Showing posts with label Global Housing Watch. Show all posts

Monday, July 27, 2015

On the Globalization of Real Estate and its Consequences

Speech delivered by Prakash Loungani

Advisor, Research Department at the IMF

2015 Global Real Estate Summit in Washington DC

July 8, 2015

Good afternoon. I am grateful to Professor Ko Wang of Johns Hopkins University for putting together this plenary session. And I welcome the many real estate associations—including the Global Chinese Real Estate Congress—that have come together to make this a truly unique event.

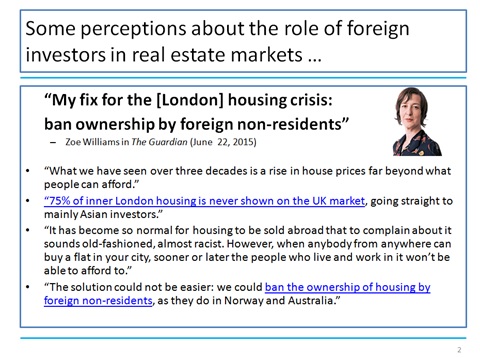

My remarks will focus on one aspect of the globalization of real estate markets, namely the role of foreign investors. We see frequent discussions of this in the media. For example, here is a recent column by Zoe Williams of The Guardian (Slide 2).

- She complains that UK house prices—in London but also elsewhere—are “far beyond what people can afford” and that this is partly because houses are “going straight to mainly Asian investors”.

- She worries that “when anybody from anywhere can buy a flat in your city, sooner or later the people who live and work in it won’t be able to afford to” and proposes the simple solution that the UK “ban the ownership of housing by foreign non-residents”.

What do we know about the role that foreign investors are playing in real estate markets? Anecdotally, there is indeed an increased role of foreign investors. It appears to be driven by three factors.

- First, there has been an immense increase in wealth, particularly in emerging market economies.

- Second, interest rates area at historical lows around much of the world, prompting a search for yield among other investments.

- Third, in a few cases, increased geo-political risks are leading to safe haven flows to particular property markets. For instance, some research shows that has house price increases in London are correlated with increased political risk, which the authors argue drives capital inflows into real estate markets.

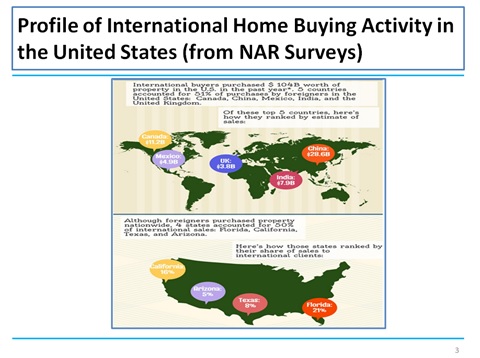

For the United States, we have a fair bit of survey evidence from the National Association of Realtors on the extent of foreign investments in real estate. These surveys reveal the following:

- Foreign buyers accounted for over $100 billion of existing home sales, which is about 8 percent of the dollar volume of existing home sales and about 4 percent of the number of existing home sales. Of course, this means that foreign buyers are a more upscale group than domestic buyers: they buy houses with an average value of $500,000—twice the average value of a home sold to a domestic buyer.

- Four U.S. states accounted for half of the sales to foreign buyers: Florida, California, Texas, and Arizona. About half of the foreign buyers came from five countries: Canada, China, Mexico, India, and the United Kingdom (Slide 3).

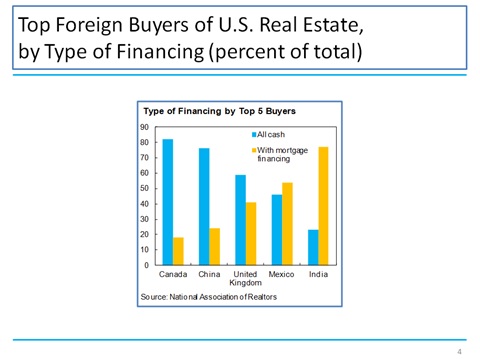

Just over half of the purchases by foreign buyers are all-cash purchases. Nationally, about 25 percent of existing home sales are all-cash purchases, with the remainder involving some form of mortgage financing. In contrast, about 55 percent of reported transactions with foreign buyers were all-cash sales (Slide 4).

