Showing posts with label Global Housing Watch. Show all posts

Wednesday, January 13, 2016

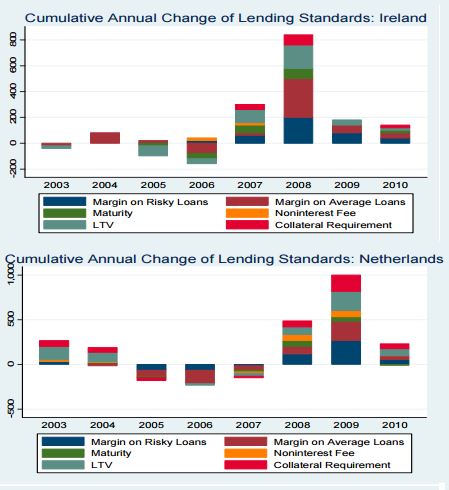

Effectiveness and Channels of Macroprudential Policies: Lessons from the Euro Area

A new IMF paper develops an analytical framework using bank lending survey data to investigate the effectiveness of macroprudential measures in containing housing booms in the euro area, the channels of transmission of such measures and their interaction with monetary policy.

The authors findings suggest that macro-prudential instruments targeting the cost of bank capital would be effective in slowing down mortgage credit growth, and given similar channels of transmission, would reinforce the impact of monetary policy tightening. Read the full article…

Posted by at 8:09 PM

Labels: Global Housing Watch

Wednesday, December 23, 2015

Understanding China’s Housing Market

For several years, analysts have been expressing concerns about China’s housing market. “Boom to bust: China’s property bubble is about to burst”—this was the headline of an article in the Economist magazine in 2008. Fast forward a few years and we continue to see similar headlines. “Haunted housing: Even big developers and state-owned newspapers are beginning to express fears of a property bubble”, in 2013. “End of the golden era: China’s property market is cooling off, at long last”, in 2014. These days, together with the housing market, analysts are also expressing concerns about the overall health of the Chinese economy. Here is one headline from 2015: “Coming down to earth: Chinese growth is losing altitude. Will it be a soft or hard landing?”

So why China’s housing market has not seen a bust yet? At last weekend’s conference in Shenzhen on December 18-19, leading experts on China’s housing market provided some answers. The conference—International Symposium on Housing and Financial Stability in China—was organized by the Chinese University of Hong Kong in Shenzhen, International Monetary Fund, and Princeton University.

Getting the facts right: housing and mortgage market

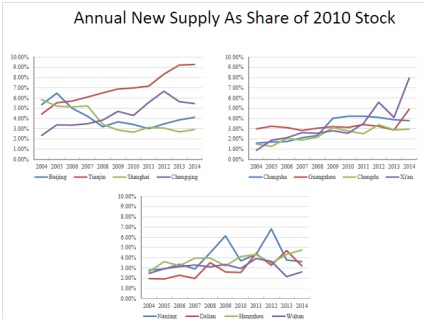

New research by Joe Gyourko (University of Pennsylvania) and his co-authors provides facts on China’s housing market from a supply and demand perspective. “In China, different housing markets behave very differently. A boom in Beijing and Shenzhen doesn’t mean a boom everywhere”, Gyourko said at the conference.

In his presentation, Gyourko made two key points. First point: there is substantial heterogeneity across cities in the balance between housing supply and demand. At one end, housing supply has outpaced demand in the interior part of the country. Specifically, housing supply has outpaced demand by at least 30 percent in twelve major markets and by 10 to 29 percent in another eight markets. On the other end, housing demand has outpaced supply in most major eastern markets. These include: Beijing, Hangzhou, Shanghai, and Shenzhen. Second point: markets such as Beijing, despite their strong measured fundamentals, should be considered somewhat risky because homes there trade at very high multiples of rent.

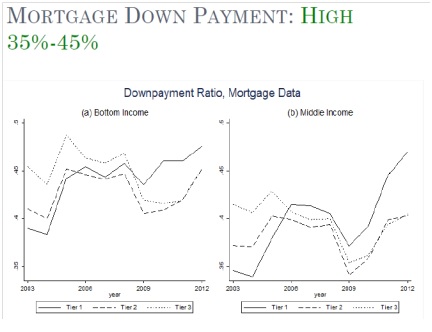

Another new piece of research, by Hanming Fang (University of Pennsylvania) and his co-authors, provides facts on China’s housing market from the mortgage market perspective. They have constructed a set of house price indices for 120 major cities in China and used a comprehensive data set of mortgage loans from 2003 to 2013. In his presentation, Fang showed that the Chinese housing boom has been accompanied by strong growth in income, and high mortgage down payments. For a decade, household’s disposable income has had an average annual real growth of 9 percent at the national level. Also, down payments have been over 30 percent on all mortgage loans.

