighter fiscal envelope, and poverty rates already edging up in some countries, policies will have to be carefully recalibrated to sustain social progress. Increasing personal income tax revenues while rebalancing spending could help maintain key social transfers and infrastructure spending. Better targeting of social transfers and reforming decentralization frameworks also have an important role to play.”

The new IMF Regional Economic Outlook says that “Latin America has made impressive progress in reducing inequality and poverty since the turn of the century, although it remains the most unequal region in the world. The declines in inequality and poverty were particularly pronounced for commodity exporters during the commodity boom. Much of the progress reflected real labor income gains for lower-skilled workers, especially in services, with a smaller but positive role for government transfers.

Posted by at 3:16 PM

Labels: Inclusive Growth

Subscribe to: Posts