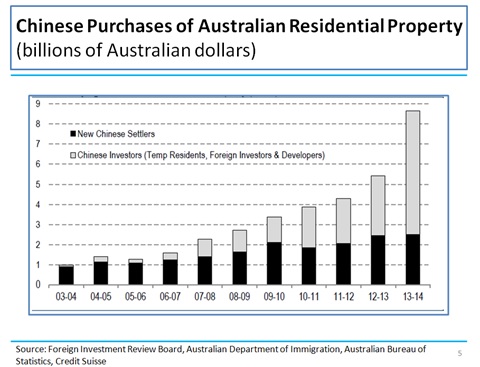

While I have focused on the United States, there is also data available for a few other countries, such as Australia (Slide 5), which are the major destinations for foreign real estate investment.

The increases in foreign real estate investment present both opportunities and challenges. Housing has often been regarded as a prime example of a ‘non-traded’ good. As economists, we should welcome the increased opportunities for trade in housing, much as we would welcome any other form of international trade.

However, we also know from experience that the benefits of trade come with some short-run challenges. Let me mention a couple. The first is that, as in other forms of international trade, there are winners and losers from the increased trade in housing. In this case, the losers are often domestic buyers who could be getting shut out of particular property markets which are attractive to foreign buyers. Certainly we see many media reports of this kind as I noted at the outset of my remarks with the example from The Guardian. In some cases, the negative perceptions about foreign buyers are reinforced by allegations of fraudulent behavior. For instance, in Australia, foreign buyers are only permitted to buy new rather than existing residential property. But allegations of foreign buyers circumventing this rule have led the Australian government are to increase monitoring of foreign investment—including increased fines for those found to be in non-compliance—and an increase in application fees for foreign acquisitions to fund the additional monitoring.

We should take concerns about the possible short-run adverse effects of the globalization of real seriously. This is both the fair and pragmatic thing to do. At the same time, we should remind people of the long-term benefits from increased trade, and indeed even the short-run benefits. Consider the case of Spain. As is well-known, an over-investment in real estate was a source of the crisis in that country. But there may have been an over-correction as well, leading to a housing market that was too depressed relative to potential. But now, reports suggest that foreign investors are helping to drive a welcome recovery of Spain’s housing market.

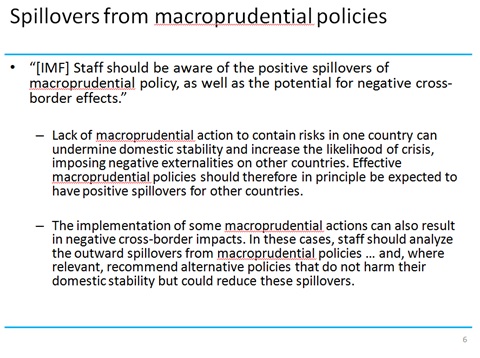

The second challenge that foreign buyers can pose is to the conduct of macroprudential policy. In many countries, macroprudential tools have been used to contain housing booms. The most common tools are limits on loan-to-value (LTV) ratios and debt-to-income (DTI) ratios. Evidence thus far suggests that these measures are somewhat effective in cooling off both house prices and credit growth in the short run. However, as I noted earlier, many foreign purchases are cash-only transactions. Hence the limits on LTV and DTI ratios may not be effective against housing booms driven by increased housing demand from foreign cash inflows that bypass domestic credit intermediation. In such cases, other tools are needed. For instance, stamp duty has been imposed to cool down rising house prices in Hong Kong SAR and Singapore. Evidence shows that this fiscal tool did reduce demand from foreigners who were outside of the LTV and DTI regulatory perimeters. We may also need to consider what spillovers are generated from the presence of foreign investors and how to design macroprudential policies to deal with such spillovers (see Slide 6 for the general guidance given to IMF staff).

Global Housing Watch

Let me conclude with some remarks on recent developments in global housing markets and, given the interests of this audience, tell you a bit about the IMF’s views on housing markets in China.