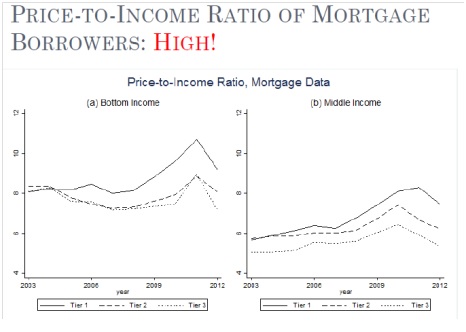

However, Fang noted that the participation of low-income home buyers in the housing boom has been characterized by high price-to-income ratios. The ratios are around eight in second and third tier cities, and even ten in first tier cities.

Haizhou Huang (CICC) provided very interesting facts on China’s housing market from the perspective of population in big cities. Huang pointed out that population concentrates into big cities. For example, in Japan and the United States, an increase in urbanization was accompanied by an increase in population concentration in big cities. So Huang expects that population concentration in China’s big cities will continue to rise. This could lead to more pressure on the housing market in Tier 1 cities. Huang asks: “Should China follow the European or Japanese model of few cities that have a large amount of the population?” China needs to develop more megacities, in his view. This could imply that the housing market could continue to grow and pressure in the housing market in tier I cities could decrease in the future.

Xiaobo Zhang (Peking University) talked the impact on China’s housing market from cultural traditions. “In rural areas of China, a new home is a necessary condition for marriage”, says Zhang. This is due in part by the sex ratio imbalance in China. Zhang showed that in 2000, 1 in 14 males could not marry. And in 2005, it was 1 in 10.

Assessing the risks: the role of expectations and local government debt

One area of risk is the role of expectations. Fang and Gyourko said that risks in Chinese housing market could arise with a shift in expectations. Specifically, Fang said that the willingness of low-income homebuyers to endure high price-to-income rations is explained by expectation of continued growth in income. However, the high expectation of future income growth may not be sustainable. Likewise, Gyourko said that a modest downward shift in expectations could generate sharp decline in house prices.

Moreover, Richard Koss (Global Housing Watch Initiative) compared how expectations have played an important role in the housing market in China and the United States. In both countries, expectations have played a role, but in different ways. Koss said that in the United States, expectations played a role in terms of house prices (e.g. expectations that house prices would continue rising), while in China, expectations play a role in terms of income growth (e.g. expectations that income will continue rising).

In the United States, said Koss, “No one thought house prices could fall as they never had on a nationwide basis, although specific regions suffered declines in the past. Americans thought they were special and that financial innovation would minimize risks but that turned out to be completely wrong.” So, in China, there could be risks in terms of irrational expectations of income growth.

Another area of risk is the local government debt and its linkage with the housing market. A new paper by Yongheng Deng (National University of Singapore) and his co-authors explores this link. At the conference, Deng noted that unlike local governments in western countries, local Chinese governments are prevented from directly issuing debt to fund mandated capital projects. Therefore, local governments tap into the growing housing market by selling public land to rise funding.

More specifically, future land sales revenue are used to repay the local government’s debt and land parcels are the most widely-used collateral for local government debt. This implies that “a substantial drop in housing or land prices may increase the risk level of local government debt, or even trigger a systematic default”, said Deng.

From the Global Housing Watch Newsletter: December 2015

For several years, analysts have been expressing concerns about China’s housing market. “Boom to bust: China’s property bubble is about to burst”—this was the headline of an article in the Economist magazine in 2008. Fast forward a few years and we continue to see similar headlines. “Haunted housing: Even big developers and state-owned newspapers are beginning to express fears of a property bubble”,

Posted by at 4:46 PM

Labels: Global Housing Watch

Wednesday, December 9, 2015

Housing Market in Kuwait

On the policy front, the report says that “Macroprudential tools can help mitigate potential risks posed by banks’ high exposures to the real estate sector. It is important to ensure that macroprudential policies are reviewed constantly to ensure that they do not exacerbate any property price correction, while preempting the buildup of excessive risks related to real estate exposures. (…) House price growth is a core indicator to monitor and the authorities should construct indices for residential properties as well as commercial properties. Also, other indicators, such as both the average and distribution of the LTV and DSTI (DSC) ratio, should be collected and analyzed to adjust macroprudential policy measures properly and swiftly.”

