Showing posts with label Global Housing Watch. Show all posts

Tuesday, April 7, 2015

House Prices in the United States

The National Association of Realtors takes a look at single-family median home prices in metro areas of 16 teams playing baseball Opening Day on April 6, 2015.

Posted by at 6:28 PM

Labels: Global Housing Watch

Thursday, April 2, 2015

House Prices in Qatar

- While the total number of real estate transactions has decreased from the 2013 peak, the total value of real estate transactions has dramatically increased, reflecting higher average prices and compositional changes.

- Land prices appear to have increased at the fastest pace, followed by villas where land is typically the most important cost component. Price increases have been slower for apartments and villas with extension (e.g., a guest house).

- While the Doha market experienced intermittent price hikes, price growth was recently strongest outside of Doha, given development projects and urbanization. For example, prices in Al Wakrah, a previously underdeveloped neighbor to Doha, have notably risen over the past year in light of its proximity to the new Hamad International Airport and the planned Doha Expressway route. Al Daayen has similarly experienced rapid price growth, due in part to its proximity to Lusail City and various 2022 World Cup projects.”

“Real estate prices accelerated last year, despite the sharp drop in oil prices,” according to the IMF’s latest annual report on Qatar. The report points out that “price growth gathered speed especially in the second half of 2014, with the December real estate values up by 35 percent year-on-year. Staff calculations based on transaction-level data from the Ministry of Justice point to the following broad trends:

- While the total number of real estate transactions has decreased from the 2013 peak,

Posted by at 5:15 PM

Labels: Global Housing Watch

Tuesday, March 31, 2015

Global Housing Watch Newsletter

- The Newsletter has an interview with Lars Svensson on when and how to deal with housing booms. Svensson lays out the policy options with his characteristic clarity. Read the full interview and the newsletter here.

- The Quarterly Update shows why averages can sometimes be misleading—the Global House Price Index shown on the first page continues a slow and boring uptick, but turn the page and you see it’s a story of two very different halves. Read the full note here.

- The Newsletter has an interview with Lars Svensson on when and how to deal with housing booms. Svensson lays out the policy options with his characteristic clarity. Read the full interview and the newsletter here.

- The Quarterly Update shows why averages can sometimes be misleading—the Global House Price Index shown on the first page continues a slow and boring uptick,

Posted by at 2:17 PM

Labels: Global Housing Watch

Saturday, March 28, 2015

House prices in Ireland

The latest IMF report for Ireland says: “Property markets are bouncing back rapidly. Commercial real estate values are up 30.7 percent y/y in 2014, though they still remain about 30 percent below pre-boom levels. Values were bolstered by record transaction volumes with over one-third reflecting foreign investment inflows. At the same time, house prices rose 16.3 percent y/y, as fast as the increases during the boom period, though they are still 38 percent below peak.”

Posted by at 1:04 AM

Labels: Global Housing Watch

Saturday, March 21, 2015

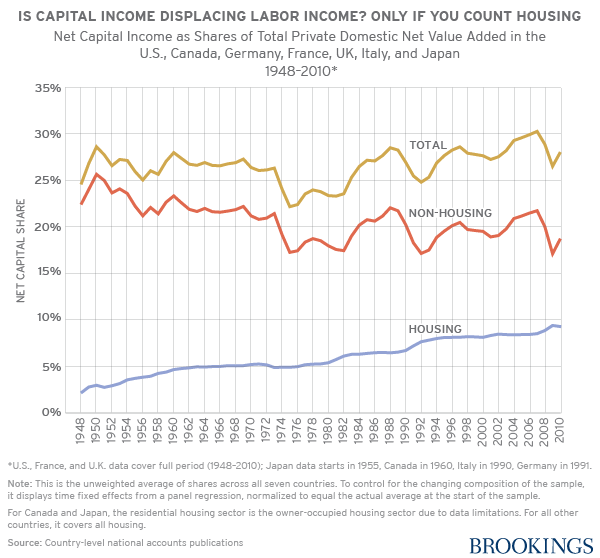

Housing Wealth and Inequality

Beyond housing, the results in this paper suggest that concern about inequality should be shifted away from the split between capital and labor, and toward other aspects of distribution, such as the within-labor distribution of income. Although the net capital share has at times seen dramatic shifts both up and down, away from housing its long-term movement has been quite small, and there is not strong reason to suspect that this pattern will change going forward.”

Matt Rognlie concludes: “Housing has a pivotal role in the modern story of income distribution. Since housing has relatively broad ownership, it does not conform to the traditional story of labor versus capital, nor can its growth be easily explained with many of the stories commonly proposed for the income split elsewhere in the economy—the bargaining power of labor, the growing role of technology, and so on.

Beyond housing, the results in this paper suggest that concern about inequality should be shifted away from the split between capital and labor,

Posted by at 7:55 PM

Labels: Global Housing Watch

Subscribe to: Posts