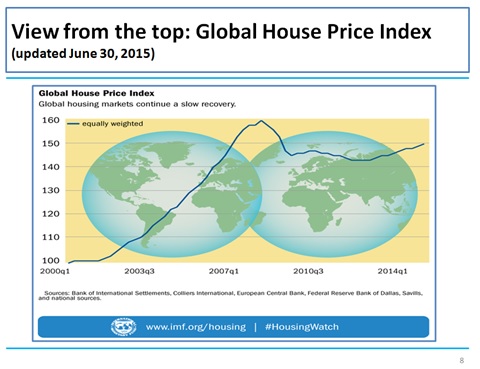

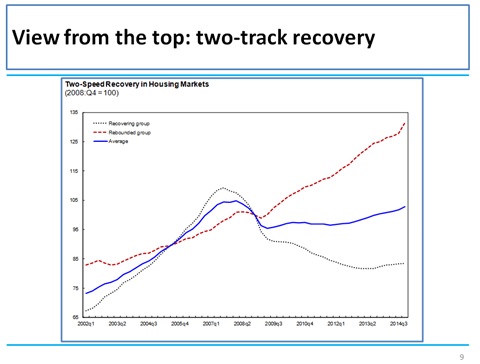

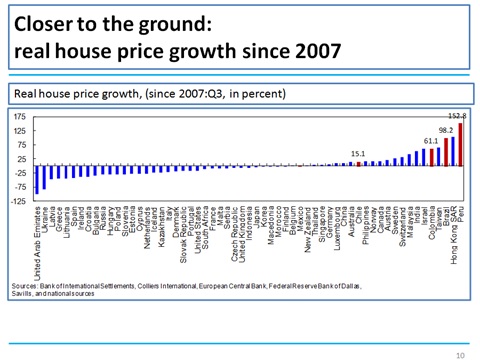

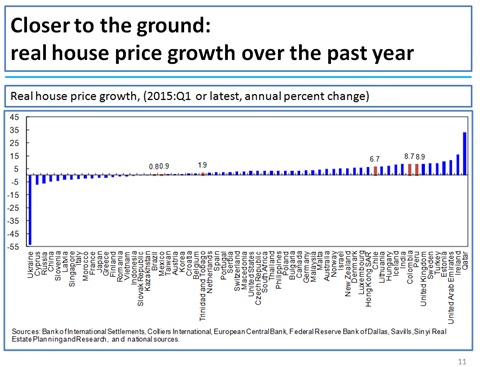

Our Global House Price Index has been inching up for over two years now (Slide 8). After a brief correction at the onset of the Great Recession, many countries have seen robust growth in house prices over the past eight years (Slide 9-11). These include advanced economies—such as Australia, Canada and Norway—and many emerging economies in Asia and Latin America.

Now this does not mean that house prices are over-valued in these countries. Detecting over-valuation in housing markets requires detailed analysis and judgment. As part of their annual economic analysis of each economy, the IMF staff often does an assessment of the housing sectors as well.

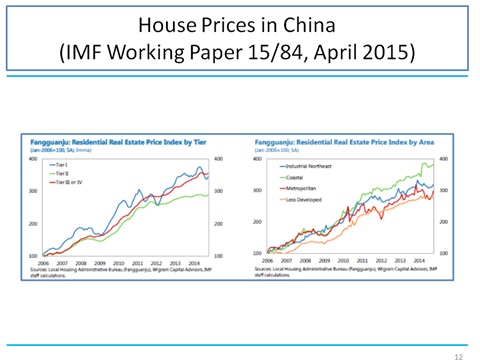

Many in this audience may be interested in our view of China’s housing market. Given the size of the country, we of course have to take a more granular look in this case, using city-level and provincial data. Our country team has provided a comprehensive analysis in a working paper released just a few months ago. They find that prices have been moderating at both the national level and across all city tiers. On average, Tier II and Tier III/IV cities have performed the weakest; across geographical areas, the industrial Northeast and the Coast are experiencing the weakest price development (Slide 12).