“Prices have shown some signs of softening (…) As of July 2015, prices across the residential and investment property segments have seen average prices fall in year-on-year terms by 6 and 7 percent, respectively (…). As residential prices began to fall in the first half of 2014, average investment property prices began increasing, rising by some 71 percent between March and September. After peaking in September 2014, average investment property prices have fallen by approximately 32 percent as of July 2015. Read the full article…

Posted by at 10:00 AM

Labels: Global Housing Watch

Monday, December 7, 2015

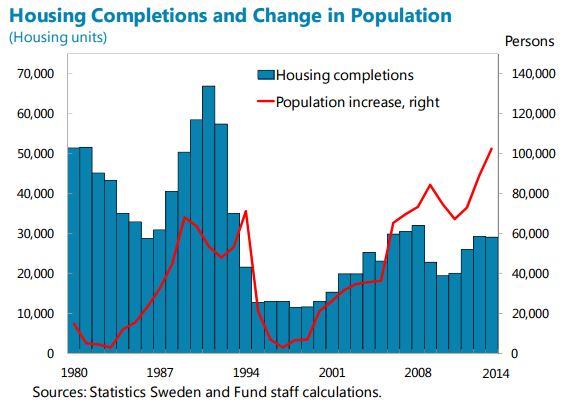

Sweden’s Housing Market

In terms of policies, the report recommends that:

- “Housing supply should be enhanced through land sale and planning reforms, which will also facilitate more competition in residential construction. Rent controls should be eliminated on new rental apartments and phased out more broadly.”

- “Mortgage interest deductibility should be phased out to moderate housing demand over time and limits on capital gains tax deferrals raised to release pent up supply.”

- “A debt-to-income limit should be adopted to contain rises in the already sizable share of highly indebted households, which adds to macroeconomic vulnerabilities.”

A separate IMF report looks at the role of supply constraints in driving prices of owner-occupied housing using municipal-level data.

“The housing market shows imbalances, with double-digit price gains as the urban population outpaces construction, pushing up household debt from already high levels. Dwelling price rises accelerated to 16 percent y/y in September, led by apartment price increases exceeding 20 percent in Stockholm and Gothenburg. Housing supply is constrained by construction impediments and rent controls while demand is bolstered by population growth and urbanization, rising income and financial savings, and historically low interest rates. Households need to borrow more at higher house prices, Read the full article…

Posted by at 10:00 AM

Labels: Global Housing Watch

Monday, November 30, 2015

Canada’s Housing Market: Which Way Now?

When looking at the national level, “moderate overvaluation is still observed (…). The inventory of completed and unsold units has trended higher and is above its historical average in large part because of the multi-unit segment”, says Canada Mortgage and Housing Corporation (CMHC). When looking at the local level, CHMC notes that there is “strong overall evidence of problematic conditions in Toronto, Winnipeg, Saskatoon and Regina. In Toronto, strong evidence of problematic conditions reflects a combination of price acceleration and overvaluation. Strong evidence of problematic conditions in Winnipeg, Saskatoon, and Regina reflects detection of overvaluation and overbuilding.” The divergence in Canada’s housing market is also pointed out by Scotiabank and the Canadian Real Estate Association. On developments in the west part of Canada, CMHC is expecting to see more homeowners fall behind in their mortgage payments as a prolonged slump in oil prices hit household budgets. Finally, the OECD recently released a report warning that the “newly completed but unoccupied housing units have soared in Toronto, increasing the risk of a sharp market correction.” However, Benjamin Tal at CIBC says that the most widely used data on unabsorbed units overstates and misrepresents the level of condo inventory.

