Showing posts with label Inclusive Growth. Show all posts

Thursday, June 14, 2018

Labor Market Implications of the Exposure to Routinization

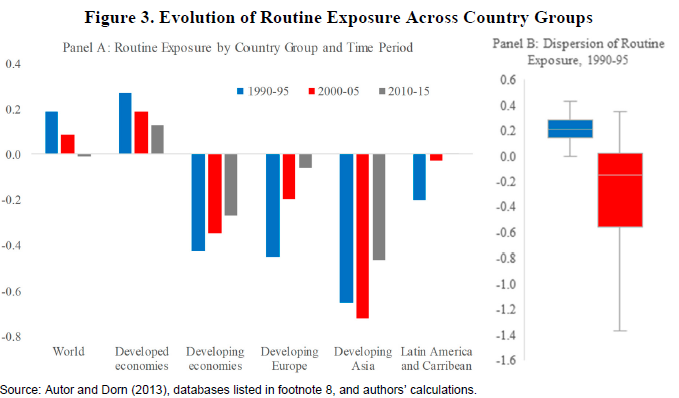

A new IMF working paper proposes “a measure of the exposure to routinization—that is, the risk of the displacement of labor by information technology—and assemble several facts that link the exposure to routinization with the prospects of polarization”, and finds that “(1) developing economies are significantly less exposed to routinization than their developed counterparts; (2) the initial exposure to routinization is a strong predictor of the long-run exposure; and (3) among countries with high initial exposures to routinization, polarization dynamics have been strong and subsequent exposures have fallen; while among those with low initial exposure, the globalization of trade and structural transformation have prevailed and routine exposures have risen.

A new IMF working paper proposes “a measure of the exposure to routinization—that is, the risk of the displacement of labor by information technology—and assemble several facts that link the exposure to routinization with the prospects of polarization”, and finds that “(1) developing economies are significantly less exposed to routinization than their developed counterparts; (2) the initial exposure to routinization is a strong predictor of the long-run exposure; and (3) among countries with high initial exposures to routinization,

Posted by at 9:47 AM

Labels: Inclusive Growth

Wednesday, June 13, 2018

IMF on Operationalizing Gender Issues

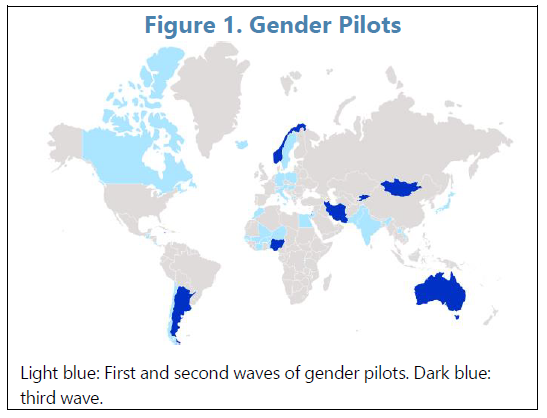

A new IMF report provides a thorough overview of practices and resources on operationalizing gender issues:

“Reducing gender gaps can have important economic benefits. Gender gaps remain significant on a global scale, both with respect to opportunities and outcomes. For example, gender-based legal restrictions in many parts of the world, as well as barriers in access to education, healthcare, and financial services, prevent women from fully participating in the economy. In turn, labor force participation rates are lower among women than men. Gender equality can play an important role in promoting economic stability by boosting economic productivity and growth, enhancing economic resilience, and reducing income inequality.

The Fund has begun operationalizing gender issues in its work. Staff has contributed to the economic literature through country-level and cross-country analytical studies, confirming the macro-criticality of gender issues in a broad set of circumstances. Gender issues are also increasingly becoming an integral part of capacity development though technical assistance and training. And in country work, two waves of gender pilots have been completed—encompassing both surveillance and Fund-supported programs and covering all regions of the world and all levels of income—and a third wave is under way.”

