Showing posts with label Inclusive Growth. Show all posts

Wednesday, January 9, 2019

Factors in Unemployment Dynamics

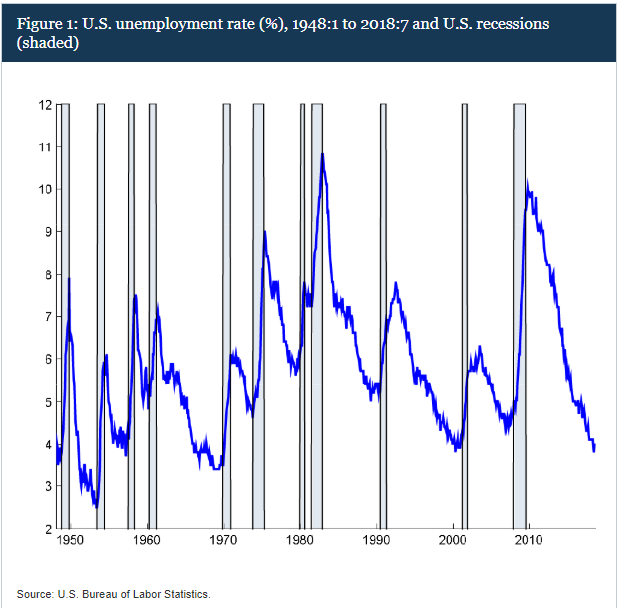

From a FEDS Note by Hie Joo Ahn and James Hamilton:

“The U.S. unemployment rate averaged 8.4% during the first five years of recovery from the Great Recession of 2007-2009, the weakest recovery on record (see Figure 1). But as the expansion continued, unemployment continued to decline and by 2018 reached the lowest levels in almost half a century. Why did unemployment remain so high for so long, and what factors contributed to the recent lows?”

“One of the most striking features of the length of time people stay unemployed is the heterogeneity across the experience of different people. Most people who become unemployed find a new job relatively quickly. Even during the Great Recession, of people who were newly unemployed in month t, on average only 64% were still unemployed in month t + 1. By contrast, if someone has been unemployed for 4-6 months as of month t, on average since 1976, there was an 81% probability that they would still be unemployed in month t + 1. The lowest the latter probability ever got in any month from 1976 to 2018 was 71%. In other words, the newly unemployed during the Great Recession had better success finding jobs than did the long-term unemployed during the strongest economic boom.”

Continue reading here.

From a FEDS Note by Hie Joo Ahn and James Hamilton:

“The U.S. unemployment rate averaged 8.4% during the first five years of recovery from the Great Recession of 2007-2009, the weakest recovery on record (see Figure 1). But as the expansion continued, unemployment continued to decline and by 2018 reached the lowest levels in almost half a century. Why did unemployment remain so high for so long,

Posted by at 10:38 PM

Labels: Inclusive Growth

Transport Infrastructure, City Productivity Growth and Sectoral Reallocation: Evidence from China

