Showing posts with label Global Housing Watch. Show all posts

Friday, December 23, 2022

Housing View – December 23, 2022

On cross-country:

- Conference: Alternative technics on housing and construction during Covid – REFINE

On the US—developments on house prices, rent, permits and mortgage:

- Mortgage Buydowns Are Making a Comeback. Soaring rates have revived interest in a product that fell out of favor after the financial crisis – Wall Street Journal

- Higher mortgage rates depress U.S. single-family housing starts, building permits – Reuters

- Single-Family Permits Continues On A Downward Trend in October 2022 – NAHB

- US Housing Starts, Permits Fall on Slide in Single-Family Homes. Total new construction slips 0.5%, marking third-straight drop. Permit applications for one-family homes lowest since May 2020 – Bloomberg

- In US housing market, homebuilders are wary of starting new projects. Permits to build new houses fell by double digits in November. – Quartz

- Prepare for US house prices to slump, unemployment to spike, and a recession to set in, Harvard economist Kenneth Rogoff says – Markets Insider

- The Normal Seasonal Pattern for Median House Prices – Calculated Risk

- 3rd Look at Local Housing Markets in November. “Median home prices in the Austin-Round Rock MSA experienced a 0% year over year increase” – Calculated Risk

- 10 facts about U.S. renters during the pandemic – Pew Research Center

- Lawler: Early Read on Existing Home Sales in November. Another Step Down for Sales in November – Calculated Risk

- 4th Look at Local Housing Markets in November; California Sales off 48% YoY. Another step down in sales in November – Calculated Risk

- Existing Home Sales Decline Further in November – NAHB

- NAR: Existing-Home Sales Decreased to 4.09 million SAAR in November. Median Prices Down 10.4% from Peak in June 2022 – Calculated Risk

- Existing-Home Sales Dipped 7.7% in November – NAR

On the US—other developments:

- Why This Housing Downturn Isn’t Like the Last One. A postcrisis mortgage-market makeover and an overhaul of the financial system make a repeat of 2008 unlikely – Wall Street Journal

- Homing in on a Housing Recovery. After a miserable year for housing, some reasons for optimism – Wall Street Journal

- The Push of Big City Prices and the Pull of Small Town Amenities – Philadelphia Fed

- Where Are the Most and Least Affordable Homes? A new study compares median home prices against household income, property taxes and mortgage expenses to determine affordability. – New York Times

- Americans Want More Affordable Housing — Just Not Nearby – Five Thirty Eight

- The Size of the Housing Shortage: 2021 Data – NAHB

- In the US, Owning a Home May Not Lead to a Better Life – Insead

- Biden Administration Calls for 25% Cut in Homelessness by 2025. The Biden administration’s new strategic plan to address homelessness includes a focus on equity and a promise to help cities build more housing. – Bloomberg

- America’s Housing Shortage Crisis, in Two Maps. Chronic NIMBYism has left America’s population centers without enough places to live. – Bloomberg

- The Homeownership Society Was a Mistake. Real estate should be treated as consumption, not investment. – The Atlantic

- Housing Sentiment in the Fourth Quarter of 2022 – Freddie Mac

- Nine Percent of New Homes Are Teardowns – NAHB

- Eviction and Poverty in American Cities – Philadelphia Fed

- Evictions in New England and the Impact of Public Policy during the COVID-19 Pandemic – Boston Fed

On China:

- China mulls new measures to support real estate sector – vice premier – Reuters

- China To Correct Past ‘Mistaken’ Housing Policies: Top Economist. Government is changing tone on the property sector: Yao Yang. 2021 policies to curb the sector were ‘mistaken,’ he says – Bloomberg

On other countries:

- [Australia] The Stench of Failure: How Perception Affects House Prices – NBER

- [Australia] Australia’s housing crisis, largely hidden, is getting worse – Reuters

- [Canada] Cities have to expand for house prices to fall – New Geography

- [Israel] House prices keep soaring, marking record 20.3% rise in a year. Dramatic figure comes as other inflationary pressures ease, with consumer prices rising more slowly – The Times of Israel

- [Sweden] Sweden’s Housing Market Seeks Bottom as Price Drop Continues. HOX index shows decline continued for eighth month in a row. Price drop of 15% from the peak also seen in other recent data – Bloomberg

- [United Kingdom] How UK House Prices Could Fall by 30%. There’s plenty of precedent for a steep decline in ‘real’ values. – Bloomberg

- [United Kingdom] UK house prices expected to fall by 8% next year, says Halifax. Lender says market rebalancing after years of growth, as mortgage rates and cost of living push prices down – The Guardian

- [United Kingdom] Debt charities warn over surging mortgage costs for millions of borrowers. Concerns mount after Bank of England increases interest rates to 3.5 per cent – FT

- [United Kingdom] UK mortgage guarantee scheme extended by a year. Ministers delay closure to help first-time buyers facing high interest rates and fewer borrowing options – FT