A new IMF report provides a thorough overview of practices and resources on operationalizing gender issues:

“Reducing gender gaps can have important economic benefits. Gender gaps remain significant on a global scale, both with respect to opportunities and outcomes. For example, gender-based legal restrictions in many parts of the world, as well as barriers in access to education, healthcare, and financial services, prevent women from fully participating in the economy. In turn,

Posted by at 3:48 PM

Labels: Inclusive Growth

IMF on Operationalizing Inequality Issues

A new IMF report provides a thorough overview of practices and resources on operationalizing inequality issues:

“Economic inclusion is the broad sharing of the benefits of, and the opportunities to participate in, economic growth. It embodies equitable outcomes related to financial well-being as well as opportunities in access to markets and resources, and protects the vulnerable.

Economic inclusion is a high priority issue for the IMF. High inequality is negatively associated with macroeconomic stability and sustainable growth—core to the Fund’s mandate in promoting systemic, balance of payments, and domestic stability. Some macroeconomic policies and reforms may have adverse distributional implications, which in turn can undermine public support for reforms. And, interest in distributional issues and inequality has grown among the membership, increasing the demand for the Fund to work in these areas. While the IMF has long recognized the importance of inequality issues, it has adopted in the recent years a more systematic and structured approach. In this regard, a pilot initiative on inequality was launched in 2015, with the third wave of countries currently participating. Once this wave is concluded, staff proposes to incorporate the analysis of inequality-related issues into broader country work where relevant.”

Several of my papers are noted:

- Furceri, Loungani, and Zdzienicka (2016) study the effects of monetary policy shocks on inequality.

- Furceri and Loungani (2015) investigate the association between capital account liberalization and inequality.

- Ball, Furceri, Leigh, and Loungani (2013) examine the distributional effects of fiscal consolidation.

A new IMF report provides a thorough overview of practices and resources on operationalizing inequality issues:

“Economic inclusion is the broad sharing of the benefits of, and the opportunities to participate in, economic growth. It embodies equitable outcomes related to financial well-being as well as opportunities in access to markets and resources, and protects the vulnerable.

Economic inclusion is a high priority issue for the IMF. High inequality is negatively associated with macroeconomic stability and sustainable growth—core to the Fund’s mandate in promoting systemic,

Posted by at 3:47 PM

Labels: Inclusive Growth

Monday, June 11, 2018

Impact of Emigration

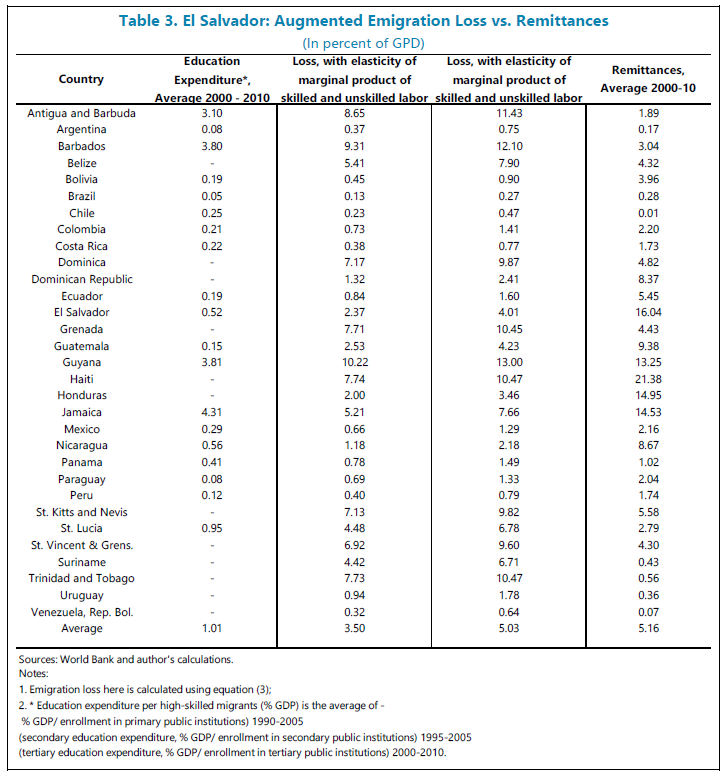

From a new IMF report:

