Showing posts with label Inclusive Growth. Show all posts

Tuesday, January 29, 2019

Gender Gaps in Senegal: From Education to Labor Market

From the IMF’s latest report on Senegal:

“For Senegal to meet its goal of reaching emerging market status by 2035, reforms should address development challenges, including gender inequality. Gender inequality is associated with lower economic growth (IMF 2015, Hakura and others 2016; Gonzales and others 2015), higher income inequality (Gonzales and others 2015, IMF 2016), lower economic diversification (Kazandjian and others 2016), and less bank stability (Sahay and others 2017), while it worsens other development indicators.

Senegal still has large gender gaps in both education access and labor opportunities. Authorities should improve incentives for girls to continue their studies, by diminishing indirect costs of studying (such as those in transportation and in school supplies); enforcing civil laws and campaigning against child marriage and early pregnancy; targeting areas with higher gender gaps (especially rural areas); and reducing discrimination in the labor market (thus increasing the financial returns from studying). To improve outcomes in the labor market, authorities should address gender gaps in access to assets, especially credit and land, and employment segregation.

Net costs of policies can be mitigated through an enlargement of the formal sector and an improvement of spending efficiency. As shown in the model simulations, increasing average years of education to 5, combined with increasing the formal sector share of GDP by 10 percentage points can boost government tax revenues to more than cover the costs, generating a net surplus for the government budget. Furthermore, improving education spending efficiency (for instance as pointed out by the experiments in Senegal by Carneiro and others, 2016) would reduce the government’s overall cost of education.

Mixed policies are necessary to tackle all sources of macro-critical gender inequalities. The framework presented is a valuable tool to show how gender gaps should be tackled from different angles simultaneously to end gender gaps in economic opportunities. For instance, although higher expected returns from labor expands female labor force participation (as seen in Figure 6), it is difficult to close the participation gap entirely if policies to address family costs for women to work outside the house (such as those in Table 1) are not implemented. Similarly, wage gaps cannot be closed if authorities address education gaps but ignore gaps in the labor market.”

From the IMF’s latest report on Senegal:

“For Senegal to meet its goal of reaching emerging market status by 2035, reforms should address development challenges, including gender inequality. Gender inequality is associated with lower economic growth (IMF 2015, Hakura and others 2016; Gonzales and others 2015), higher income inequality (Gonzales and others 2015, IMF 2016), lower economic diversification (Kazandjian and others 2016), and less bank stability (Sahay and others 2017), while it worsens other development indicators.

Posted by at 9:25 AM

Labels: Inclusive Growth

Monday, January 28, 2019

Beyond Okun’s law: Introducing labour market flows

From VoxEU post by Guay Lim, Robert Dixon, Jan van Ours:

“One version of Okun’s law specifies a relationship between the change in the unemployment rate and output growth. This column uses US labour market flows data to investigate this relationship between 1990 and 2017. It finds that the net flows between employment and unemployment are sensitive to changes in growth but respond differently to positive and negative changes. This implies that the US Okun relationship is stable but asymmetric, the effect of a change being larger in contractionary periods than in expansionary ones.

There is a large body of research based on Okun (1962) in which researchers (like Okun himself) approach the relationship the law specifies in different ways. Most common are the ‘difference approach’ (i.e. examining the relationship between the change in the unemployment rate and output growth) and the ‘gap approach’ (i.e. examining the relationship between the deviation of the actual from the natural or equilibrium unemployment rate, on the one hand, and the gap between the level of actual and potential output on the other).

Recent research on US data has focused on the magnitude, the stability, and the asymmetry of the Okun coefficient over the economic cycle. Owyang and Sekhposyan (2012) show that during recent US recessions – including the Great Recession – unemployment appears to be more sensitive to economic growth than before. Cazes et al. (2013) also find that the Okun coefficient varies over time and appears to be larger during recessions than during expansions. Pereira (2013) concludes that there are asymmetries in the Okun relationship with a weaker relationship during periods of expansion. Valadkhani and Smyth (2015) also find asymmetries and a weakening of the Okun relationship since the early 1980s. Furthermore, Belaire-Franch and Peiro (2015) conclude that there is an asymmetry in the relationship between unemployment and the business cycle. Finally, Ball et al. (2017) find that Okun’s law is a strong, reliable and stable relationship and that a constant (not time-varying) Okun coefficient is a good approximation to reality.

In a recent paper (Lim et al. 2018), we look at the relationship between changes in the unemployment rate and output growth through the lens of US labour market flows. As far as we know, no one has utilised flows data in this context, yet clearly the change in the unemployment rate reflects the balance of flows into and out of unemployment within a period. Therefore it is natural to look at the Okun relationship as one between output growth and labour market flows. Our analysis is based on the ‘difference approach’ to Okun’s law, since labour market flows are informative about the change in the unemployment rate. We also propose focusing on net flows (the balance of the gross flows between any two states) as they more effectively highlight the dynamics (including asymmetries) behind the evolution of the Okun coefficient.