- [United Kingdom] House prices in central London fell by a quarter over five years. Expensive areas, hardest hit in real terms, will feel the effects of high mortgage rates in 2023 – FT

On cross-country:

- Conference: Alternative technics on housing and construction during Covid – REFINE

On the US—developments on house prices, rent, permits and mortgage:

- Mortgage Buydowns Are Making a Comeback. Soaring rates have revived interest in a product that fell out of favor after the financial crisis – Wall Street Journal

- Higher mortgage rates depress U.S. single-family housing starts, building permits – Reuters

- Single-Family Permits Continues On A Downward Trend in October 2022 – NAHB

- US Housing Starts,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, December 21, 2022

The Push of Big City Prices and the Pull of Small Town Amenities

From a new paper by Heidi Artigue, Jeffrey Brinkman, and Svyatoslav Karnasevych:

“As house prices continue to rise in large, supply-constrained cities, what are the implications for other places that have room to grow? Recent literature suggests that amenities that improve quality of life are becoming increasingly important in location decisions. In this paper, we explore how location amenities have differentially driven population and price dynamics in small towns versus big cities, with a focus on the role of housing supply. We provide theory and evidence that demand for high-amenity locations has increased in recent decades. High-amenity counties in large metropolitan areas have experienced relatively higher price increases, while high-amenity counties in small metros and rural areas have absorbed increased demand through population growth. This divergence in population dynamics between big cities and small towns was driven by domestic migration, with high-amenity small towns and rural areas experiencing significant domestic in-migration.”

From a new paper by Heidi Artigue, Jeffrey Brinkman, and Svyatoslav Karnasevych:

“As house prices continue to rise in large, supply-constrained cities, what are the implications for other places that have room to grow? Recent literature suggests that amenities that improve quality of life are becoming increasingly important in location decisions. In this paper, we explore how location amenities have differentially driven population and price dynamics in small towns versus big cities,

Posted by at 11:42 AM

Labels: Global Housing Watch

Tuesday, December 20, 2022

Conference: Alternative technics on housing and construction during Covid

From Real Estate Finance and Economics Network:

“A conference was organized by the Alter Property Data Network on November 21st, 2022, hosted by ReFinE/Institut Louis Bachelier. This network gathers economists, data scientists and practitioners from all over the world (from the IMF, World Bank, OECD, European Commission, BIS, central banks, universities…) who share information, data, programs and papers on alternative techniques (web-scraping, mobile data, satellite data, machine learning, text mining…) related to housing and construction in general.

(…)

The theme of this conference was: To what extent do alternative techniques (web-scraping, satellite data…) help to better understand what happened during the Covid crisis in housing and construction?

After a transversal introductory statement by Yunhui Zhao (IMF), this conference gave insights mainly from two different perspectives, first showing how alternative tools such as web-scraping or satellite data can give additional information on real estate during the Covid-19 and showing the latest developments on methodological tools on housing and construction.

The first part included:

- An OECD paper showing evolutions in housing demand during the pandemics: Rudiger Ahrend, Manuel Bétin, Maria Paula Caldas, Boris Cournède, Marcos Diaz Ramirez, Pierre-Alain Pionnier, Daniel Sanchez-Serra, Paolo Veneri and Volker Ziemann (OECD): Changes in the geography housing demand after the onset of COVID-19: First result for large cities in 13 OECD countries, https://www.oecd-ilibrary.org/economics/changes-in-the-geography-housing-demand-after-the-onset-of-covid-19-first-results-from-large-metropolitan-areas-in-13-oecd-countries_9a99131f-en

- A Banca d’Italia paper analyzing the evolution of housing preferences in the case of Italy: Elisa Guglielminetti & Michele Loberto & Giordano Zevi & Roberta Zizza (Banca d’Italia): Living on my own: the impact of the Covid-19 pandemic on housing preferences; https://www.bancaditalia.it/pubblicazioni/qef/2021-0627/QEF_627_21.pdf

- An article that complements the official statistics on the evolution of the housing market in the UK: Jean-Charles Bricongne (Banque de France), jointly with Baptiste Meunier and Sylvain Pouget: Web-scraping housing prices in real-time: the Covid-19 crisis in the UK (https://www.banque-france.fr/sites/default/files/medias/documents/wp827.pdf )

The second part on methodological tools included the following presentations:

- Alexandre Banquet (OECD): presentation of advances in satellite data for the monitoring of built areas: Dynamic World and new version of GHSL

- Nina Biljanovska (IMF), Chenxu Fu (IMF) & Deniz Igan (BIS), Housing Affordability: A New Panel Dataset

- Emmanuel Flachaire, Gilles Hacheme, Sullivan Hué and Sébastien Laurent (AMSE): GAM(L)A: An econometric models for interpretable Machine Learning, used to forecast housing prices in Boston (USA); https://slaurent.pagesperso-orange.fr/pdf/GAMA.pdf

- Pierre-Alain Pionnier (OECD), jointly with Johannes Schuffels: Estimating regional house price levels; Methodology and results of a pilot project with Spain, https://www.oecd-ilibrary.org/fr/economics/estimating-regional-house-price-levels_b9fec1b2-en “.

