Showing posts with label Global Housing Watch. Show all posts

Monday, February 3, 2020

Guyana: Housing Market and Implications for Macroprudential Policies

From the IMF’s latest report on Guyana:

“Guyana’s residential real estate prices have been rising, particularly in the capital city Georgetown, following the discovery of oil in 2015. In line with the growing demand for housing, commercial banks’ housing loans have increased, prompting higher household debt. This paper presents two analyses which suggest that housing prices in Georgetown and banks’ lending to the housing sector appear to be in their early stages of growth. However, given the data limitations and caveats that underpin the analyses, the findings could also indicate early signals of possible risks. Further data collection would support surveillance and deeper studies. At the same time, enhancing prudential measures would help safeguard financial and macroeconomic stability. These include strengthening the monitoring of the housing market, bank lending practices and household debt, as well as fortifying the macroprudential framework, including with more effective toolkits for early intervention.”

From the IMF’s latest report on Guyana:

“Guyana’s residential real estate prices have been rising, particularly in the capital city Georgetown, following the discovery of oil in 2015. In line with the growing demand for housing, commercial banks’ housing loans have increased, prompting higher household debt. This paper presents two analyses which suggest that housing prices in Georgetown and banks’ lending to the housing sector appear to be in their early stages of growth.

Posted by at 11:14 AM

Labels: Global Housing Watch

Friday, January 31, 2020

Housing View – January 31, 2020

On cross-country:

- New Risk to World Economy: Synchronized Housing Slowdown – Wall Street Journal

On the US:

- Refinancing Boom Fuels Mortgages to Postcrisis Record – Wall Street Journal

- Housing speculation and its economic consequences – VOX

- Texas Housing Insight – Real Estate Center Texas A&M University

- Average U.S. Home Seller Profits Hit $65,500 in 2019, Another New High – ATTOM Data Solutions

- The Trump administration’s new housing rules will worsen segregation – Economic Policy Institute

- The Folly Of Bernie Sanders’ National Rent Control Proposal – Cato

- Everything You Think You Know About Housing Is Probably Wrong – New York Times

- Concentration in Mortgage Markets: GSE Exposure and Risk-Taking in Uncertain Times – Federal Reserve Bank of Philadelphia

On other countries:

- [Cambodia] Cambodia has oversupply of housing market – Global Property Guide

- [Finland] Housing market in Finland stays weak – Global Property Guide

- [Puerto Rico] Puerto Rico’s housing market bounced back strongly – Global Property Guide

- [United Arab Emirates] Dubai steps up efforts to revive property market – Financial Times

- [United Kingdom] Number of young homeowners catches up with private renters once more – Financial Times

- [Vietnam] Positive outlook for Vietnam’s property market – Global Property Guide

On cross-country:

- New Risk to World Economy: Synchronized Housing Slowdown – Wall Street Journal

On the US:

- Refinancing Boom Fuels Mortgages to Postcrisis Record – Wall Street Journal

- Housing speculation and its economic consequences – VOX

- Texas Housing Insight – Real Estate Center Texas A&M University

- Average U.S. Home Seller Profits Hit $65,500 in 2019,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, January 24, 2020

Housing View – January 24, 2020

On cross-country:

- OECD Affordable Housing Database – OECD

- 16th Annual Demographia International Housing Affordability Survey – Demographia

- The 11 most expensive cities to live in around the world in 2020 – Insider

- Prerequisites to getting Africa’s urbanization ‘right’ – Brookings

On the US:

- The Outlook for Housing – Fed

- Housing Supply Chartbook – Urban Institute

- Slight Gains in 2020 Outlook for Residential Remodeling – Harvard Joint Center for Housing Studies

- Why Manhattan’s Skyscrapers Are Empty – The Atlantic

- How the trade war impacts regional economies and housing markets – Builder

- The slowdown in the US housing market – Central Bank of Spain

- Who’s to blame for high housing costs? It’s more complicated than you think. – Brookings

- Planet Money: Single Women Are Shortchanged In The Housing Market – NPR

- What’s Ahead for the U.S. Housing Market in 2020? – Wharton Business Daily

- Are Housing Markets Still Clearing out the Trash of the Last Bust? – Mises Institute

- Opinion: How unfair mortgage and housing practices affect you and your neighborhood — and what can be done about it – Market Watch

- She Almost Lost Her Home In California’s Wildfires. Instead She Built A $200 Million Business. – Forbes

- Changing supply elasticities and regional housing booms – Bank of England

- Institutional Investors’ Impact on the Housing Market – Urban Institute

- Here’s How Many New Homes It Would Take To Fix The Housing Shortage – Forbes

- Eight ways travelers can fight ‘the Airbnb effect’ on local housing costs – Washington Post

On other countries:

- [China] Magnification of the “China Shock” Through the U.S. Housing Market – VoxChina

- [Hong Kong] Pressure building on rental market amid continued stress – RICS

- [United Arab Emirates] UAE’s housing market remains gloomy – Global Property Guide