The flows framework provides an encompassing structure to study the relationship between GDP growth and changes in the unemployment rate and in particular, the conditions under which the Okun coefficient (i.e. the coefficient linking the change in the unemployment rate to the output growth rate) is time-varying and/or asymmetric, i.e. the change in the unemployment rate differs for positive/negative shocks to growth. Furthermore, the flows approach allows us to adopt a three-state analysis – namely, flows between employment, unemployment and not in the labour force. Thus we study how shocks to growth affects labour flows and how they, in turn, translate into changes in three summary statistics – the unemployment rate, the participation rate and the employment–population ratio.”

From VoxEU post by Guay Lim, Robert Dixon, Jan van Ours:

“One version of Okun’s law specifies a relationship between the change in the unemployment rate and output growth. This column uses US labour market flows data to investigate this relationship between 1990 and 2017. It finds that the net flows between employment and unemployment are sensitive to changes in growth but respond differently to positive and negative changes. This implies that the US Okun relationship is stable but asymmetric,

Posted by at 9:48 AM

Labels: Inclusive Growth

Monday, January 21, 2019

Does Ultra-Low Unemployment Spur Rapid Wage Growth?

From a new FRBSF Economic Letter:

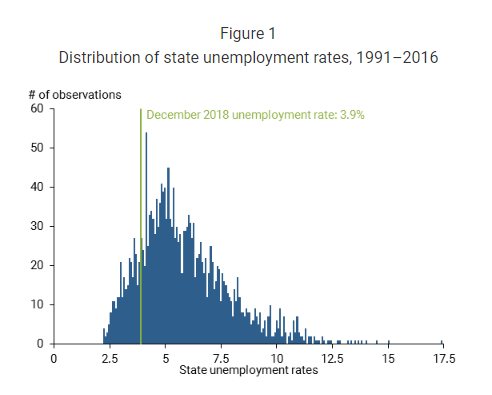

“The unemployment rate ended 2018 at just under 4%, substantially lower than most estimates of the natural rate. Could such an ostensibly tight labor market lead to a sharp pickup in wage growth from its recent moderate pace, such that the relationship between wage growth and unemployment is not always linear? Investigations using state-level data show no economically significant nonlinearity between wage growth and unemployment that would predict an abrupt jump in wage growth.”

“In sum, a careful look at the wage Phillips curve across states yields little evidence supporting the contention that wage growth sharply rises as the labor market reaches especially tight conditions. Of course, the current period may be different from the past. For instance, the typical pattern of local wage growth in a tight local labor market may differ when all other nearby labor markets are experiencing similar tightness, as is currently the case. As a result, geographical labor mobility—which can mute wage pressures in tight markets as workers are attracted to higher-wage areas—may be playing less of a restraining role. With this caveat in mind, given the historical experiences of states in recent decades, we do not foresee a sharp pickup in wage growth nationally if the labor market continues to tighten as many anticipate.”

From a new FRBSF Economic Letter:

“The unemployment rate ended 2018 at just under 4%, substantially lower than most estimates of the natural rate. Could such an ostensibly tight labor market lead to a sharp pickup in wage growth from its recent moderate pace, such that the relationship between wage growth and unemployment is not always linear? Investigations using state-level data show no economically significant nonlinearity between wage growth and unemployment that would predict an abrupt jump in wage growth.”

Posted by at 12:57 PM

Labels: Inclusive Growth

Predicting recessions using term spread at the zero lower bound: The case of the euro area

From a new VOX post:

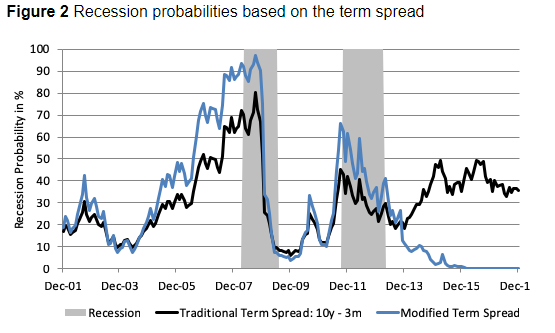

“The flattening of the US yield curve has left academics, central bankers and market commentators divided, with one camp interpreting it as a sign of impending recession (in line with historical patterns), and the other camp arguing that this time is different given unprecedented changes in monetary policy and other structural forces. This column argues that the ECB’s quantitative easing programme undermined the performance of term spreads as predictors of recessions. It suggests and tests a modified term spread and several other variables that are more successful at predicting recessions. ”

“This revised version of the term spread successfully predicts the 2011 recession with a lead time of two months, and signals an average recession probability above 50% during the first half of the recession. It also sees recession probabilities falling to 1% for the period between January 2015 and December 2017, which compares to an average recession signal of 40%, indicated by the traditional term spread over the same period (Figure 2). Given this, we find that switching to the shadow rate in face of the zero lower bound brings a valuable perspective on the term spread as an input factor to recession models.”

From a new VOX post:

“The flattening of the US yield curve has left academics, central bankers and market commentators divided, with one camp interpreting it as a sign of impending recession (in line with historical patterns), and the other camp arguing that this time is different given unprecedented changes in monetary policy and other structural forces. This column argues that the ECB’s quantitative easing programme undermined the performance of term spreads as predictors of recessions.

