Showing posts with label Global Housing Watch. Show all posts

Wednesday, May 28, 2014

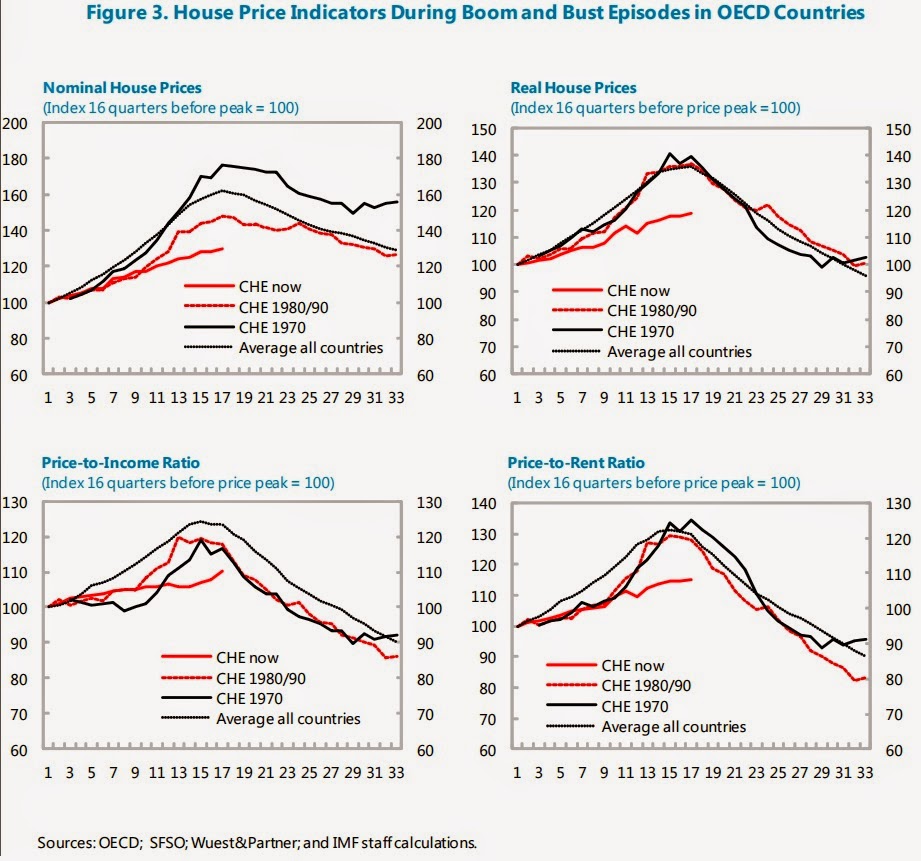

House Prices in Switzerland

“With monetary conditions remaining accommodative and housing prices [in Switzerland] growing faster than incomes, measures to curb mortgage demand especially from the more vulnerable households need to be strengthened,” says the latest IMF’s annual report on Switzerland. Read the report here for a dedicated section on the housing market.

“With monetary conditions remaining accommodative and housing prices [in Switzerland] growing faster than incomes, measures to curb mortgage demand especially from the more vulnerable households need to be strengthened,” says the latest IMF’s annual report on Switzerland. Read the report here for a dedicated section on the housing market.

Posted by at 8:53 PM

Labels: Global Housing Watch

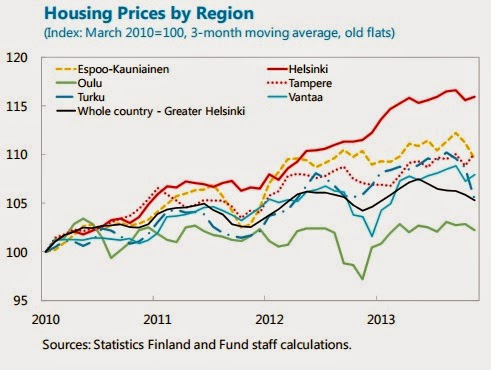

House Prices in Finland

“(…) the level of overvaluation [in house prices in Finland] is lower than in other Nordic countries. However, the national average conceals rapid growth in prices in large metropolitan areas (…),” according to the IMF’s economic report on Finland.

