Showing posts with label Global Housing Watch. Show all posts

Wednesday, February 12, 2020

Scottish Home Prices: Compatible with Euro Membership?

From a paper by William Miles (Wichita State University):

“Although the Scottish electorate voted down independence in 2014, Brexit has led to renewed calls from Scottish political leaders for a second referendum. Scottish independence would likely lead to joining the European Union, and this would obligate Scotland to eventually join the euro common currency. If Scottish home prices were not highly cohesive with those in euro zone countries, the ECB’s monetary policy could cause major disruptions for Scottish housing, and, by extension, the Scottish economy. As an example, if most euro-country home values were rising, but those in Scotland were falling, the ECB would likely run a tight monetary policy, which would be devastating to housing conditions in Scotland. We accordingly investigate the co-movement of house prices in Scotland with those in eight major euro zone countries, as well as co-movement between Scottish and UK home prices, using a variety of metrics. The use of methods that are primarily linear indicates that joining the euro may not result in a large loss of co-movement with other regional housing markets, compared to Scotland’s current correlation with UK national home prices. However, the use of a measure that takes into account differences in the magnitude, and not just the phase of cycles yields results indicating Scotland exhibits very little co-movement with other euro housing markets. Indeed Scotland has co-movement metrics within the euro countries at levels similar to those of Spain and Ireland, which both suffered devastating booms and busts. Thus leaving sterling for the euro could be highly problematic.”

From a paper by William Miles (Wichita State University):

“Although the Scottish electorate voted down independence in 2014, Brexit has led to renewed calls from Scottish political leaders for a second referendum. Scottish independence would likely lead to joining the European Union, and this would obligate Scotland to eventually join the euro common currency. If Scottish home prices were not highly cohesive with those in euro zone countries, the ECB’s monetary policy could cause major disruptions for Scottish housing,

Posted by at 10:45 AM

Labels: Global Housing Watch

A just transition must help those struggling to heat their homes

From Social Europe post by Monique Goyens:

“In the latest contribution to our series on ‘just transition’, Monique Goyens argues that it must address the people finding it hard to pay their energy bills.

The task of moving to a carbon-neutral society is herculean, but the benefits won’t just include saving the planet. There are also long-term economic gains, even for the most hard-up.

An estimated 50 million around the European Union struggle to keep their homes warm and pay their energy bills. Many suffer from the same problems: poorly insulated homes, ill-suited tariffs, insufficient advice on how to save energy or a combination of all three.

The lowest income earners in the EU spend an increasingly large share of their budget on energy—rising from 6 per cent in 2000 to 9 per cent in 2014. In the short term, for this group, it makes more sense to use energy more efficiently than to invest in solar panels, heat pumps or pellet stoves. It will also deliver faster savings.

The choice should not however be between having a warm home and having food on the table. In making their homes more efficient, people consume less energy to heat their living space and can more easily pay their bills.

But getting people to take action can be complex. Those at risk of energy poverty might feel overwhelmed and prioritise solving other problems, such as warmer clothing or food. Often, they might not know what solutions are out there.

For governments and energy advisers to upload advice about insulation to a website isn’t enough. That advice needs to get out to people. Human contact also helps.”

Continue reading here.

From Social Europe post by Monique Goyens:

“In the latest contribution to our series on ‘just transition’, Monique Goyens argues that it must address the people finding it hard to pay their energy bills.

The task of moving to a carbon-neutral society is herculean, but the benefits won’t just include saving the planet. There are also long-term economic gains, even for the most hard-up.

