Showing posts with label Global Housing Watch. Show all posts

Thursday, April 28, 2022

Housing demand and remote work

From a new work by John Mondragon (Federal Reserve Bank of San Francisco) and Johannes Wieland (UCSD and NBER):

“What explains record U.S. house price growth during the Covid-19 pandemic? We show that the shift to remote work explains over one half of the 23.8 percent national house price increase over this period. Using variation in remote work exposure across U.S. metropolitan areas we estimate that an additional percentage point of remote work causes a 0.90 percent increase in house prices after controlling for negative spillovers from migration. This cross-sectional estimate combined with the aggregate shift to remote work implies that remote work raised aggregate U.S. house prices by 14.6 percent. Using a model of remote work and location choice we argue that this estimate is a lower bound on the aggregate effect. Our results imply that the evolution of remote work is likely to have large effects on the future path of house prices and inflation.”

From a new work by John Mondragon (Federal Reserve Bank of San Francisco) and Johannes Wieland (UCSD and NBER):

“What explains record U.S. house price growth during the Covid-19 pandemic? We show that the shift to remote work explains over one half of the 23.8 percent national house price increase over this period. Using variation in remote work exposure across U.S. metropolitan areas we estimate that an additional percentage point of remote work causes a 0.90 percent increase in house prices after controlling for negative spillovers from migration.

Posted by at 6:41 AM

Labels: Global Housing Watch

Wednesday, April 27, 2022

Lessons Learned from Housing Policy during COVID-19

From a new work at Brookings by Kris Gerardi, Lauren Lambie-Hanson, Paul Willen, Laurie Goodman, and Susan Wachter:

“Evidence on housing policy

- The national forbearance mandate, foreclosure moratorium, enhanced Unemployment Insurance (UI), and Economic Impact Payments (EIPs) aided in reducing financial distress for both owners and renters at the outset of the pandemic and prevented longer-run problems in mortgage and housing markets.

- Over 80 percent of borrowers who missed a mortgage payment in the first three months of the pandemic enrolled in forbearance. Although minority mortgage borrowers were much more likely to experience distress and miss mortgage payments, conditional on missing payments, forbearance uptake was similar across racial and ethnic lines.

- Low interest rates led to a wave of refinancing, but fewer Black borrowers benefited from refinancing than white borrowers.

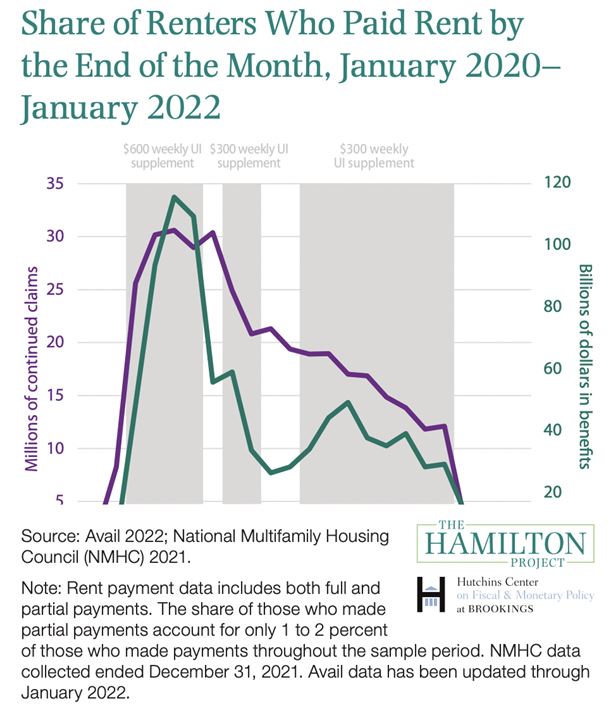

- The share of renters behind on rental payments has been above 2017 levels since 2020. Renter households who missed a rental payment were more likely to be lower-income households and were disproportionately minority households. Missed payments were most common among households who were struggling prior to the pandemic. The erratic rollout of the ERA, which was administered at the local level, prevented timely or easy access to these funds.

- Eviction moratoria resulted in a redirection of scarce household resources to immediate consumption needs and likely prevented homelessness. The decline in evictions during the pandemic is not solely the result of the eviction moratorium. The decline may also reflect the impact of ERA, greater access to legal aid, the impact of eviction diversion programs, and income replacement for households.”

Read the full chapter here.