More specifically, it says that “House prices have risen the fastest in metropolitan areas. The pace of house price growth has been pronounced in Helsinki and other highly developed areas despite the crisis, but less so in other regions, especially where there have been declines in manufacturing and industry. Similar dynamics are evident in the relative prices of smaller dwellings compared to larger properties or detached homes, underscoring the upward pressures on house prices in highly populated areas.” The report also talks about macroprudential policies, read the full report here.

“(…) the level of overvaluation [in house prices in Finland] is lower than in other Nordic countries. However, the national average conceals rapid growth in prices in large metropolitan areas (…),” according to the IMF’s economic report on Finland.

More specifically, it says that “House prices have risen the fastest in metropolitan areas. The pace of house price growth has been pronounced in Helsinki and other highly developed areas despite the crisis,

Posted by at 8:01 PM

Labels: Global Housing Watch

House Prices in Colombia

“House prices rose significantly in recent years, fuelled by a robust expansion of income and credit growth and government subsidies. If prices were to fall, banks’ non-performing loans could increase. However, the risk is mitigated by low households’ loan-to-value ratios (about 55 percent), fixed borrowing rates, and a low exposure of banks to mortgage loans. High growth in credit to the private sector, including consumer loans, has been a concern in recent years (IMF Country Report 13/35), but has been abating,” says IMF’s annual economic report on Colombia.

“House prices rose significantly in recent years, fuelled by a robust expansion of income and credit growth and government subsidies. If prices were to fall, banks’ non-performing loans could increase. However, the risk is mitigated by low households’ loan-to-value ratios (about 55 percent), fixed borrowing rates, and a low exposure of banks to mortgage loans. High growth in credit to the private sector, including consumer loans, has been a concern in recent years (IMF Country Report 13/35), but has been abating,”

Posted by at 4:25 PM

Labels: Global Housing Watch

Saturday, May 24, 2014

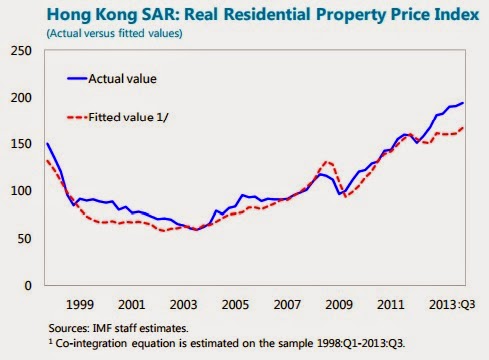

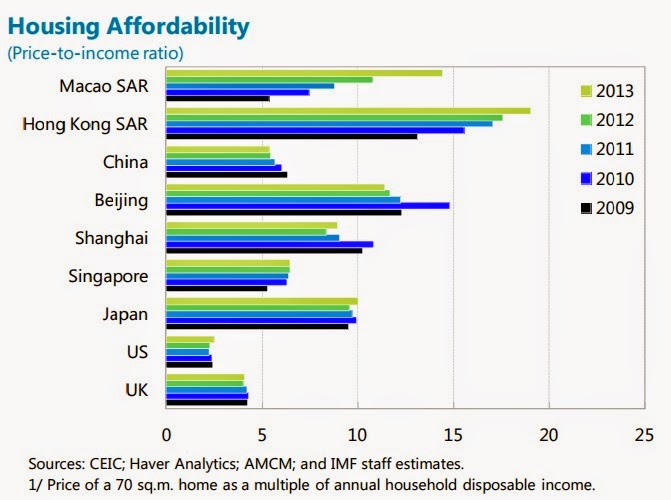

House Prices in Hong Kong

“Property prices have increased some 300 percent from their trough in 2003. While prices have leveled off more recently, estimates from [IMF] staff models suggest they could be higher than suggested by fundamentals. (…) a disorderly correction, resulting from, for example, global market volatility or domestic shock, remains a key risk as an abrupt downturn in prices could trigger an adverse feedback loop between economic activity, bank lending, household balance sheets, and the property market.” says the new IMF’s economic report on Hong Kong.

“Property prices have increased some 300 percent from their trough in 2003. While prices have leveled off more recently, estimates from [IMF] staff models suggest they could be higher than suggested by fundamentals. (…) a disorderly correction, resulting from, for example, global market volatility or domestic shock, remains a key risk as an abrupt downturn in prices could trigger an adverse feedback loop between economic activity, bank lending, household balance sheets, and the property market.” says the new IMF’s economic report on Hong Kong.

