Showing posts with label Global Housing Watch. Show all posts

Friday, October 20, 2017

Housing View – October 20, 2017

On cross-country:

- Risks in International Housing Markets – Reserve Bank of Australia

- Interest rates and house prices in the United States and around the world – Bank for International Settlements

- The State of Housing in the EU 2017 – Housing Europe

- Housing Markets: A European Perspective – Seeking Alpha

- Inclusive City Development: City-Wide Slum Upgrading and Housing Development – World Resource Institute

- International housing policies – CMHC

On the US:

- Paying For Dirt: Where Have Home Values Detached From Construction Costs? – BuildZoom

- First-Time Homebuyers: Toward a New Measure – Federal Reserve Bank of Philadelphia

- Don’t Worry About Inflation. Solve the Housing Shortage. – Bloomberg

- The Barriers Stopping Poor People From Moving to Better Jobs – The Atlantic

- How Historic Racial Injustices Still Impact Housing Today – Zillow

- Reducing Work Disincentives in the Housing Choice Voucher Program: Rent Reform Demonstration Baseline Report – U.S. Department of Housing and Urban Development

On other countries:

- [Canada] Canada’s Bank Regulator Toughens Mortgage Qualifying Rules – Bloomberg

- [Canada] Canadian housing agency says it can withstand severe downturn – Reuters

- [China] Chinese property boom props up Xi’s hopes for the economy – Financial Times

- [China] Chinese Cities Buy Off Housing Glut With Borrowed Money – Wall Street Journal

- [Hong Kong] Nano apartments rise to HK’s housing challenge – Financial Times

- [Sweden] Warning Signs Are Mounting for Sweden’s Once-Hot Housing Market – Bloomberg

- [Sweden] ‘The risks have definitely increased’ – Sweden’s housing boom wobbles – Financial Times

- [United Kingdom] Curbs on UK housing benefit making system ‘irrelevant’, IFS warns – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Risks in International Housing Markets – Reserve Bank of Australia

- Interest rates and house prices in the United States and around the world – Bank for International Settlements

- The State of Housing in the EU 2017 – Housing Europe

- Housing Markets: A European Perspective – Seeking Alpha

- Inclusive City Development: City-Wide Slum Upgrading and Housing Development – World Resource Institute

- International housing policies – CMHC

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, October 13, 2017

Housing View – October 13, 2017

On cross-country:

- Global urban house price index records slower growth – Knight Frank

- Global Residential Cities Index – Q2 2017 – Knight Frank

- The State of Housing in the EU 2017 – Housing Europe

- Transparent and efficient social housing – Housing Europe

On the US:

- Sixth annual AEI and CRN conference on housing risk – American Enterprise Institute

- Gentrification and the Amenity Value of Crime Reductions: Evidence from Rent Deregulation – NBER

- What happens to U.S. home prices after Fed rate increase? – Real Estate Decoded

On other countries:

- [Australia] Chinese Investors Keep Pouring Money Into Australian Housing – Bloomberg

- [Canada] Government Eyeing ‘All Options’ to Cool Vancouver Housing Market – Bloomberg

- [United Arab Emirates] Dubai: Premiums Under the Microscope – Reidin

Photo by Aliis Sinisalu

On cross-country:

- Global urban house price index records slower growth – Knight Frank

- Global Residential Cities Index – Q2 2017 – Knight Frank

- The State of Housing in the EU 2017 – Housing Europe

- Transparent and efficient social housing – Housing Europe

On the US:

- Sixth annual AEI and CRN conference on housing risk – American Enterprise Institute

- Gentrification and the Amenity Value of Crime Reductions: Evidence from Rent Deregulation – NBER

- What happens to U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, October 6, 2017