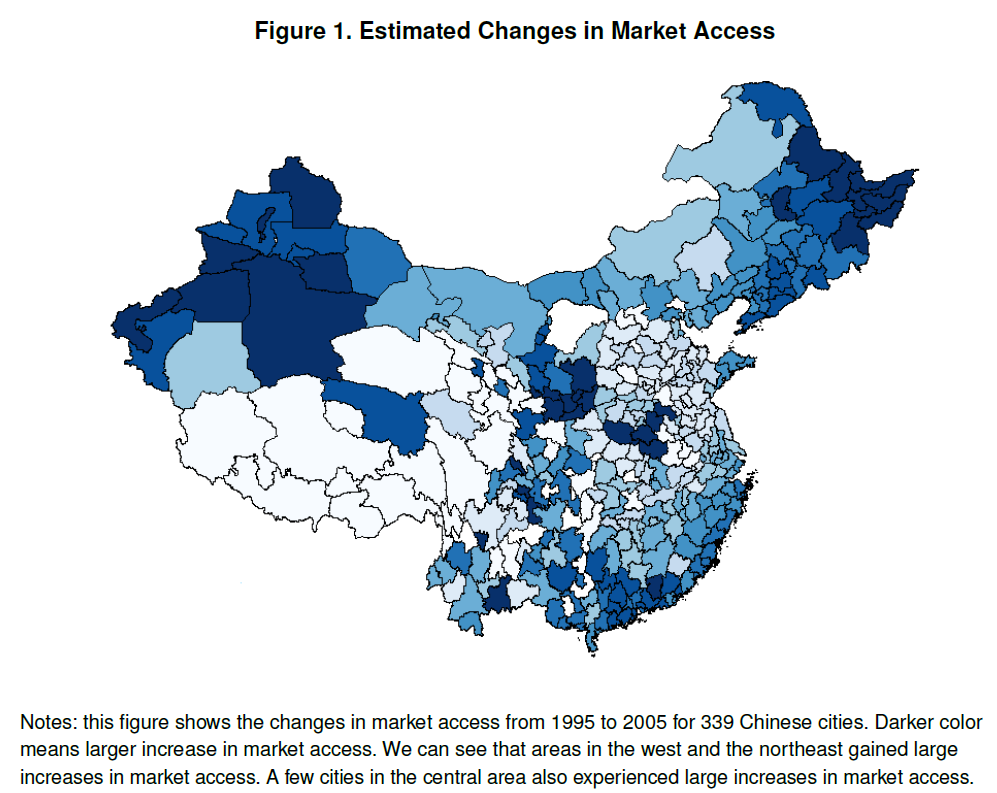

From a new IMF working paper:

“This paper examines the impact of highway expansion on aggregate productivity growth and sectoral reallocation between cities in China. To do so, I construct a unique dataset of bilateral transportation costs between Chinese cities, digitized highway network maps, and firm-level census. I first derive and estimate a market access measure that summarizes all direct and indirect impact of trade costs on city productivity. I then construct an instrumental variable to examine the causal impact of highways on economic outcomes and the underlying channels. The results suggest that highways promoted aggregate productivity growth by facilitating firm entry, exit and reallocation. I also find evidence that the national highway system led to a sectoral reallocation between cities in China.”

“The findings presented in this paper have important policy implications. Facing the threat of secular stagnation, policymakers are searching for tools to boost aggregate demand in the short run and promote economic growth in the long run. After the global recession, there has been a growing interest among policymakers worldwide in using infrastructure investments both as a short-term fiscal policy instrument and as a long-term growth generator. For example, the World Bank has consistently dedicated itself to investing in infrastructure in low-income countries to fight poverty. The International Monetary Fund is also actively advocating for more infrastructure investments in Latin America and Africa to meet the infrastructure needs and boost economic growth in these regions. The two recently-founded development banks–the Asian Infrastructure Investment Bank and the New Development Bank, were established under the leadership of China to address the increasing infrastructure needs in Asia. The US President Donald Trump envisions a trillion-dollar infrastructure plan. The increasing use of infrastructure projects by policymakers begs the question of whether the huge amount of tax dollars spent on infrastructure is well justified by their potential benefits.”

From a new IMF working paper:

“This paper examines the impact of highway expansion on aggregate productivity growth and sectoral reallocation between cities in China. To do so, I construct a unique dataset of bilateral transportation costs between Chinese cities, digitized highway network maps, and firm-level census. I first derive and estimate a market access measure that summarizes all direct and indirect impact of trade costs on city productivity. I then construct an instrumental variable to examine the causal impact of highways on economic outcomes and the underlying channels.

