Showing posts with label Global Housing Watch. Show all posts

Tuesday, April 11, 2017

A Closer Look at Global Housing

Posted by at 4:55 PM

Labels: Global Housing Watch

Monday, April 10, 2017

Housing Market in San Marino

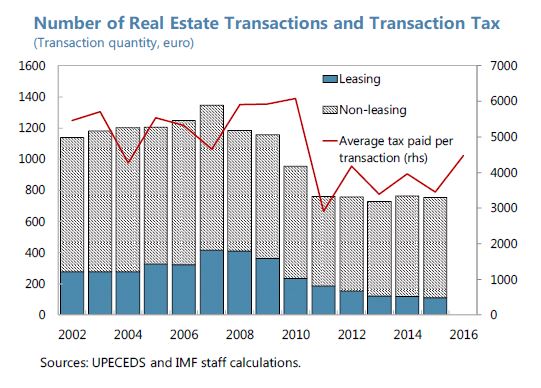

“Credit growth continues to be subdued, and activity in the housing market remains at the low level. (…) In the housing market, the number of real estate sales remains low, but the average tax per transaction for non-leasing properties, which is likely correlated with real estate prices, has stabilized”, says IMF report.

“Credit growth continues to be subdued, and activity in the housing market remains at the low level. (…) In the housing market, the number of real estate sales remains low, but the average tax per transaction for non-leasing properties, which is likely correlated with real estate prices, has stabilized”, says IMF report.

Posted by at 1:30 PM

Labels: Global Housing Watch

Monday, April 3, 2017

Housing Market in Netherlands

The IMF’s latest report on Netherlands points out the following:

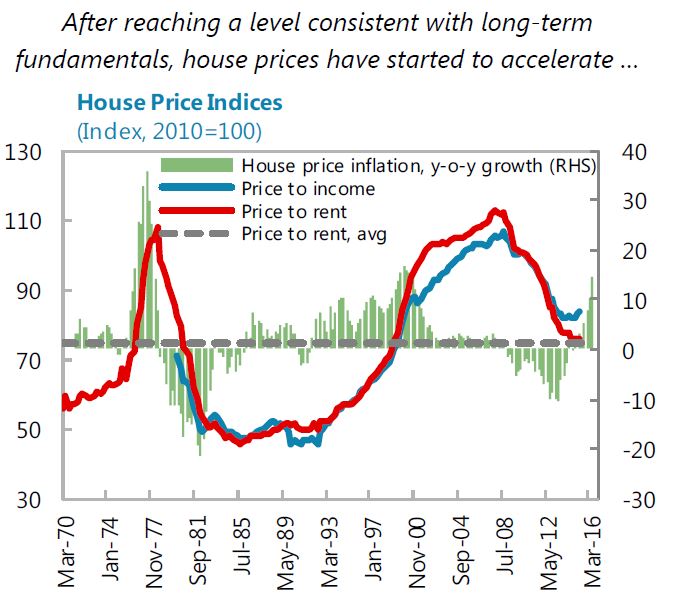

- “House prices have been accelerating and close monitoring may be warranted in the country’s main cities. After turning a corner in 2014, house prices have been steadily accelerating and transaction volumes have doubled in 2016. At the aggregate level, real house prices are broadly consistent with long-term equilibrium (priceto-income, price-to-rent ratios, Figure 3) but developments have been uneven across regions, with prices for apartments in Amsterdam 15 percent higher than a year ago. After plummeting by 20 percent during the crisis, commercial real estate has only started to recover recently.”

- “Households remain highly leveraged, with a sizeable share of mortgages in negative equity.”

- “Staff recommends accelerating the implementation of macro-prudential and other measures aimed at lessening household financial vulnerabilities. The authorities should build on recent initiatives, (…) They should accelerate the phasing down of mortgage interest deductibility (MID), by at least 1 percentage point per year ultimately bringing it to a neutral level relative to the taxation of other assets. (…) The authorities should continue to gradually lower the maximum limit on LTV ratios by at least 1 percentage point per year to no more than 90 percent by 2028 and to 80 percent thereafter. (…) The authorities should introduce prudential ceilings on debt service-to-income caps by income category that could not be relaxed during periods of strong growth.”

- “The private rental market needs to be deregulated and placed on a more even footing with owner-occupied homes and social housing.”

The IMF’s latest report on Netherlands points out the following:

- “House prices have been accelerating and close monitoring may be warranted in the country’s main cities. After turning a corner in 2014, house prices have been steadily accelerating and transaction volumes have doubled in 2016. At the aggregate level, real house prices are broadly consistent with long-term equilibrium (priceto-income, price-to-rent ratios, Figure 3) but developments have been uneven across regions,

Posted by at 2:32 PM

Labels: Global Housing Watch

Thursday, March 30, 2017

Das House-Kapital: A Long Term Housing & Macro Model

From a new IMF working paper:

“There are, by now, several long term, time series data sets on important housing & macro variables, such as land prices, house prices, and the housing wealth-to-income ratio. However, an appropriate theory that can be employed to think about such data and associated research questions has been lacking. We present a new housing & macro model that is designed specifically to analyze the long term. As an illustrative application, we demonstrate that the calibrated model replicates, with remarkable accuracy, the historical evolution of housing wealth (relative to income) after World War II and suggests a further considerable increase in the future. The model also accounts for the close connection of house prices to land prices in the data. We also compare our framework to the canonical housing & macro model, typically employed to analyze business cycles, and highlight the main differences.”