“Remittances outweigh the sum of augmented emigration loss and education expenditure for nearly half of the 31 countries in this sample. Most of these countries are from Central America. The countries for which remittances are not able to outweigh the above sum are mostly the Caribbean ones.

Of course, these results need to be qualified by the fact that there are other costs and benefits of emigration which have not been included in this framework, for e.g. the impact on trade, investment and marginal productivity of capital, and some others which are harder to measure. Other characteristics like demography, civil unrest, and natural disasters have also not been captured. The value of elasticity of factor price of skilled labor may be different from that of overall labor. Estimating country‐level elasticities would better capture country characteristics, but is subject to the availability of detailed survey data.”

From a new IMF report:

“Remittances outweigh the sum of augmented emigration loss and education expenditure for nearly half of the 31 countries in this sample. Most of these countries are from Central America. The countries for which remittances are not able to outweigh the above sum are mostly the Caribbean ones.

Of course, these results need to be qualified by the fact that there are other costs and benefits of emigration which have not been included in this framework,

Posted by at 3:33 PM

Labels: Inclusive Growth

Thursday, June 7, 2018

Snapshots of the Salubrious US Labor Market

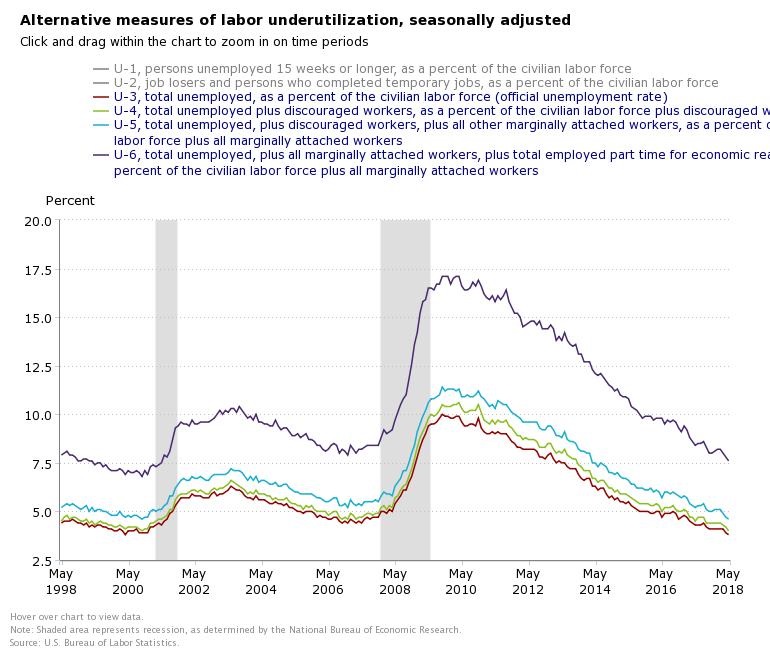

A new post by Timothy Taylor says that “there are a lot of ways to look at unemployment, but whatever measure you choose, the measure is essentially back to what it was before the Great Recession.” “There is no heaven on Earth, and there is no ultimate perfection to be found in real-world labor markets. But the current US labor market situation is really quite good.”

A new post by Timothy Taylor says that “there are a lot of ways to look at unemployment, but whatever measure you choose, the measure is essentially back to what it was before the Great Recession.” “There is no heaven on Earth, and there is no ultimate perfection to be found in real-world labor markets. But the current US labor market situation is really quite good.”

Posted by at 10:18 AM

Labels: Inclusive Growth

Subscribe to: Posts