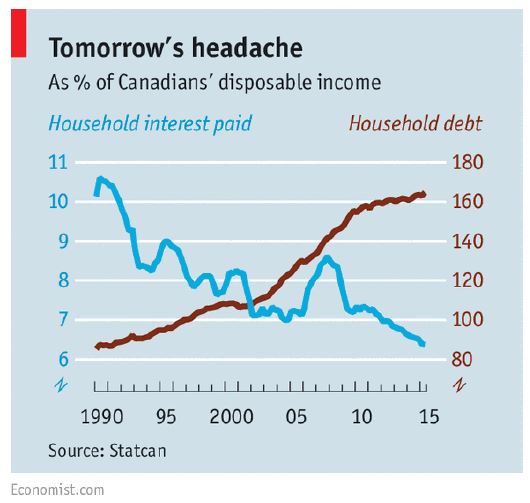

The views on household debt: “Consumer debt is a record 165% of disposable income. Most of that borrowing has gone into buying houses, which now look scarily overpriced”, says the Economist. TD Economics looked at the household debt issue in geographical terms. In doing so, TD Economics finds that “(…), financial vulnerability remains at elevated levels nationally. Households in British Columbia, Ontario and Alberta hold the top three spots, in that order. Households in these three provinces report having the highest debt-to-income ratios, devote the greatest share of income to making debt payments and have built up the highest degree of froth in their housing markets over the last decade.” Meanwhile, the Canadian Centre for Policy Alternatives looked at the household debt issues in terms of age group. It “(…) assesses the impact of a housing market correction on the net worth of Canadian families and finds a 20% decline in real estate prices would leave 169,000 families under 40 underwater, with more debts than assets.” However, the risk of household debt is not shared among the developers and builder community. A report by Ben Myers at Fortress Real Developments says: “The elevated level of household indebtedness in Canada is frequently cited as a vulnerability to the domestic economy, yet none of the builders and developers in our 2015 survey felt it was a significant risk to the housing market.” A new paper by the Central Bank of Canada finds “(…) that high and rising levels of both house prices and debt since the late-1990s can be mostly explained by movements in incomes, housing supply, mortgage interest rates and credit conditions, suggesting that the outlook for house prices and debt could depend mainly on the future paths of these variables.” A paper by Alan Walks (University of Toronto Mississauga) provides a picture of the emerging urban debtscape in Canadian cities, reflecting an essential element of the geography of risk and financialization. His research demonstrates that debt-related risk is associated with high and rising real estate values at each scale. Urban growth has thus brought with it significant new vulnerabilities, mainly related to housing costs and large mortgages, and this is particularly evident within Canada’s global cities.

Who is buying in the city of Vancouver? And how? New research by Andy Yan (Bing Thom Architects) looks at all the sales to occur within three west side neighborhoods in the City of Vancouver over a 6 month period and the ownership and mortgage patterns within these titles. There were a total of 172 transactions, with a total dwelling value of $525 million and with a starting price of $1.25 million and above. Here are some of the interesting findings: in terms of cash vs. mortgage, the study finds that 82 percent of the properties held a mortgage. In terms of ownership, 109 properties were listed with a single name and only 8 listed as corporation. In terms of occupations, 52 were listed as homemaker/housewife. And 66 percent of the 172 buyers had non-anglicized Chinese name. On a separate note, Tony Roy (BC Non-Profit Housing Association) says that nearly half of all renters are pouring more than 30 percent of their income into rent, while 24 percent in Metro Vancouver are spending more than half of their income on rent.

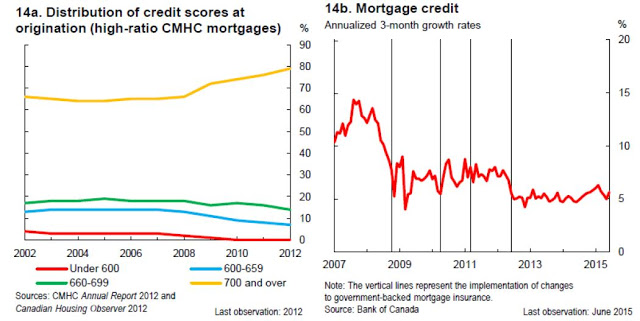

Macroprudential Policies: Are they working? More needed? According to the Central Bank of Canada, there have been four successive rounds of macroprudential tightening. The main target has been the rules for insured mortgages. For example, the maximum amortization period for insured loans has been shortened from 40 years to 25. Loan-to-value ratios have been lowered to 95 percent for new mortgages, and 80 percent for refinancing and investor properties. Qualification criteria such as limits on the total debt-service ratio and the gross debt-service ratio, as well as requirements for qualifying interest rates, have also been tightened.

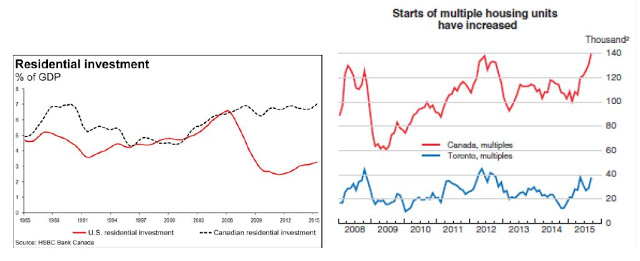

The measures taken have resulted in higher average credit scores, which have improved the quality of mortgage borrowing. With respect to household credit growth, the trend growth of mortgage credit declined from 14 percent in 2007–08 to around 5 percent in 2013–15. However, David Watt at HSBC Bank Canada says that there is a strong case for further macroprudential measures. He points out the trend in residential investment (see figure below on the left) and says that “the rise in residential investment as a percentage of GDP between 2002 and 2008 was in the backdrop of a generally rising terms of trade … With the terms of trade now worsening, it suggest that these trends should cool off, not accelerate.” Moreover, the OECD says that “(…) high household debt and strong price increases in some markets (single dwellings in Toronto and Vancouver) that are already expensive relative to fundamentals, further macro-prudential tightening on mortgage lending in these markets, such as maximum loan-to-value or debt-servicing ratios, should be implemented to ensure financial stability.”

From the Global Housing Watch Newsletter: November 2015

The views on the housing market: New research by National Bank Financial says that “There are now two housing markets in Canada.”

When looking at the national level, “moderate overvaluation is still observed (…). The inventory of completed and unsold units has trended higher and is above its historical average in large part because of the multi-unit segment”,

Posted by at 10:00 AM

Labels: Global Housing Watch

Subscribe to: Posts