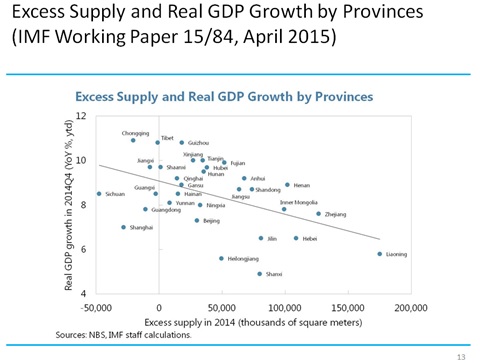

The softening in prices reflects overbuilding across many cities. Inventory indicators point to a risk that construction has run ahead of demand in some regions. Based on historical data, higher excess supply is usually associated with lower real GDP growth across provinces (Slide 13). The transmission channel is likely through a slowdown in real estate investment, which was a key driver of growth as excess supply built up.

An orderly unwinding of this excess supply would be welcome. It will free up resources that can be used more efficiently in other parts of the economy, helping China moving towards its goal of a new and sustainable growth model. The key will be to allow this adjustment to take place, while avoiding a too sharp of an economic slowdown.

Let me summarize:

- The global housing market has mounted a slow recovery overall. But the situation varies tremendously by country and calls for detailed country-level assessments. The IMF, as part of its annual economic reviews—our so-called Article IV consultations—has increasingly been carrying out such assessments. I provided an example of our analysis for China. Just this year alone, we have carried out assessments of housing markets in about 20 countries. I would recommend these reviews to you as a source of information and also to seek your feedback on how we can do better.

- The panel discussion today focuses appropriately on an important development, the growing globalization of real estate markets. Like other forms of trade, this will confer long-term benefits. But, as I have argued, we need to be attentive to the short-run costs, particularly those imposed on some domestic buyers, and on the increased challenges for macroprudential policies.

Thank you.

Speech delivered by Prakash Loungani

Advisor, Research Department at the IMF

2015 Global Real Estate Summit in Washington DC

July 8, 2015

Good afternoon. I am grateful to Professor Ko Wang of Johns Hopkins University for putting together this plenary session. And I welcome the many real estate associations—including the Global Chinese Real Estate Congress—that have come together to make this a truly unique event.

My remarks will focus on one aspect of the globalization of real estate markets,

Posted by at 9:57 AM

Labels: Global Housing Watch

US Housing Market: An Update

Mortgage, fed funds rate, and access to credit. If you are thinking about taking out a mortgage, don’t obsess over the Fed—that’s the advice of Neil Irwin of the New York Times. Irwin says: “(…) even the most knowledgeable people about Fed policy get it wrong. I know of a guy whose insights into the Fed are better than almost anybody else’s. He refinanced his mortgage on a house in Washington in 2011, getting a 30-year fixed-rate mortgage at 4.25 percent. He should have waited a year. By late 2012, average rates were almost a full percentage point lower. But by then Ben Bernanke was stuck with his higher mortgage rate, and, presumably, a bit of regret.” On a separate note, Robert Shiller reminds us that the housing still isn’t rational (New York Times). On fed funds rate, in a recent remarks, Federal Reserve Chairwoman Janet Yellen signaled that the Fed is likely to raise its policy rate this year, assuming its forecasts for stronger growth and lower unemployment are realized. In contrast, an IMF report says that the Fed should delay policy rate rise until 2016. And on access to credit, the Urban Institute points out that access to credit is slowly increasing after years of post-crisis restriction.

Housing finance. “While a number of important steps have been taken to address the structural weaknesses exposed by the crisis in mortgage markets, comprehensive housing finance reform remains the largest piece of unfinished business. In particular, it is not clear when Fannie Mae and Freddie Mac will exit conservatorship and what an end point for a reformed housing finance system will look like. This creates not only fiscal but also financial risks: moral hazard from coverage of credit losses by the government or the government-sponsored enterprises, a distorted competitive landscape due to the dominant footprint of Fannie Mae and Freddie Mac, and large subsidies for homeownership that create incentives to take on excessive levels of household debt,” according to Deniz Igan of the IMF.

Housing market activity. On the demand front, Redfin’s new Housing Demand Index rose 13 percent in June compared to last year. Currently, the national breakeven horizon on a typical home for buyers making the median income is a little less than two years, according to Zillow. On the supply front, there is a general consensus that housing supply is tight. Bidding wars are making a comeback in a number of metro areas across the US due to a market short of homes for sale, notes the Wall Street Journal. Moreover, the lack of supply varies across the different segments. An acute lack of construction at the lower end of the housing market is creating a tight supply, driving up rents and pushing up prices of affordable homes to levels reached in 2006, says the Financial Times. On the sentiment front, home builders recently reported their highest level of satisfaction with the real estate market since 2005 (NAHB).