From a new work at Brookings by Kris Gerardi, Lauren Lambie-Hanson, Paul Willen, Laurie Goodman, and Susan Wachter:

“Evidence on housing policy

- The national forbearance mandate, foreclosure moratorium, enhanced Unemployment Insurance (UI), and Economic Impact Payments (EIPs) aided in reducing financial distress for both owners and renters at the outset of the pandemic and prevented longer-run problems in mortgage and housing markets.

- Over 80 percent of borrowers who missed a mortgage payment in the first three months of the pandemic enrolled in forbearance.

Posted by at 10:16 AM

Labels: Global Housing Watch

Friday, April 22, 2022

Housing View – April 22, 2022

On cross-country:

- These Are the World’s Most Affordable and Least Affordable Cities to Buy a Home – Bloomberg

- We Need Public Housing, Not Affordable Housing. Homeownership is out of reach for millions in Canada and the US. One well-meaning response to this crisis has been to call for more affordable housing. But we should be demanding more social housing instead. – Jacobin

On the US:

- Inflation, Interest and the Housing Paradox – New York Times

- Are We Approaching Bubble Territory in the U.S. Real Estate Market? – Realtor

- US homebuilders say materials are getting easier to find – Quartz

- The case for granny flats. Adding density would boost housing supply and lower emissions – The Economist

- Demographics, COVID-19 Leave Construction with Tight Labor Supply – St. Louis Fed

- Changing Minds on Restrictive Zoning: How to Unclog America’s Home Supply – Manhattan Institute

- Concentration in Homebuilding Driven by a Few Large Builders – Harvard Joint Center for Housing Studies

- High Building Materials Prices Erode Preference for New Construction – NAHB

- What’s Ahead for Cities & Real Estate – Wall Street Journal

- Are Some Homebuyers Strategically Transferring Climate Risks to Lenders? – Richmond Fed

- Property taxes lagged in 2021 — even as real estate prices soared – Axios

- The Sky-High Pandemic Housing Market Finds Gravity Does Exist. Mortgage costs have jumped as the Federal Reserve has raised rates. With higher rates come fewer offers – New York Times

- Decade-High Mortgage Rates Pose Threat to Spring Housing Market. Demand remains strong, but borrowing rates are climbing at fastest pace in years – Wall Street Journal

- Housing Market Fever Starts to Break in Boise – Bloomberg

- Homeowner Groups Seek to Stop Investors From Buying Houses to Rent. Suburban neighborhoods are rewriting rules as rental investors’ purchases surge – Wall Street Journal

- Home Costs and Rents Are Soaring. When Buying Makes Sense – Barron’s

- Higher Rates Start to Cool Canada’s Hot Housing Market. Transactions fall 5.4%, their biggest drop in nine months. Benchmark prices up 27% year-over-year on shortage of homes – Bloomberg

On other countries:

- [Australia] Australia’s COVID-19 pandemic housing policy responses – AHURI

- [Canada] Canada Wants to Double Home Construction But Needs to Find Workers – Canada

- [Germany] Constraints on bank lending unlikely to halt upward residential price spiral – REFIRE

- [Greece] Housing markets, the great crisis, and metropolitan gradients: Insights from Greece, 2000–2014 – IDEAS

- [United Kingdom] House prices to fall? Definitely, but not quite yet. While values are high, real interest rates are negative, making homes surprisingly affordable – FT

On cross-country:

- These Are the World’s Most Affordable and Least Affordable Cities to Buy a Home – Bloomberg

- We Need Public Housing, Not Affordable Housing. Homeownership is out of reach for millions in Canada and the US. One well-meaning response to this crisis has been to call for more affordable housing. But we should be demanding more social housing instead. – Jacobin

On the US:

- Inflation,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, April 15, 2022

Housing View – April 15, 2022

On the US:

- The American property market is once again looking bubbly. Soaring mortgage rates have yet to cool exuberant demand – The Economist

- The housing market is running hot. Can the Fed cool it before it crashes? S&P Global considers 88% of U.S housing regions overvalued – Market Watch

- Early signs of cooling housing market seen in some U.S. cities, Redfin says – Reuters

- The new risk to the housing market – Politico

- What Higher Mortgage Rates Mean for the Housing Market. Wharton’s Benjamin Keys explains why higher mortgage interest rates are discouraging home buyers, but not for long. – Wharton

- Homebuyers Get Desperate in Overheated U.S. Spring Sales Season. Soaring mortgage rates and prices are fueling a rush to seal a deal in market where competition for houses is intense. – Bloomberg

- Fed’s Quantitative Tightening Throws a Wrench Into Mortgage-Bond Market. Investors have been cautious with mortgage bonds, and the Fed’s latest policy signals are unlikely to resolve all their concerns – Wall Street Journal

- Senators Romney, Lee Introduce Bill to Increase Utah Housing Supply – Mitt Romney

- The Landscape of Middle-Income Housing Affordability in California – Terner Center

- Raise Residential Taxes? Bring in Casinos? Cities Look at Ways to Bolster Budgets. Leaders in urban areas struggling with pandemic hits to business and travel revenues are brainstorming longer-term strategies – Wall Street Journal

- How Homeownership Changes You. It’s not just a financial commitment. It can alter people’s relationships to a community, a place, and even time. – The Atlantic

- House-flipping algorithms are coming to your neighborhood. Despite millions of dollars in losses, iBuying’s failure doesn’t signal the end of tech-led disruption, just a fumbled beginning. – Bloomberg

- Pandemic-fueled suburban growth doesn’t mean we should abandon climate resiliency – Brookings

- Understanding the U.S. Housing Crisis in an Era of Inflation. Economist Jenny Schuetz offers a practical guide to one of the biggest challenges facing renters and homebuyers: the skyrocketing cost of housing. – Bloomberg

On China

- China Banks Allow Mortgage Payment Holiday in Covid-Hit Shanghai. Shanghai reports record new infections as lockdown extended. Megabanks’ profit growth at risk amid Covid, property weakness – Bloomberg

On other countries:

- [Australia] Melbourne and Sydney suburbs lead housing value declines – CoreLogic

- [Canada] Canada targets housing, banks in modest-spending budget – Reuters

- [Canada] Canada plans to double homebuilding in decade, but where are the workers? – Reuters

- [Canada] ‘The Top Is Off’: Home Prices Show Signs of Cracking in Canada’s Hot Market. Industry experts are predicting Canada’s home prices could finally start to decline after a 50% surge over the past two years. – Bloomberg

- [Canada] Bank of Canada rate hike could cool Canada’s hot housing markets, economists say – The Globe and Mail

- [Hong Kong] The coming end of ‘property hegemony’. Rising inequality and the deterioration of living conditions and standards among ordinary people – the alleged underlying sources of the 2019 unrest – have been blamed on the dominance of the real estate sector. Beijing may want the next chief executive to crack down – South China Morning Post

- [New Zealand] New Zealand house prices fall as interest rates and inflation weigh – Reuters

- [New Zealand] New Zealand house prices are starting to fall – but many buyers remain locked out. Some economists are predicting a 10% decrease over the year, but even that won’t return prices to those of two years ago – The Guardian

- [United Kingdom] Home Ownership and the UK Mortgage Market: An International Review – Institute for Global Change

- [United Kingdom] Stamp duty holiday tempted buyers into ‘marathon’ loans. Many homebuyers opted for mortgages of 35 years or more – The Guardian

- [United Kingdom] Breathing rooms: pollution and the property market. Air quality could become as important to homebuyers as price per square foot, proximity to schools and transport links – FT

On the US:

- The American property market is once again looking bubbly. Soaring mortgage rates have yet to cool exuberant demand – The Economist

- The housing market is running hot. Can the Fed cool it before it crashes? S&P Global considers 88% of U.S housing regions overvalued – Market Watch

- Early signs of cooling housing market seen in some U.S. cities, Redfin says – Reuters

- The new risk to the housing market – Politico

- What Higher Mortgage Rates Mean for the Housing Market.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, April 13, 2022

Housing Market in Macao

From the IMF’s latest report on Macao:

“Staff reiterates its call to phase out the residency-based LTV capital flow management measure and macroprudential measure (IMF Country Report No. 19/123, Appendix IV). The authorities have introduced this measure in response to a potential risk from soaring property prices fueled by demand from non-residents. However, since 2019 this risk has abated as residential prices have plateaued and residential property transactions by non-residents have fallen. Linking the differentiation in LTV limits directly to banks’ risk assessment of loans and borrowers could attain the same objective without residency-based differentiation.”

From the IMF’s latest report on Macao:

“Staff reiterates its call to phase out the residency-based LTV capital flow management measure and macroprudential measure (IMF Country Report No. 19/123, Appendix IV). The authorities have introduced this measure in response to a potential risk from soaring property prices fueled by demand from non-residents. However, since 2019 this risk has abated as residential prices have plateaued and residential property transactions by non-residents have fallen.

Posted by at 4:56 AM

Labels: Global Housing Watch

Subscribe to: Posts