Posted by at 10:28 PM

Labels: Inclusive Growth

Regional differences in the Okun’s Relationship: New Evidence for Spain (1980-2015)

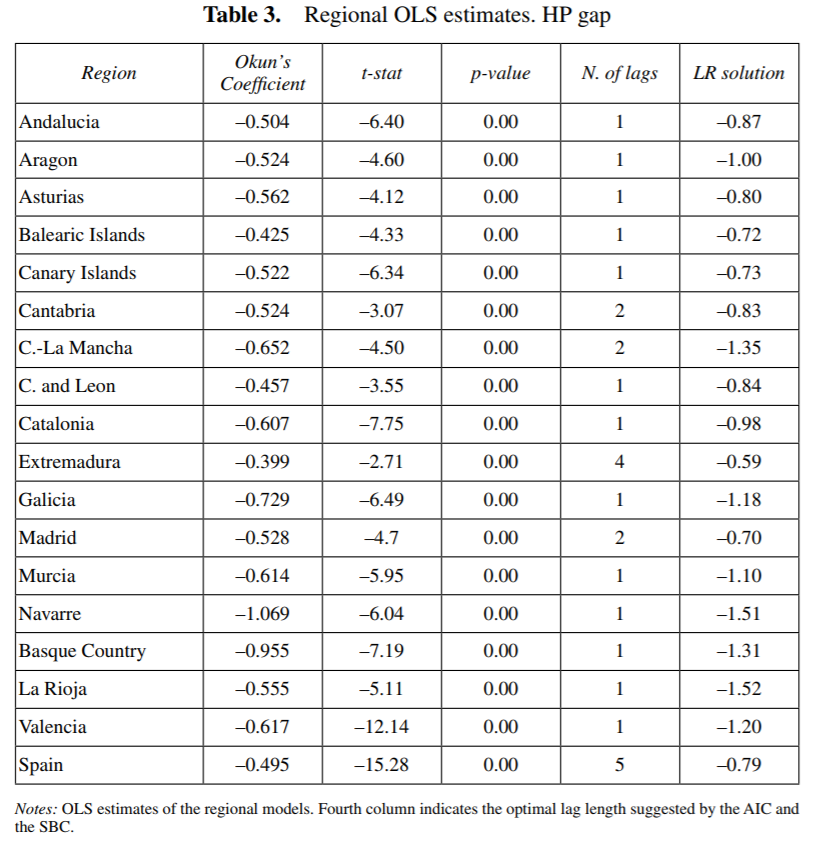

From a new paper on the Okun’s Law in Spain:

“This article provides new empirical evidence on the relationship between the unemployment rate and the output growth in Spain at the regional level. The “gap version” with the output growth on the left-hand side of the equation is our benchmark model. Our empirical results show that all coefficients are significant and show the expected negative sign. Significant regional differences in the Okun’s relationship, both for the short run and the long run, are found. These results are robust to two different specifications for the gaps: the HP filter and the QT procedure. In the final part of the article, it is also found that the OLS and the GMM estimates for panel data exhibit a similar pattern and that there is a clear asymmetry in the Okun’s relationship in booming and recession phases of the Spanish business cycle.”

From a new paper on the Okun’s Law in Spain:

“This article provides new empirical evidence on the relationship between the unemployment rate and the output growth in Spain at the regional level. The “gap version” with the output growth on the left-hand side of the equation is our benchmark model. Our empirical results show that all coefficients are significant and show the expected negative sign. Significant regional differences in the Okun’s relationship,

Posted by at 10:15 PM

Labels: Inclusive Growth

Sunday, January 6, 2019

2019 AEA’s papers on Inequality

Below is a preliminary list of papers that were presented at this year’s AEA Annual Meeting on January 4-6 in Atlanta, Georgia.

