Showing posts with label Global Housing Watch. Show all posts

Monday, February 3, 2014

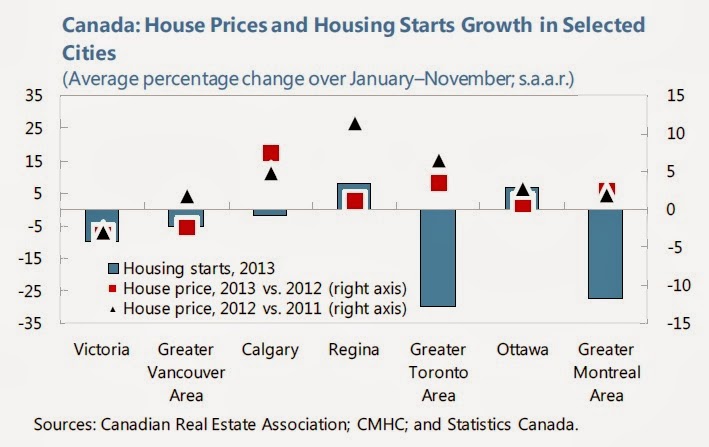

House Prices in Canada

“Household leverage remains high, and while house price and construction growth have come off their post-crisis peaks, high valuations and excess supply in a number of housing markets are a source of vulnerability. If maintained, the ongoing moderation in the housing market suggests little need for additional macro-prudential measures but it is important to remain vigilant. Over the longer term, rethinking the role of government-backed mortgage insurance may reduce the government exposure to housing sector risks and lead to a more efficient allocation of resources,” says the new IMF report on Canada.

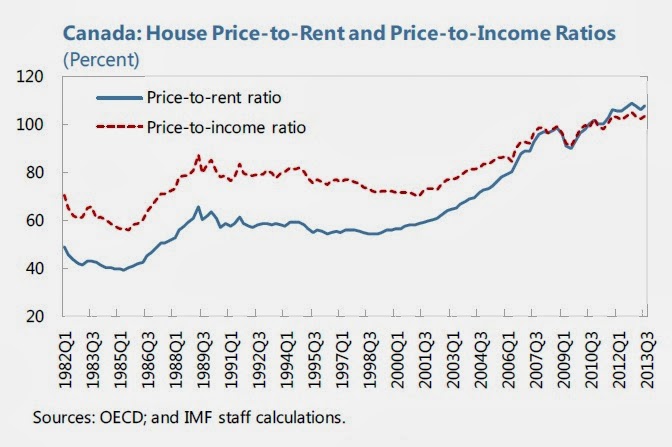

More specifically on house prices and valuation measures, it says “Canada’s housing market has cooled but house prices remain overvalued, although with important regional differences. Despite picking up somewhat in mid-2013, in line with renewed strength in resale activity, Canada’s house price inflation and residential investment growth have slowed. On average across Canada, house prices grew about 4 percent (y/y) in November 2013, up from 2 percent in April but about half the pace two years ago. The slowdown involved all large metropolitan areas except Calgary, particularly Vancouver (where house prices in the first eleven months of 2013 were about 3 percent lower than a year ago). Housing starts have also picked up since April 2013, but are on a declining trend: as of November 2013, their 6-month moving average was about 10 percent below last year’s peak, mainly owing to weaker construction of multiple units, especially in Ontario. Despite the downward trend in growth, a few simple indicators continue to suggest overvaluation in the Canadian housing market. In particular, house prices are high relative to both income and rents, compared to historical averages and many other advanced economies. Staff estimates that, in real terms, average house prices in Canada are about 10 percent above what would be justified by fundamentals, with most of the gap coming from the real estate markets in Ontario and Québec.”

“Household leverage remains high, and while house price and construction growth have come off their post-crisis peaks, high valuations and excess supply in a number of housing markets are a source of vulnerability. If maintained, the ongoing moderation in the housing market suggests little need for additional macro-prudential measures but it is important to remain vigilant. Over the longer term, rethinking the role of government-backed mortgage insurance may reduce the government exposure to housing sector risks and lead to a more efficient allocation of resources,”

Posted by at 5:42 PM

Labels: Global Housing Watch

Wednesday, January 29, 2014

House Prices in Peru

“Real estate prices have risen substantially over the past few years (…) However, deviation of prices from fundamentals has apparently been minimal,” according to the new IMF report on the Peruvian economy.

“Real estate prices have risen substantially over the past few years (…) However, deviation of prices from fundamentals has apparently been minimal,” according to the new IMF report on the Peruvian economy.