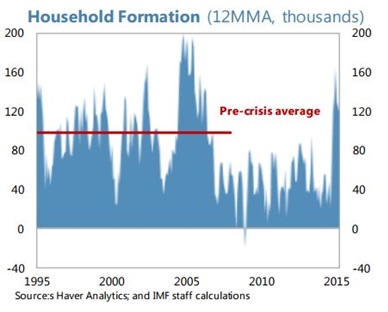

A new long-term housing equilibrium. According to an IMF report: “Up until recently, household formation has been depressed despite the potential for pent-up demand from demographics and more secure job prospects. The slow return of millennials to the first-time home buyers market could signal a preference shift away from traditional suburban, owner-occupied housing. Indeed, the urban rental market remains strong which could represent an enduring increase in demand for multi-family housing units with a smaller square footage. If true, this would permanently lower the steady state growth contribution from residential construction. A less concerning interpretation comes from household surveys, which suggest that attitudes to home ownership haven’t changed much: most renters would prefer to own if they had the necessary financial resources. If that were true, once the job market improves further and millennials have paid off some of their student loans (which have grown to over US$1 trillion or 7½ percent of GDP), the demand for housing could quickly revert to previous norms, with an accompanying step-up in residential investment.”

A new long-term housing equilibrium. According to an IMF report: “Up until recently, household formation has been depressed despite the potential for pent-up demand from demographics and more secure job prospects. The slow return of millennials to the first-time home buyers market could signal a preference shift away from traditional suburban, owner-occupied housing. Indeed, the urban rental market remains strong which could represent an enduring increase in demand for multi-family housing units with a smaller square footage. If true, this would permanently lower the steady state growth contribution from residential construction. A less concerning interpretation comes from household surveys, which suggest that attitudes to home ownership haven’t changed much: most renters would prefer to own if they had the necessary financial resources. If that were true, once the job market improves further and millennials have paid off some of their student loans (which have grown to over US$1 trillion or 7½ percent of GDP), the demand for housing could quickly revert to previous norms, with an accompanying step-up in residential investment.”

Rental market. The single-family rental market has enjoyed a strong run due to the foreclosure crisis and declining homeownership, according to Mark Zandi and Adam Kamins (both at Moody’s Analytics). In the long run, the rental market is also likely to remain strong. While the millennial generation born after 1980 has driven demand for apartments in recent years, baby boomers — those born from 1946 to 1964 — will be the next wave, pushing up rents and spurring construction of more multifamily housing, according to Jordan Rappaport (Federal Reserve Bank of Kansas City). There is also anecdotal evidence that developers are building few new units as demand is hit by post-crisis rules on condo mortgages (Wall Street Journal).

Debate on the causes of the recent housing crash continues. New research has focused on the reported income for mortgage loans (income reported in mortgage applications vs. income reported on tax returns). A second study from Manuel Adelino, Antoinette Schoar, and Felipe Severino finds that the results in the first study are not driven by fraudulent income overstatement as argued by Mian and Sufi. Adelino, Schoar, and Severino’s new paper show that there was no decoupling of mortgage growth from income growth at origination over the 2002 to 2006 period. Instead, their results document that mortgage debt at origination grew proportionally across the income distribution, and especially middle- and high-income and borrowers with a FICO score above 660 represented a larger share of defaults once the crisis hit. These results are hard to reconcile with the earlier view of the crisis that unprecedented levels of lending to low income and low credit score neighborhoods set off the crisis.

From the Global Housing Watch Newsletter: July 2015

Below is a snapshot of what the experts are saying about the different issues of the US housing market.

Mortgage, fed funds rate, and access to credit. If you are thinking about taking out a mortgage, don’t obsess over the Fed—that’s the advice of Neil Irwin of the New York Times. Irwin says: “(…) even the most knowledgeable people about Fed policy get it wrong.

Posted by at 9:53 AM

Labels: Global Housing Watch

Thursday, July 23, 2015

House Prices in Czech Republic

“(…) real estate prices continue their mild recovery”, says IMF report on Czech Republic.