From Real Estate Finance and Economics Network:

“A conference was organized by the Alter Property Data Network on November 21st, 2022, hosted by ReFinE/Institut Louis Bachelier. This network gathers economists, data scientists and practitioners from all over the world (from the IMF, World Bank, OECD, European Commission, BIS, central banks, universities…) who share information, data, programs and papers on alternative techniques (web-scraping, mobile data, satellite data, machine learning, text mining…) related to housing and construction in general.

Posted by at 10:09 AM

Labels: Global Housing Watch

Monday, December 19, 2022

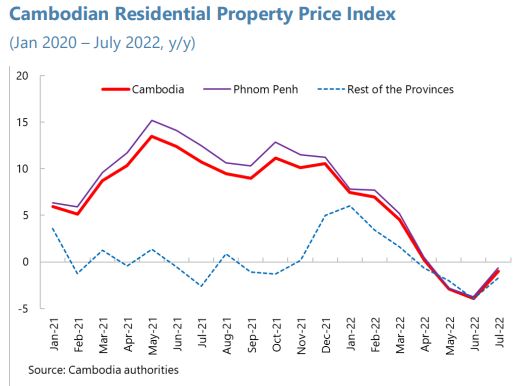

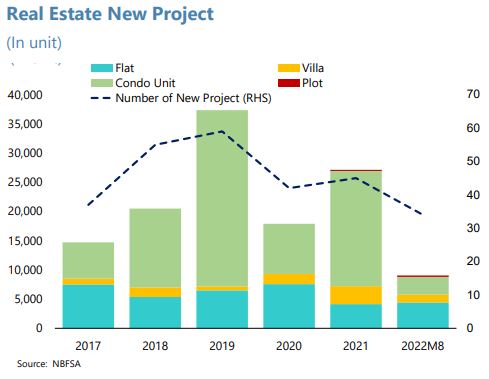

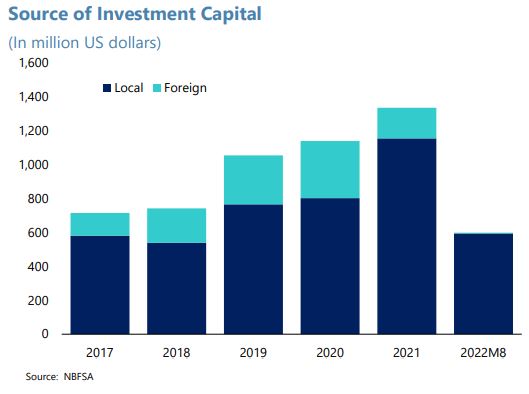

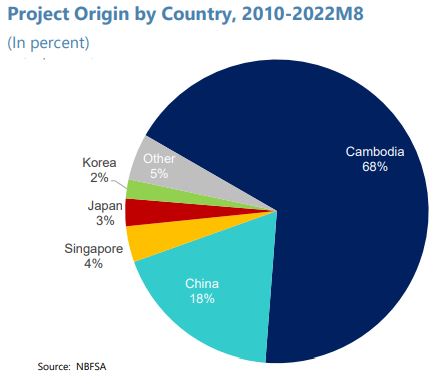

Housing Market in Cambodia

From the IMF’s latest report on Cambodia:

“There are signs that the domestic real estate market (both high-end residential and commercial) is experiencing a downturn. Yields indicate a growing surplus of commercial and high-end residential space. Rental prices for commercial developments, as well as purchase prices for high-end residential properties, appear to be falling after more than a decade of sustained growth. The sector is important in terms of both GDP share and exposure of the rest of the economy.”

From the IMF’s latest report on Cambodia:

“There are signs that the domestic real estate market (both high-end residential and commercial) is experiencing a downturn. Yields indicate a growing surplus of commercial and high-end residential space. Rental prices for commercial developments, as well as purchase prices for high-end residential properties, appear to be falling after more than a decade of sustained growth. The sector is important in terms of both GDP share and exposure of the rest of the economy.”

Posted by at 5:04 AM

Labels: Global Housing Watch

Friday, December 16, 2022

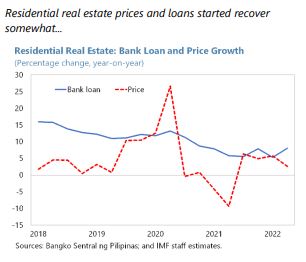

Housing Market in the Philippines

From the IMF’s latest report on the Philippines:

Posted by at 10:23 PM

Labels: Global Housing Watch

Subscribe to: Posts