The report also points out that (i) the “ratio of house prices to annual rental income has increased slightly to 15½ in 2013 from around 13½ in 2010″ and (ii) the recent macroprudential measures taken–“capital charges on higher loan-to-value mortgages, Read the full article…

Posted by at 6:09 PM

Labels: Global Housing Watch

Monday, January 27, 2014

Global House Price Index Continues To Inch Up

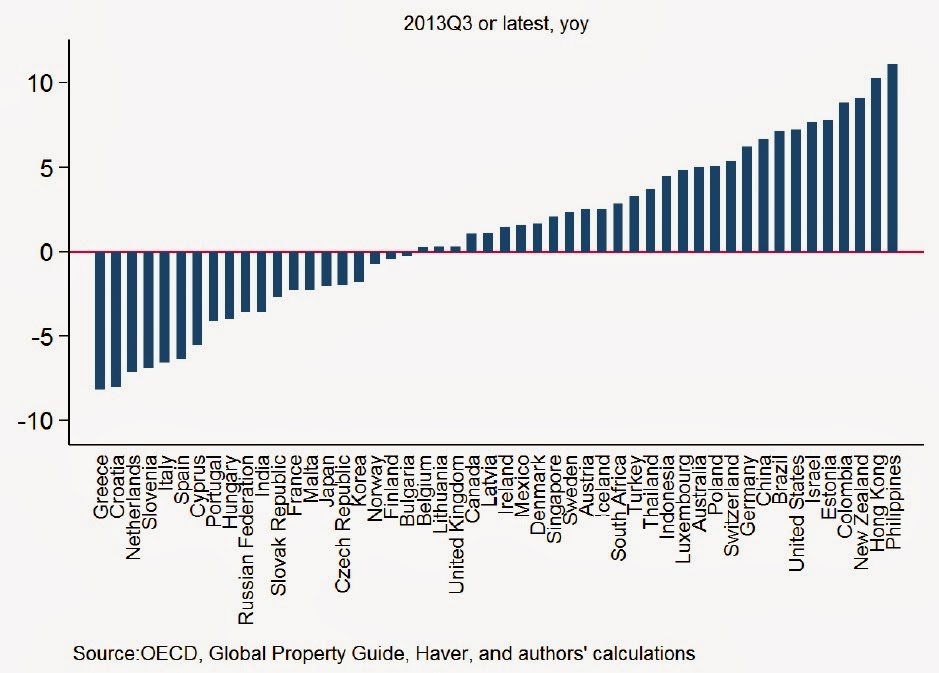

Last month, the IMF’s quarterly magazine, Finance & Development, provided a panoramic view of developments in global housing markets. This report updates that article to reflect data on house prices that has come in over the past six weeks. House prices increased in 31 out of the 51 countries we monitor, keeping our overall Global House Price Index inching up.

In this report, we now provide statistics on how long the current cycle in house prices has lasted, plus a summary table on which way various housing market indicators are pointing. As before, links are provided to IMF analysis of housing market developments (new in this edition: IMF views on developments in Brazil, Denmark, Finland, Ireland, Slovenia and Uruguay) and links to private sector views.

Last month, the IMF’s quarterly magazine, Finance & Development, provided a panoramic view of developments in global housing markets. This report updates that article to reflect data on house prices that has come in over the past six weeks. House prices increased in 31 out of the 51 countries we monitor, keeping our overall Global House Price Index inching up.

In this report,

Posted by at 1:45 PM

Labels: Global Housing Watch

Friday, January 17, 2014

House Prices in Slovenia

House prices “(…) appear to be dipping again,” says the new IMF report on Slovenia.

House prices “(…) appear to be dipping again,” says the new IMF report on Slovenia.

Posted by at 7:35 PM

Labels: Global Housing Watch

Friday, January 10, 2014

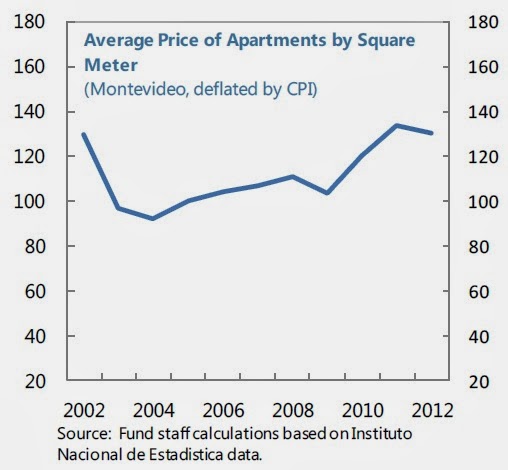

House Prices in Uruguay

“The growth of house prices moderated in 2012,” says new IMF report on Uruguay.

“The growth of house prices moderated in 2012,” says new IMF report on Uruguay.

The report points out that “most of the expansion in the real estate market in recent years had been concentrated in the urban luxury segment, and according to anecdotal evidence, has received heavy foreign investment (mainly from Argentina). The vast majority of real estate transactions are done in cash (household mortgages stood at 4 percent of GDP in July 2013, broadly unchanged from levels in recent years). Read the full article…

Posted by at 10:37 PM

Labels: Global Housing Watch

Subscribe to: Posts