Posted by at 3:03 PM

Labels: Global Housing Watch

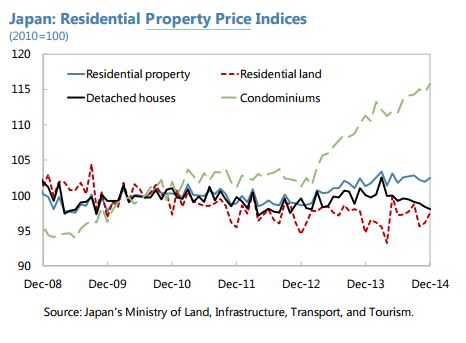

House Prices in Japan

“Land and real estate prices have bottomed out in most market segments and condominium prices in metropolitan areas are rising again after a two-decade slump,” notes the IMF report on Japan.

Posted by at 2:56 PM

Labels: Global Housing Watch

Monday, July 20, 2015

LTV and DTI Limits—Going Granular

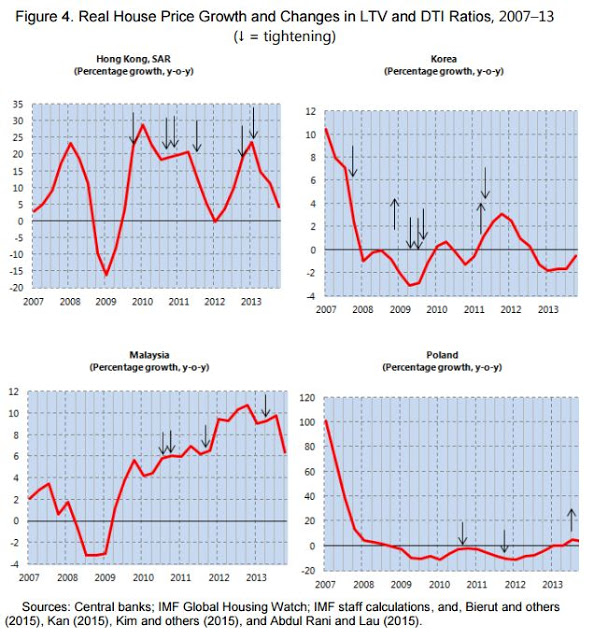

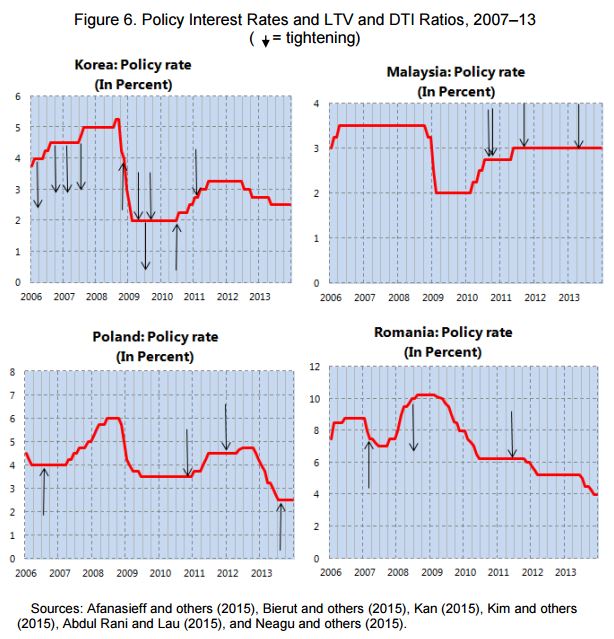

A new IMF paper by Luis I. Jácome and Srobona Mitra looks at how loan-to-value (LTV) and debt-service-to-income (DTI) limits work in practice (Brazil, Hong Kong SAR, Korea, Malaysia, Poland, and Romania). The authors find that “(…) rapid growth in high-LTV loans with long maturities or in the number of borrowers with multiple mortgages can be signs of build up in systemic risk; monitoring nonperforming loans by loan characteristics can help in calibrating changes in the LTV and DTI limits; Read the full article…

Posted by at 6:26 PM

Labels: Global Housing Watch

Subscribe to: Posts