On income inequality

- Time Discounting, Savings Behavior and Wealth Inequality – Paper

- Wealth Inequality, Income Volatility, and Race – Paper

- Are Financial Information Technologies Making the Rich Richer? – Paper

- The Uncertainty of Academic Rent and Income Inequality: The OECD Panel Evidence – Paper

- Does Environmental Policy Affect Income Inequality? Evidence from The Clean Air Act. – Paper and Presentation

- Examining Interrelation between Global and National Income Inequalities – Paper and Presentation

- Top 1% Income Shares: Comparing Estimates Using Tax Data – Paper

- Modeling Wealth and Income Inequality: Implications for Optimal Taxation – AEA

- Openness and Income Disparity in Sub-Saharan Africa: A Cross-Country Analysis – AEA

- Military Expenditures and Income Inequality Evidence from a Panel of European Countries (1990-2015) – AEA

On wage and employment inequality

- Global Value Chains, Firms, and Wage Inequality: Evidence from China – Paper

- The Effects of Credit Supply on Wage Inequality between and within Firms – Paper

- College Tuition and Income Inequality – Paper

- The Innovation Premium to Soft Skills in low-skilled occupations – Paper

- Employment Inequality: Why Do the Low-Skilled Work Less Now? – Paper and Presentation

- Skill, Agglomeration, and Inequality in the Spatial Economy – Paper

- Closing the Gap: The Effect of a Targeted, Tuition-Free Promise on College Choices of High-Achieving, Low-Income Students – Paper

- Work and Grow Rich: The Dynamic Effects of Performance Pay Contracts – Paper

- Between Firm Changes in Earnings Inequality: The Role of Productivity Dispersion, the Composition of Firms and Workers, and Industry Earnings Differentials – AEA

- Is Employment Polarization Informative About Wage Inequality and Is Employment Really Polarizing? – AEA

- Income, Poverty, and Inequality over Two Decades – AEA

- Tasks, Occupations, and Wage Inequality in an Open Economy – AEA

On gender inequality

- Coordination of Hours within the Firm – Paper and Presentation

- The Role of Historical Resource Scarcity in Modern Gender Inequality – Presentation

- Gender Inequality and Economic Growth: Evidence from Industry-Level Data – Paper

- Managers’ Gender Norms and the Gender Gap – Paper

- Gender Earnings Inequality and Wage Policy in Kyrgyzstan: Evidence from Household Surveys, 2010-2016 – Paper

- Gender Inequality and Marketisation Hypothesis in sub-Saharan Africa – Paper

- Fiscal Policy Effectiveness on Gender Equality in Asia Pacific: Efficacy of Gender Budgeting – Paper and Presentation

- Fields of Study Choices and the Reproduction of Gender Inequalities – AEA

- The Global Cost of Gender Inequality – AEA

- Sexual Dimorphism in Stature as a Measure of Gender Inequality – AEA

- The Origins and Real Effects of the Gender Gap: Evidence from CEOs’ Formative Years – AEA

On inequality and everything else

- Land Inequality and the Provision of Public Works – Paper

- Consumption Inequality across Heterogeneous Families – Paper

- Coupled Lotteries – A New Method to Analyze Inequality Aversion – Paper

- Biased Perceptions? Consolidating Cross-Country Evidence on Objective and Perceived Inequality – Paper

- Investment-Specific Technological Change, Taxation and Inequality in the U.S. – Paper and Presentation

- The Effect of Political Power on Labor Market Inequality: Evidence from the 1965 Voting Rights Act – Paper

- Regional Inequality in the U.S.: Evidence from City-level Purchasing Power – Paper

- Inequality, Autocracy and Sovereign Funds as Determinants of Foreign Portfolio Flows – Paper and Presentation

- Does the Girl Next Door Affect Your Academic Outcomes and Career Choices? – Paper

- Beyond Piketty: A New Perspective on Poverty and Inequality in India – AEA

- Is India’s Employment Guarantee Program Successfully Challenging Her Historical Inequalities? – AEA

- Regional Differences in the Intergenerational Transmission of Inequality: Evidence from the NLSY – AEA

- Globalization and Inequality in Innovation: A Perspective from U.S. R&D Tax Credit Policy – AEA

- Information and Inequality – AEA

- Redistribution through Markets – AEA

- Estimating Inequality in Air Pollution Exposure – AEA

- Are There Macroeconomic Costs to Racial Inequality in the United States? – AEA

- Food Deserts and the Causes of Nutritional Inequality – AEA

- Spatial Justice, Uneven Development, and Intergenerational Inequality: A ‘Postcolonial’ United States of America – AEA

Below is a preliminary list of papers that were presented at this year’s AEA Annual Meeting on January 4-6 in Atlanta, Georgia.

On income inequality

- Time Discounting, Savings Behavior and Wealth Inequality – Paper

- Wealth Inequality, Income Volatility, and Race – Paper

- Are Financial Information Technologies Making the Rich Richer? – Paper

- The Uncertainty of Academic Rent and Income Inequality: The OECD Panel Evidence – Paper

- Does Environmental Policy Affect Income Inequality?

Posted by at 4:54 PM

Labels: Inclusive Growth

Thursday, January 3, 2019

Countries are advancing efforts to stop criminals from laundering their trillions

From Finance & Development:

“Al Capone had a problem: he needed a way to disguise the enormous amounts of cash generated by his criminal empire as legitimate income. His solution was to buy all-cash laundromats, mix dirty money in with clean, and then claim that washing ordinary Americans’ shirts and socks, rather than gambling and bootlegging, was the source of his riches.

Almost a century later, the basic concept of money laundering is the same, but its scale and complexity have grown considerably. Were Capone alive today, he would have to run his washers and dryers around the clock to keep pace with demand; the United Nations recently estimated that the criminal proceeds laundered annually amount to between 2 and 5 percent of global GDP, or $1.6 to $4 trillion a year.

Threat to stability

Money laundering is what enables criminals to reap the benefits of their crimes, including corruption, tax evasion, theft, drug trafficking, and migrant smuggling. Many of these crimes pose a direct threat to economic stability. Corruption and tax evasion make it difficult for governments to deliver sustainable and inclusive growth by diminishing the resources available for productive purposes, such as building roads, schools, and hospitals. Criminal activity undermines state authority and the rule of law while squeezing out legitimate economic activity. And money laundering may create asset bubbles in markets like real estate, a common vehicle.

A recent example illustrates the point. A Guinean minister helped a foreign company obtain important mining concessions in exchange for $8.5 million in bribes. Falsely reporting that money as income from consulting work and private land sales, the minister transferred it to the United States and bought a luxury estate in New York. But his effort to turn ill-gotten gains into a seemingly legitimate asset was ultimately unsuccessful; last year, he was convicted of money laundering.

In some ways, expensive homes are the modern mobster’s collection of laundromats. A public advisory issued by US authorities last year indicated that over 30 percent of high-value, all-cash real estate purchases in New York City and several other major metropolitan areas were conducted by individuals already suspected of involvement in questionable dealings. The governments of Australia, Austria, Canada, and other countries have concluded that their own real estate markets could also be used to invest and launder dirty money.

Terrorism financing

More worrying still, dirty money—along with clean—may be a source of funding for terrorism and the proliferation of weapons of mass destruction. Terrorist groups need money, lots of it, to compensate fighters and their families; buy weapons, food, and fuel; and bribe crooked officials. Similarly, proliferation does not come cheap. For example, North Korea has reportedly devoted a substantial portion of its scarce resources to developing nuclear weapons.”

Continue reading here.

Rhoda Weeks-Brown

From Finance & Development:

“Al Capone had a problem: he needed a way to disguise the enormous amounts of cash generated by his criminal empire as legitimate income. His solution was to buy all-cash laundromats, mix dirty money in with clean, and then claim that washing ordinary Americans’ shirts and socks, rather than gambling and bootlegging, was the source of his riches.

Almost a century later, the basic concept of money laundering is the same,

Posted by at 9:43 AM

Labels: Inclusive Growth

Subscribe to: Posts