Showing posts with label Global Housing Watch. Show all posts

Thursday, January 29, 2015

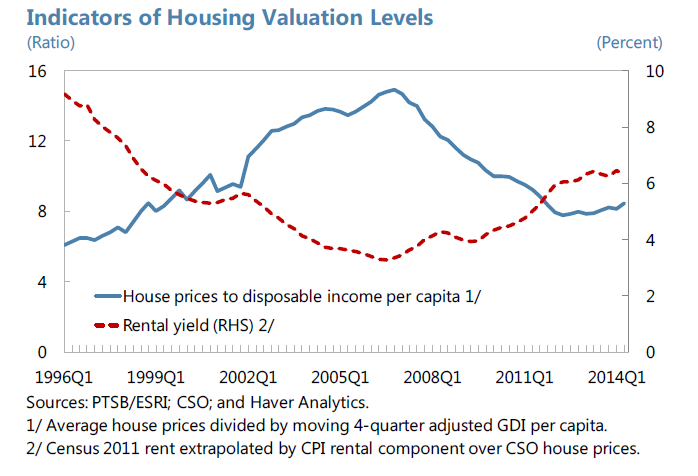

House Prices in Ireland

“Property values are up sharply, though valuation risks are not yet evident, and mortgage lending is beginning to rise from a low base. National housing prices rose 16.3 percent y/y in October, with Dublin prices surging 24.2 percent y/y, though they remain 38 percent below their pre crisis peak. New mortgage loans grew about 50 percent y/y in Q3 2014, from a low base, with about half of all residential property transactions in cash. Residential rents are also rising, and house price ratios to rents and incomes do not yet signal valuation concerns. Read the full article…

Posted by at 11:12 PM

Labels: Global Housing Watch

Tuesday, January 20, 2015

State of Housing Markets Across the Globe

Here is my presentation on the IMF’s Global Housing Watch and the state of housing markets across the globe that I gave at the International Housing Association Conference. Also, see country specific presentations that were given by other participants at the conference: Australia, Canada, Japan, Nigeria, Norway, and the United States. And here is the link to the agenda. Read the full article…

Posted by at 3:24 AM

Labels: Global Housing Watch

Wednesday, January 7, 2015

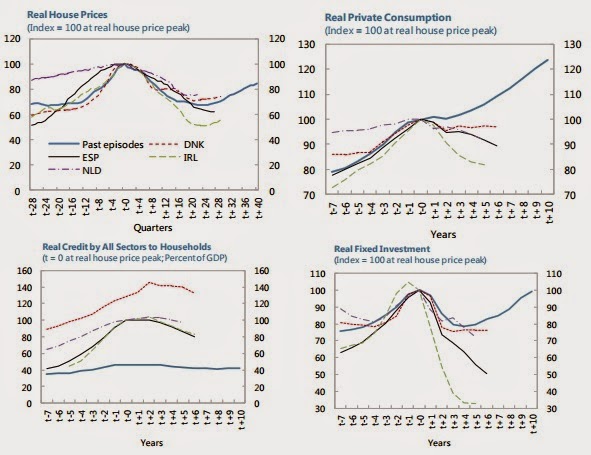

Housing Recoveries: Denmark, Ireland, Netherlands and Spain

Also, read an iMFdirect blog post on the report here.

A new report by the IMF “(…) examines the experiences of Denmark, Ireland, the Netherlands, and Spain—four countries in which the house-price cycle has been especially large and that share a similar institutional environment (a common monetary policy and the EU’s institutional framework)—with a view to exploring how policies can best support economic recovery in the wake of a house-price bust. (…) These countries’ experiences share similarities, but also important differences. Shocks to house prices, unemployment, Read the full article…

Posted by at 7:27 PM

Labels: Global Housing Watch

Friday, December 19, 2014

House Prices in Georgia

“Despite an overall positive outlook, there are several key macroeconomic vulnerabilities that would impact the financial sector: (…) Sudden decline in asset prices. As more than half of domestic private credit is backed by real estate, continued increases in real estate prices toward the pre-collapse level in 2008 could become a source of vulnerability,” says a new IMF report on Georgia.

Posted by at 9:06 PM

Labels: Global Housing Watch

House Prices in Denmark

Moreover, the report says that “Danish household debt continues to be the highest among the OECD countries, in large part to finance housing wealth. Household debt has been always relatively high in Denmark, but it grew rapidly during the housing boom, facilitated by the introduction of deferred amortization loans in 2003, reaching about 300 percent of disposable income. On the other side of the balance sheet, household assets are also large with positive net worth. However, these assets consist mostly of illiquid mandatory pension accounts and housing, leaving households with limited liquid buffers and making them more vulnerable to interest rate shocks. The need to rebuild balance sheets has depressed private consumption, weighing on the recovery in recent years.” Continue reading here. Also, see a special note on the mortgage finance system here.

“Danish house prices bottomed out and have recently started to pick up gradually. From the 2007 peak to the 2012 bottom, real house price dropped by about 30 percent. Real house prices started to rise in 2013 and grew 2.6 percent (y/y) in the second quarter of 2014 even though the pace of house price recovery varies across regions and types of housing (e.g., a stronger recovery in the prices of owner occupied flats in the Copenhagen area). Staff estimates based on three different metrics (price-to income ratio, Read the full article…

Posted by at 8:45 PM

Labels: Global Housing Watch

Subscribe to: Posts