Posted by at 1:18 PM

Labels: Global Housing Watch

Friday, May 9, 2014

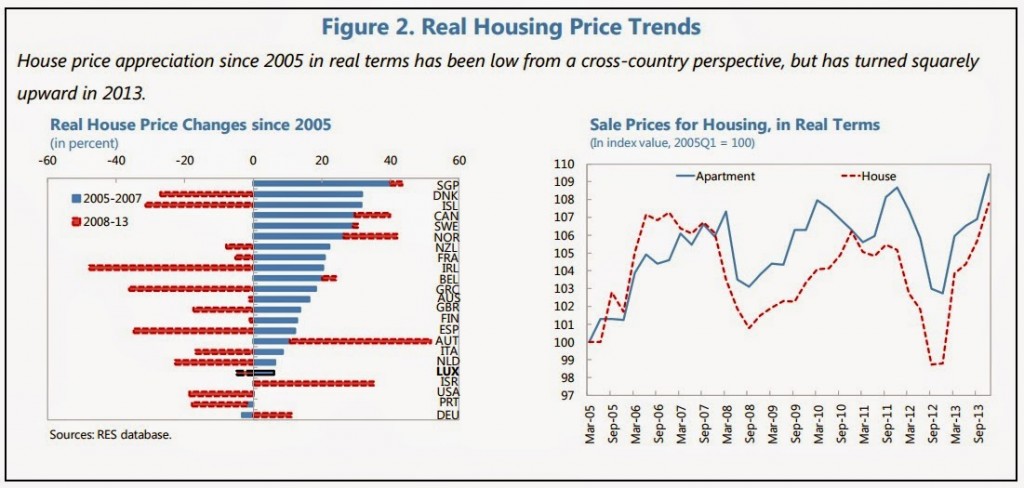

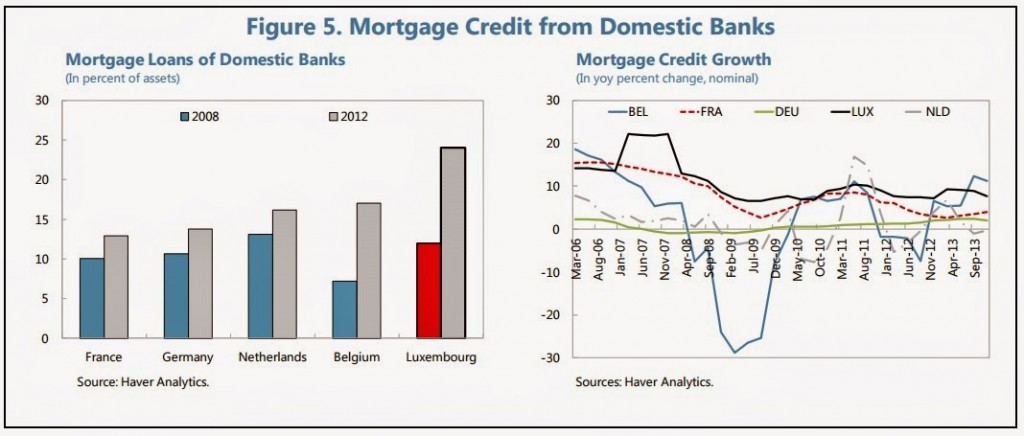

House Prices in Luxembourg

“Without policy action, underlying forces for housing price appreciation will likely persist (…) Prices do not appear overvalued at this time, though they have recently picked up (…) Banks’ increased exposure to mortgages bears vigilance, and buffers should be maintained. The tightening in the risk weights for LTVs above a certain level for banks, and the capital surcharge for domestically-oriented banks, are appropriate. If these measures are found to be insufficient after some period of observation, further steps may be needed (…) Government policies should become more neutral in relation to home ownership vs. renting. Current policies provide incentives for ownership, spurring demand pressures further”–these are the main points from the overall assessment of a new IMF study on Luxembourg’s housing market.

“Without policy action, underlying forces for housing price appreciation will likely persist (…) Prices do not appear overvalued at this time, though they have recently picked up (…) Banks’ increased exposure to mortgages bears vigilance, and buffers should be maintained. The tightening in the risk weights for LTVs above a certain level for banks, and the capital surcharge for domestically-oriented banks, are appropriate. If these measures are found to be insufficient after some period of observation,

Posted by at 6:21 PM

Labels: Global Housing Watch

Subscribe to: Posts