Posted by at 10:42 AM

Labels: Energy & Climate Change, Global Housing Watch, Inclusive Growth

Monday, February 10, 2020

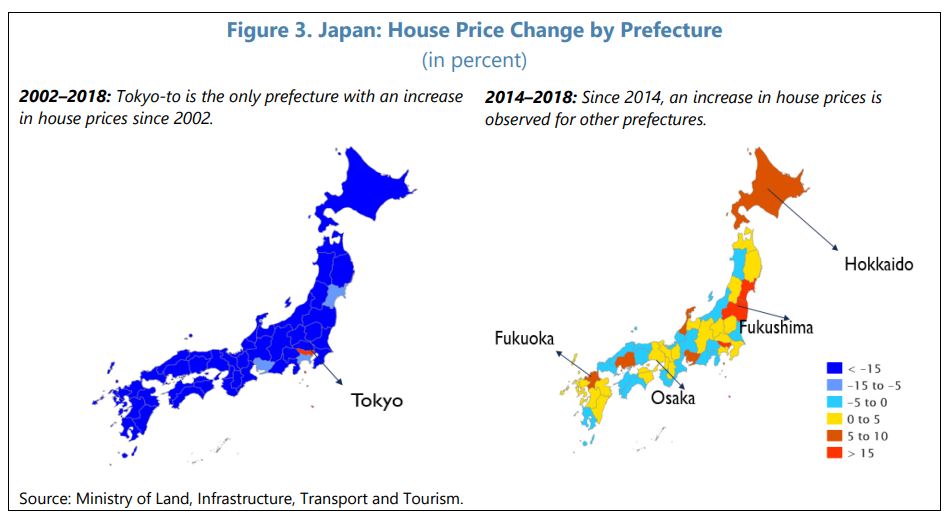

Disappearing Cities: Demographic Headwinds and their Impact on Japan’s Housing Market

From the IMF’s latest report on Japan:

“Japan’s population is rapidly aging and shrinking, and doing so unevenly across regions. Large cities, notably the Greater Tokyo area, are experiencing net migration inflows, while other regions are experiencing net migration outflows. In this chapter, we assess the regional differences in population dynamics and their implications for house price developments in Japan. Due to the durability of housing compared to other forms of investment, the magnitude of house price declines associated with population losses is larger than that of house price increases associated with population gains. These model-based predictions are likely to underestimate the actual fall in house prices associated with future population losses, as expectations of lower housing prices in the future could trigger more population outflows and disposal of houses, especially in rural areas. We suggest policy measures to help close regional disparities and avoid potential over-investment by taking account of demographic trends for housing supply.”

From the IMF’s latest report on Japan:

“Japan’s population is rapidly aging and shrinking, and doing so unevenly across regions. Large cities, notably the Greater Tokyo area, are experiencing net migration inflows, while other regions are experiencing net migration outflows. In this chapter, we assess the regional differences in population dynamics and their implications for house price developments in Japan. Due to the durability of housing compared to other forms of investment,

Posted by at 1:14 PM

Labels: Global Housing Watch

Friday, February 7, 2020

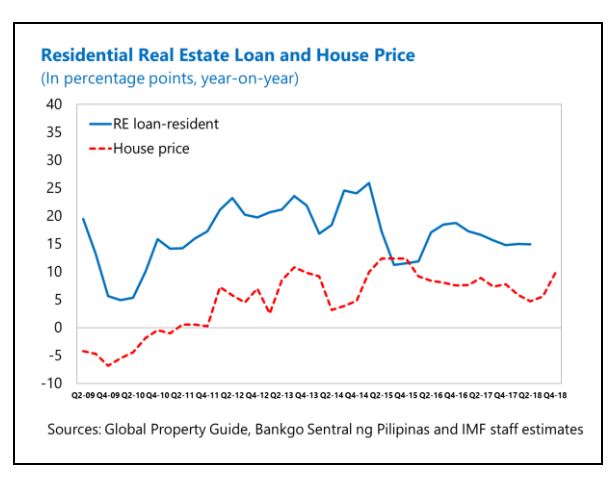

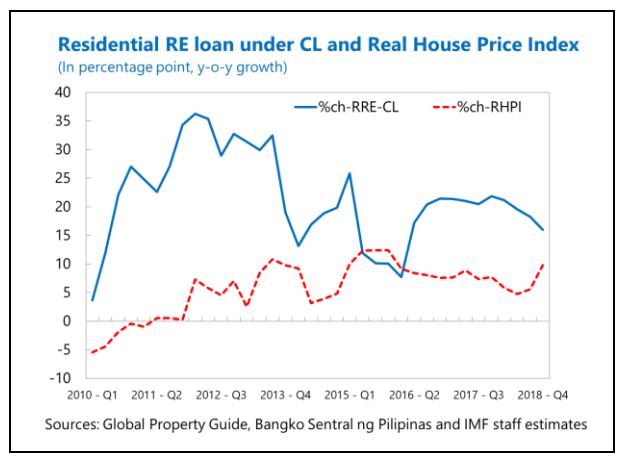

Philippines: Is Real Estate Credit a Concern?

From the IMF’s latest report on the Philippines:

“The near-boom credit episodes detected between 2014 and early 2018 coincided with strong lending growth in the real estate sector. The latter contributed importantly to the strong overall lending growth of close to 20 percent during this period. Notwithstanding some moderation recently, credit to real estate has continued to outpace that in manufacturing and other sectors. It now accounts for the largest share in total loans outstanding (18 percent).