Posted by at 12:54 PM

Labels: Inclusive Growth

The Inequality Paradox: Rising Inequalities Nationally, Diminishing Inequality Worldwide

From a new ProMarket article:

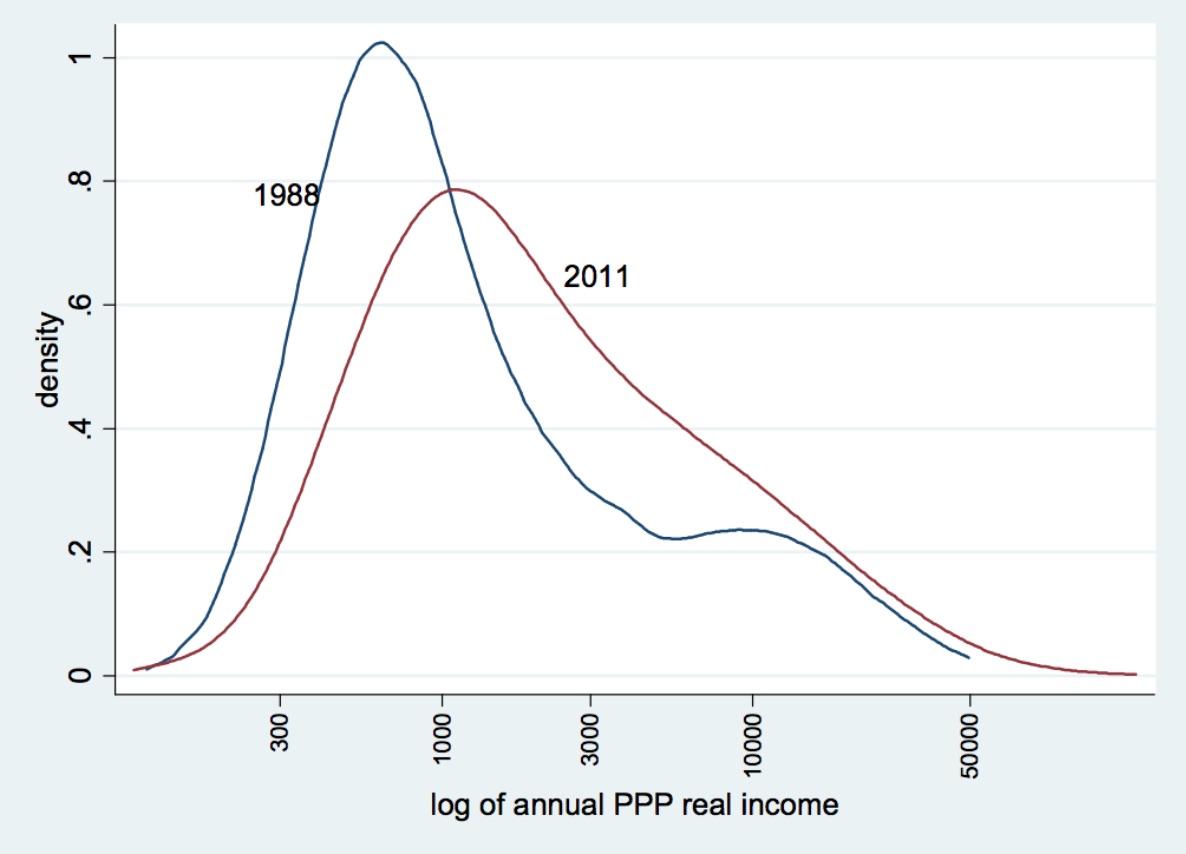

“[…] The reduction in global inequality was driven by high income growth in heretofore very poor countries like China, India, Vietnam, and Indonesia where almost everybody had seen their incomes increase at a fast clip—much faster than in the rich world. Thus a sort of “global middle class” has been created.”

“Figure 2 shows this phenomenon through the thickening of the distribution around the middle: There are simply more people in the world with incomes that are around the world median. These are indeed not the people that, in Western perception, would be considered a “middle class” since their incomes are much lower than typical Western middle class incomes, but from the global point of view they are indeed a (large) group sitting right in the middle of the global income distribution and, if the trends continue, likely to move upward. The slowdown of growth (and several years of negative growth) that affected the rich West in the wake of the global recession further helped the convergence of Asian incomes and reduced global income inequality.”

“Two things are remarkable in the current decline of global income inequality: For the first time in the past 200 years, inequality among world citizens has decreased; and this decrease has taken place while within-national inequalities almost everywhere have gone up. These two facts, translated in terms of winners and losers, mean that workers and the middle classes in emerging economies did well, and workers and the middle classes in the rich world did poorly.”

From a new ProMarket article:

“[…] The reduction in global inequality was driven by high income growth in heretofore very poor countries like China, India, Vietnam, and Indonesia where almost everybody had seen their incomes increase at a fast clip—much faster than in the rich world. Thus a sort of “global middle class” has been created.”

“Figure 2 shows this phenomenon through the thickening of the distribution around the middle: There are simply more people in the world with incomes that are around the world median.

Posted by at 9:45 AM

Labels: Inclusive Growth

Subscribe to: Posts