From a new IMF working paper:

“There are, by now, several long term, time series data sets on important housing & macro variables, such as land prices, house prices, and the housing wealth-to-income ratio. However, an appropriate theory that can be employed to think about such data and associated research questions has been lacking. We present a new housing & macro model that is designed specifically to analyze the long term.

Posted by at 6:17 PM

Labels: Global Housing Watch

Wednesday, March 29, 2017

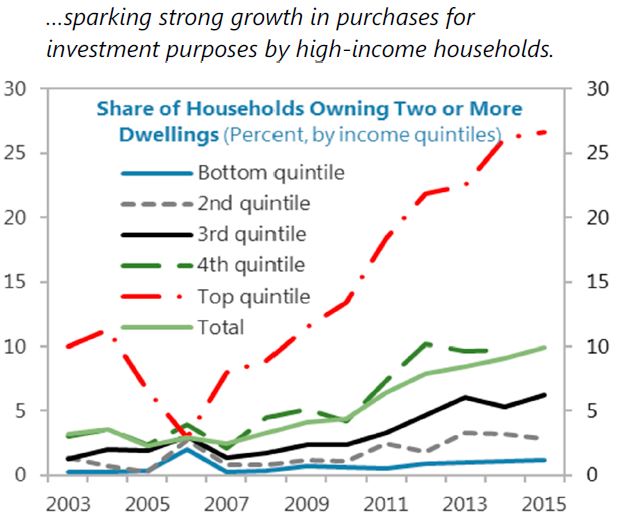

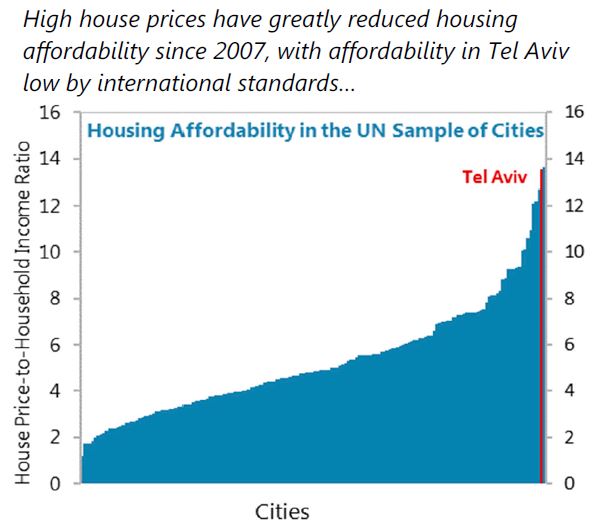

Housing Market in Israel

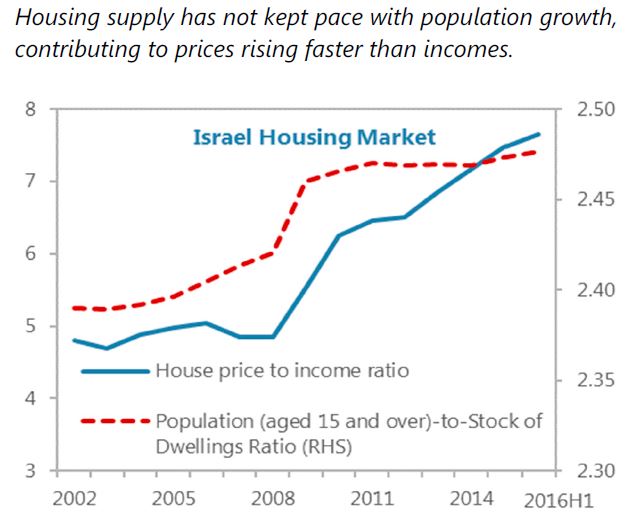

“Supply-side bottlenecks need to be addressed to improve housing affordability and contain macrofinancial risks. Housing prices are very high, posing a vulnerability while disproportionately affecting low-income households. Reforms should improve municipal incentives for development, ensure adequate land privatization and urban renewal, shorten approval times and reduce construction costs. Macroprudential policies are appropriately tight and the Bank of Israel should monitor developments closely”, says IMF’s latest report on Israel.

“Supply-side bottlenecks need to be addressed to improve housing affordability and contain macrofinancial risks. Housing prices are very high, posing a vulnerability while disproportionately affecting low-income households. Reforms should improve municipal incentives for development, ensure adequate land privatization and urban renewal, shorten approval times and reduce construction costs. Macroprudential policies are appropriately tight and the Bank of Israel should monitor developments closely”, says IMF’s latest report on Israel.

Posted by at 6:15 PM

Labels: Global Housing Watch

Subscribe to: Posts