Strong property demand from a few key players drove the real estate credit growth. The recent rise of Chinese online gaming companies operating in the Philippines (Philippines Offshore Gaming Operators—POGO) has led to a large inflow of Chinese workers and increased demand for residential and office properties. The dynamic business process outsourcing (BPO) industry has been another important driver of property demand, while demand for residential housing has also remained strong. Property prices have risen in this environment, translating into higher credit needs for many buyers.

The quality of real estate loans remains sound, despite a recent uptick in NPLs. As of end-2018:Q2, NPL ratios for real estate loans were at record low levels after a steady decline. The relatively stable NPL ratio for residential loans has not followed the continuous decrease in the NPL ratio of commercial real estate loans. This could partly reflect the fact that the 20 percent limit on the share of total bank loans to commercial real estate is binding, which could be keeping bank lending focused on high-quality projects.

Continued strong real house price increases amid the cooling in residential real estate lending suggests a need for close monitoring of related market risks. House price increases in 2018 were broadly similar to those in 2017 despite the slowdown in real estate credit growth. The latter could have partly reflected the tighter lending requirements to the real estate sector in effect since mid-2018.3 Meanwhile, the increase in real house prices could be associated with high real estate demand from POGO companies and workers, which typically does not involve credit from the domestic banking system, or, possibly, increased shadow-banking activities by real estate developers, with increased indirect exposure by domestic banks.

BSP has introduced several macroprudential measures to identify and prevent the buildup of financial stability risks. These include Basel III Liquidity and Net Stable Funding Ratios, and a countercyclical capital buffer (CCyB), which has not yet been activated, as well as the Real Estate Stress Test (REST), real estate sectoral exposure limits, and mortgage collateral value limits. The Philippines’ Macroprudential Policy Measures (Box 2) discusses in greater detail the prudential measures introduced by the BSP since 2007, including newly-introduced measures on the real estate sector credit.”

From the IMF’s latest report on the Philippines:

“The near-boom credit episodes detected between 2014 and early 2018 coincided with strong lending growth in the real estate sector. The latter contributed importantly to the strong overall lending growth of close to 20 percent during this period. Notwithstanding some moderation recently, credit to real estate has continued to outpace that in manufacturing and other sectors. It now accounts for the largest share in total loans outstanding (18 percent).

Posted by at 12:50 PM

Labels: Global Housing Watch

Housing View – February 7, 2020

On cross-country:

- The ECB considers counting owner-occupied housing in inflation – Economist, Financial Times, Bloomberg

- Watch: ING International Survey: Homes & Mortgages – ING

- Housing market polarises opinion between the haves and have-nots – ING

- Saving priorities reflect home ownership challenge – ING

On the US:

- America’s Rental Affordability Crisis is Climbing the Income Ladder – Harvard Joint Center for Housing Studies

- America’s Rental Housing 2020 – Harvard Joint Center for Housing Studies

- U.S. renters are richer, older, and have larger households – Curbed

- California, Mired in a Housing Crisis, Rejects an Effort to Ease It – New York Times

- Demystifying GSE Credit Risk Transfer: How, and How Well, Does It Work? – Harvard Joint Center for Housing Studies

- The Housing Bill Is Dead. Long Live the Housing Bill? – New York Times

- Column: Suburban sprawl wins again in the battle against California’s housing crisis – Los Angeles Times

- To Unleash Housing Supply, Allow and Finance Accessory Dwelling Units – Urban Institute

- Is the Sudden Increase in Black Homeownership Too Good to Be True? – Urban Institute

- All Five Federal Mortgage Programs Should Treat Student Loan Debt the Same Way – Urban Institute

- Labor Conditions Are a Big Factor in Our Current Housing Supply Challenges – Urban Institute

- Housing Finance At A Glance: A Monthly Chartbook, January 2020 – Urban Institute

- In the Land of Big Tech Outposts, a Push for More Housing – Wired

- Three lessons 21st century housing policy could learn from “Little Women” – Brookings

On other countries:

- [China] China’s property market stalls amid coronavirus outbreak – Financial Times

- [Ireland] Irish housing crisis derails Varadkar’s re-election bid – Reuters

- [Netherlands] Luxury Home Buyers Are Revamping Amsterdam’s Historic Housing Stock – Wall Street Journal

On cross-country:

- The ECB considers counting owner-occupied housing in inflation – Economist, Financial Times, Bloomberg

- Watch: ING International Survey: Homes & Mortgages – ING

- Housing market polarises opinion between the haves and have-nots – ING

- Saving priorities reflect home ownership challenge – ING

On the US:

- America’s Rental Affordability Crisis is Climbing the Income Ladder – Harvard Joint Center for Housing Studies

- America’s Rental Housing 2020 – Harvard Joint Center for Housing Studies

- U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts