Showing posts with label Global Housing Watch. Show all posts

Wednesday, June 8, 2022

Vulnerabilities in the housing sector from rising mortgage rates

From the OECD’s latest Economic Outlook:

“House prices, along with household debt, rose steadily throughout the pandemic, even in countries in which valuations were already stretched and debt levels already high. With monetary policy now beginning to normalise, mortgage rates are increasing in many OECD countries, raising solvency concerns. However, vulnerabilities appear contained at present due to households’ relatively strong balance sheets and the limited use of adjustable-rate mortgages (ARM). Still, fragile borrowers could be at risk in economies where ARM dominate, debt-service ratios are high and monetary policy is likely to tighten substantially. The potential adverse consequences for households and financial system resilience of a sharper-than-expected house price reversal also need to be prevented, primarily by macroprudential policy tools.

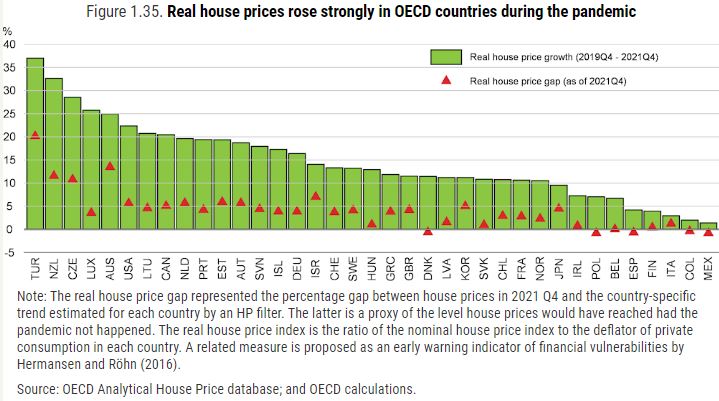

The pandemic pushed house prices to new heights in many countries

House prices rose strongly and quickly in most OECD countries during the pandemic. Between the fourth quarter of 2019 and the fourth quarter of 2021, real house prices rose by 13% in the median OECD economy (Figure 1.35). On average across countries, real house prices in the fourth quarter of 2021 were about 4% higher than expected based on the underlying trend prevailing before the COVID-19 pandemic, suggesting that the pandemic has exacerbated pre-existing tensions in many housing markets. A range of factors can explain this strong and synchronised response of house prices. Exceptionally accommodative monetary conditions, a surge in household savings and unprecedented fiscal support all boosted housing demand during the pandemic, with housing supply temporarily curtailed by mobility restrictions and logistical bottlenecks. Higher financing costs should moderate future housing demand, helping the rise in house prices to abate. A slowdown is already taking place in several key markets, such as the United States, with home sales and prices stabilising or even declining in some large cities, due to rising mortgage rates.

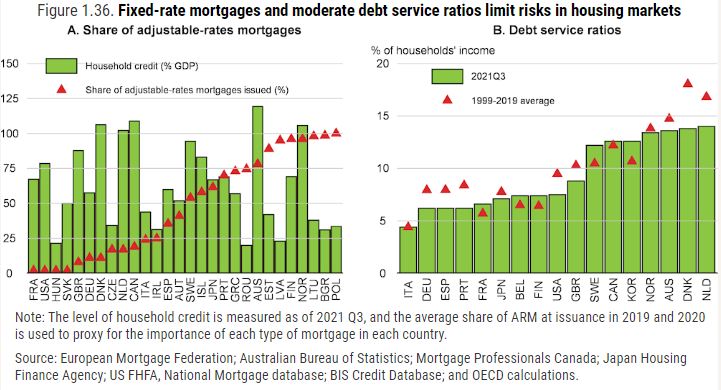

Fixed-rate loans dominate the mortgage landscape

The exposure of households to rising mortgage rates will be damped by the limited use of flexible or adjustable rate mortgages (ARM) in many OECD countries (Figure 1.36, Panel A), although there are also differences across countries in the typical period for which interest rates are fixed (van Hoenselaar et al., 2021). With the exception of Japan and, to some extent, Spain, the largest mortgage markets in advanced economies are heavily dominated by fixed-rate mortgages. In contrast, ARM contracts, which have been shown to be associated with a higher probability of default on mortgages when interest rate rise (Gross et al., 2022), are prevalent in several countries in Southern (Portugal and Greece), Eastern (Poland, Bulgaria, Romania and the Baltics) and Northern Europe (Sweden, Finland and Norway). If monetary policy normalisation proceeds gradually, borrowers should be protected from a sharp increase in financing costs over the medium term. Financially fragile borrowers in countries with independent monetary policies and rising inflation pressures could nonetheless experience a substantial rise in their debt servicing costs, particularly in countries where the ratio of mortgage costs to disposable income is already high for the lowest income quintile (van Hoenselaar et al., 2021).

Households’ savings are high and debt service ratios are still low

Household balance sheets are currently stronger than before the global financial crisis (GFC) in many countries. Stronger regulation in the aftermath of the GFC has limited the amount of risk-taking in the household sector over the last decade. In addition, the recent rise in household debt has been matched by a significant rise in household savings during the pandemic. These savings should support the repayment capacity of many households exposed to adjustable rates, especially if interest rates were to increase more rapidly than expected. Moreover, the low interest rate environment is still keeping average debt service ratios (DSR) in the household sector close or even below their long-term norms (Figure 1.36, Panel B), and significantly below what is considered a stressed DSR. However, aggregate numbers might conceal important heterogeneity, and risks remain that the repayment capacity of low-income borrowers could deteriorate, given the withdrawal of pandemic income support measures and higher inflation.

Macroprudential policies could be strengthened further

Real estate prices might adjust more abruptly. A sharp deterioration in the growth outlook, or a sudden increase in inflationary pressures, could accelerate a correction in housing markets, with potentially damaging consequences for households’ and banks’ balance sheets. Given the large uncertainty surrounding the outlook, it is critical that there are adequate buffers in the banking sector to ensure resilience to unexpected fluctuations in property markets.

Most countries already have policies in place to limit over-indebtedness and associated risks. Following ESRB recommendations (ESRB, 2022), many European countries have recently announced increases in their countercyclical buffer (CCyB) after some relaxation during the pandemic, including some measures explicitly targeting risks in the real estate sector. For instance, Germany’s financial regulator, BaFin, proposed in January 2022 to (i) raise the countercyclical buffer on banks’ domestic exposures to 0.75% of risk-weighted assets (RWAs) from 0% and (ii) to apply an additional systemic risk buffer of 2% of RWAs specifically targeted at residential real estate mortgage loans.

Preventive measures to limit further price increases, such as additional steps to lower LTVs or DSTI ratios, might also be welcome to moderate risks. Some countries have already taken steps to tighten existing tools to moderate new housing loans, while others could consider implementing those tools. In addition to these macroprudential instruments, reforms in rental regulation and property taxation may also be effective means of addressing housing pressures over time. Those tools, along with stronger public investment in social housing and potential land use reforms, especially in job-rich urban areas, could ease the tensions that are still likely to prevail in the medium term (OECD, 2021b). Although the supply of new construction slowed down only moderately during the pandemic, new housing permits and starts dropped significantly in many OECD countries. This gap, along with ongoing supply bottlenecks and labour shortages, is likely to amplify the structural housing shortages affecting many countries.”

From the OECD’s latest Economic Outlook:

“House prices, along with household debt, rose steadily throughout the pandemic, even in countries in which valuations were already stretched and debt levels already high. With monetary policy now beginning to normalise, mortgage rates are increasing in many OECD countries, raising solvency concerns. However, vulnerabilities appear contained at present due to households’ relatively strong balance sheets and the limited use of adjustable-rate mortgages (ARM).

Posted by at 7:34 AM

Labels: Global Housing Watch

Tuesday, June 7, 2022

How did house and stock prices respond to different crisis episodes since the 1870s?

From Shuddhasattwa Rafiq:

“This paper analyses the effects of different types of macroeconomic downturns on house and stock prices. While pre-crisis asset price bubbles are identified as major signals for macroeconomic fragility, recent literature document that house and stock prices are interlinked during recovery periods. To delve deeper into this post-crisis asset price behaviours, we project house and stock price paths following three different macroeconomic crises, normal recessions, financial recessions, and disasters, using historical macro-financial dataset since the 1870s for 17 western economies. We find that financial recessions have the most detrimental effect on house and stock prices followed by severe disasters like war and extreme weather. The results also reveal that stock prices drop substantially immediately after financial crisis and rebound within six years, while impacts to house prices are more persistent. The differences in magnitude and persistence of these effects can be attributed to the nature of crisis and asset class.”

From Shuddhasattwa Rafiq:

“This paper analyses the effects of different types of macroeconomic downturns on house and stock prices. While pre-crisis asset price bubbles are identified as major signals for macroeconomic fragility, recent literature document that house and stock prices are interlinked during recovery periods. To delve deeper into this post-crisis asset price behaviours, we project house and stock price paths following three different macroeconomic crises, normal recessions, financial recessions,

Posted by at 6:46 AM

Labels: Global Housing Watch

Frank Nothaft, economist with “inimitable style,” has died

From Housing Wire:

“Frank Nothaft, chief economist at CoreLogic and before that, the top economist at Freddie Mac, has died. He was 66.

At CoreLogic, Nothaft headed the office of the economist, providing analysis, commentary and forecasting trends in global real estate, insurance and mortgage markets. Prior to joining CoreLogic in 2015, Nothaft had a nearly 30-year career at Freddie Mac, where he was most recently the chief economist.

“When I arrived at Freddie Mac in 2012 he was a long-established major name in mortgage research,” said Donald Layton, who was CEO of Freddie Mac from 2012 to 2018. “It was always a pleasure to work with him because he was truly a nice individual.”

Before joining Freddie Mac, Nothaft was an economist with the Board of Governors of the Federal Reserve System, where he served in the mortgage and consumer finance section and assisted Gov. Henry Wallich.

During his career, Nothaft often was called upon to provide expert commentary on national television and at industry trade conferences, explaining the workings of the housing market for both industry-focused and general audiences.

“Most people knew Frank as one of the nation’s premier housing economists,” said Robin Wachner, a CoreLogic spokesperson. “He was also an outstanding leader and one of those extraordinary people who was loved and admired by everyone who was lucky enough to know him.”

From 2010 to 2015, he was on the faculty at Georgetown University School of Continuing Studies, where he taught urban real estate economics. He was a past president of the American Real Estate and Urban Economics Association and served on the board of directors of the Financial Management Association.

Nothaft was well-liked by fellow economists studying the housing market, as well as his colleagues, who described him as straightforward and prizing accuracy. But he was also known for his quirky sense of style.”

From Housing Wire:

“Frank Nothaft, chief economist at CoreLogic and before that, the top economist at Freddie Mac, has died. He was 66.

At CoreLogic, Nothaft headed the office of the economist, providing analysis, commentary and forecasting trends in global real estate, insurance and mortgage markets. Prior to joining CoreLogic in 2015, Nothaft had a nearly 30-year career at Freddie Mac, where he was most recently the chief economist.

Posted by at 6:44 AM

Sunday, June 5, 2022

Solving the Housing Crisis will Require Fighting Monopolies in Construction

From the James A. Schmitz at the Minneapolis Fed:

“U.S. government concerns about great disparities in housing conditions are at least 100 years old. For the first 50 years of this period, U.S. housing crises were widely considered to stem from the failure of the construction industry to adopt new technology — in particular, factory production methods. The introduction of these methods in many industries had already greatly narrowed the quality of goods consumed by low- and high-income Americans. It was widely known why the industry failed to adopt these methods: Monopolies in traditional construction blocked and sabotaged them. Very little has changed in the last 50 years. The industry still fails to adopt factory methods, with monopolies, like HUD and NAHB, blocking attempts to adopt them. As a result, the productivity record of the construction industry has been horrendous. One thing has changed. Today there is very little discussion of factory-built housing; of the very few that recognize the industry’s failure to adopt factory methods, there is no realization that monopolies are blocking the methods. That these monopolies, in particular, HUD and NAHB, can cause so much hardship in our country, and through misinformation and deceit cover it up, seems almost beyond belief. But, unfortunately, it’s a history that is not uncommon. There are many other industries where monopolies have inflicted great harm on Americans, like the tobacco industry, yet through misinformation and deceit cover up the great harm.”

From the James A. Schmitz at the Minneapolis Fed:

“U.S. government concerns about great disparities in housing conditions are at least 100 years old. For the first 50 years of this period, U.S. housing crises were widely considered to stem from the failure of the construction industry to adopt new technology — in particular, factory production methods. The introduction of these methods in many industries had already greatly narrowed the quality of goods consumed by low- and high-income Americans.

Posted by at 1:05 PM

Labels: Global Housing Watch

Friday, June 3, 2022

A Multi-pronged Strategy to Reduce Housing Market Imbalances in Luxembourg

From the IMF’s latest report on Luxembourg:

“With residential real estate prices more than doubling in a decade and (60 percent in the last 4 years),

housing is becoming a key challenge in Luxembourg. Although 2/3rd of households are homeowners,

affordability concerns have been on the rise, including for the middle-income. If continued, these

trends could hamper the country’s competitiveness and attractiveness for workers and pose risks for

financial stability in the medium term. Building on previous IMF analytical work, and looking at the

drivers of the recent housing trends as well as the government’s policies, the paper advocates for a

comprehensive strategy to reduce imbalances in the housing market. The approach includes measures

to: i) boost housing supply (e.g., by mobilizing vacant dwellings and unused land, using existing

resources more efficiently by building more, denser, faster, and at a lower cost), while increasing the

share of affordable homes, ii) contain demand pressure and reduce its geographic concentration,

iii) increase residential mobility, and iv) reduce under occupation. The paper also emphasizes the need

for a more effective and coordinated implementation of reforms.”

From the IMF’s latest report on Luxembourg:

“With residential real estate prices more than doubling in a decade and (60 percent in the last 4 years),

housing is becoming a key challenge in Luxembourg. Although 2/3rd of households are homeowners,

affordability concerns have been on the rise, including for the middle-income. If continued, these

trends could hamper the country’s competitiveness and attractiveness for workers and pose risks for

financial stability in the medium term.

Posted by at 10:34 AM

Labels: Global Housing Watch

Subscribe to: Posts