- [United Kingdom] Housing equity used to fund home improvements, not future care needs – Financial Times

- [United Kingdom] Evidence and the persistence of mistaken ideas: the case of house prices – mainly macro

On cross-country:

- OECD Affordable Housing Database – OECD

- 16th Annual Demographia International Housing Affordability Survey – Demographia

- The 11 most expensive cities to live in around the world in 2020 – Insider

- Prerequisites to getting Africa’s urbanization ‘right’ – Brookings

On the US:

- The Outlook for Housing – Fed

- Housing Supply Chartbook – Urban Institute

- Slight Gains in 2020 Outlook for Residential Remodeling – Harvard Joint Center for Housing Studies

- Why Manhattan’s Skyscrapers Are Empty – The Atlantic

- How the trade war impacts regional economies and housing markets – Builder

- The slowdown in the US housing market – Central Bank of Spain

- Who’s to blame for high housing costs?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 23, 2020

As California comes to grips with housing crisis, Texas real estate rises in 2020

From Curbed:

“Housing availability and affordability will help determine these states’ trajectories this year

Texas and California represent opposite poles on the spectrum of government ideology—the Golden State’s Democratic supermajority versus the conservative Lone Star State’s regulation-averse independent streak—and in recent years, starkly different results when it comes to housing policy and production.

Predictions for this coming year highlight the divide. According to the recently released Texas A&M Real Estate Center’s outlook for 2020, the state’s homebuilding industry will still have a banner year, despite forecasts for muted economic growth.

“Both the Texas and U.S. economy will likely slow in 2020 yet still register solid growth,” says Real Estate Center research economist Luis Torres. “With uncertainty around trade wars and the current crude oil trajectory, two of the strongest economic drivers for Texas will decrease economic momentum. In contrast, one of the star performers of the 2020 economy will be the housing market, with double-digit growth in new home construction for the first time since 2017.”

California flips that idea on its head. Instead of attracting residents with a surfeit of new housing options despite low growth, it’s posting job growth above the national average, even beating the economies of many European nations when it comes to growth and performance metrics, yet still pushing away many residents—making it harder for lower- and middle-income residents to stay—as a result of soaring housing prices and continued difficulty building new supply.”

Continue reading here.

From Curbed:

“Housing availability and affordability will help determine these states’ trajectories this year

Texas and California represent opposite poles on the spectrum of government ideology—the Golden State’s Democratic supermajority versus the conservative Lone Star State’s regulation-averse independent streak—and in recent years, starkly different results when it comes to housing policy and production.

Predictions for this coming year highlight the divide. According to the recently released Texas A&M Real Estate Center’s outlook for 2020,

Posted by at 9:53 AM

Labels: Global Housing Watch

Wednesday, January 22, 2020

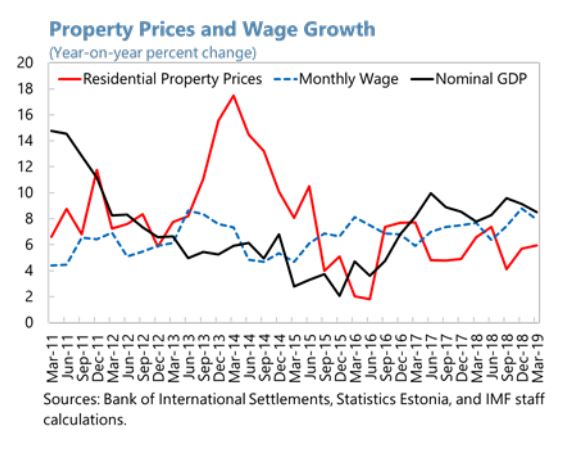

House prices in Estonia

From the IMF’s latest report on Estonia:

“Real estate market activity has moderated, and prices remained anchored to incomes. Transactions in the housing market slowed by 1.6 percent (y/y) in 2018, compared to an increase of 8.2 percent the previous year. House prices increased by 5.7 percent in 2018, driven by the rising share of new houses (…). Furthermore, the ratio of total liabilities to gross wages and salaries declined further from 114 percent in 2017 to 109 percent last year, suggesting a continued reduction in household leverage. Overall price trends remain strong, but aligned to income growth. During 2019H1, there were similar transactions overall compared to 2018H1, but fewer transactions for new apartments. The average price increased by 5.9 percent as new dwellings are being added at a slower pace.”

From the IMF’s latest report on Estonia:

“Real estate market activity has moderated, and prices remained anchored to incomes. Transactions in the housing market slowed by 1.6 percent (y/y) in 2018, compared to an increase of 8.2 percent the previous year. House prices increased by 5.7 percent in 2018, driven by the rising share of new houses (…). Furthermore, the ratio of total liabilities to gross wages and salaries declined further from 114 percent in 2017 to 109 percent last year,

Posted by at 9:57 AM

Labels: Global Housing Watch

Subscribe to: Posts