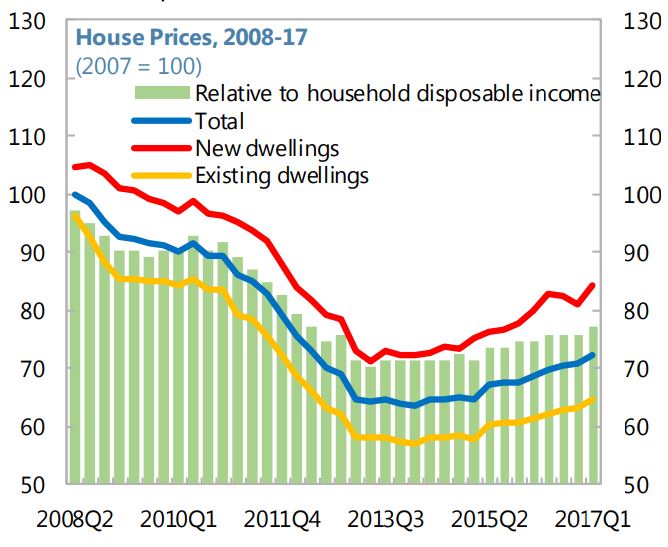

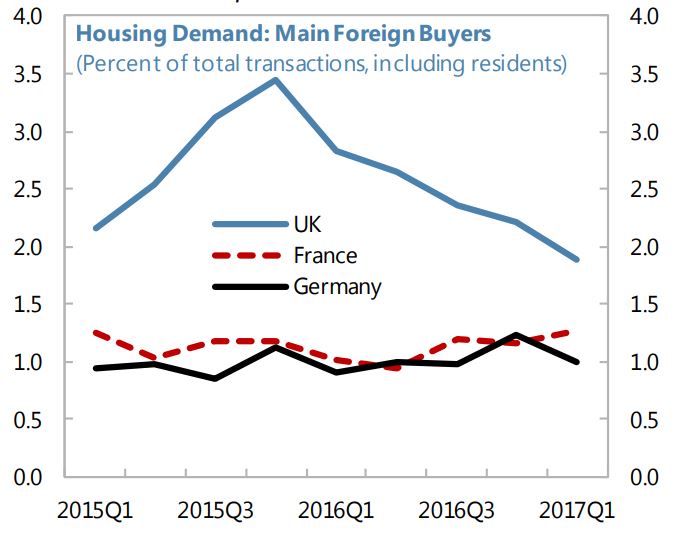

House Prices in Spain

The IMF’s latest report on Spain says that:

- “House prices have started to recover, but are still well below pre-crisis levels.”

- “UK citizens are also the main foreign buyers of houses, but their purchases declined in 2016.”

The IMF’s latest report on Spain says that:

- “House prices have started to recover, but are still well below pre-crisis levels.”

- “UK citizens are also the main foreign buyers of houses, but their purchases declined in 2016.”

Posted by at 11:46 AM

Labels: Global Housing Watch

Housing View – October 6, 2017

On cross-country:

- Finance and housing in Central and Eastern Europe – a demand-side approach – National Bank of Romania

- Affordable housing key for development and social equality, UN says on World Habitat Day – UN

- Quarterly Review of European Mortgage Markets Q2 2017 – European Covered Bond Council

- Hypostat 2017 – European Covered Bond Council

- Ownership rates in Europe – European Covered Bond Council

- Capital flows into European real estate are ‘developing not cooling’ – PropertyEU

On the US:

- The 2017 National Rental Housing Landscape – NYU Furman Center

- July 2017 Market Report: Almost Half of U.S. Homes Are Worth More Now Than Before the Bubble – Zillow

- 15 Favorites From Zillow Group Report on Consumer Housing Trends Report 2017 – Zillow

- A More Timely House Price Index – The Review of Economics and Statistics

- The real cause of the America’s housing bubble was foreign money – Financial Times

- The Negative (and Positive) Spillovers of Concentrated Foreclosure Activity in New York City – Harvard Joint Center for Housing Studies

- Overregulation Is the Main Block to Affordable Housing – Wall Street Journal

- Why Fall Should Be Hunting Season for Starter Home Buyers – Trulia

- Land-Use Regulations, Property Values, and Rents: Decomposing the Effects of the California Coastal Act – Federal Reserve Bank of Philadelphia

- Housing as a Safety Net – Urban Land Institute

- Housing as an Asset Class – Urban Land Institute

On other countries:

- [Canada] A novel approach to affordable housing in Canada – CMHC

- [Canada] Too Many Bedrooms, Not Enough Housing? – University of B.C.

- [China] China steps up battle against runaway property prices – Financial Times

- [Germany] Assessing Recent House Price Developments in Germany: An Overview – Monetary Policy, Financial Crises, and the Macroeconomy

- [Ireland] Irish House Price Report Q3 2017 – Daft.ie

- [Israel] A Housing Plunge Doesn’t Concern Israel’s Top Economic Adviser – Bloomberg

- [Macau] Macau’s amazing, incredible, soaring property prices – Global Property Guide

- [United Kingdom] Rent control could deepen the housing crisis in UK’s most expensive cities – Centre for Cities

- [United Kingdom] Britain’s Housing Crunch – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- Finance and housing in Central and Eastern Europe – a demand-side approach – National Bank of Romania

- Affordable housing key for development and social equality, UN says on World Habitat Day – UN

- Quarterly Review of European Mortgage Markets Q2 2017 – European Covered Bond Council

- Hypostat 2017 – European Covered Bond Council

- Ownership rates in Europe – European Covered Bond Council

- Capital flows into European real estate are ‘developing not cooling’

Posted by at 10:04 AM

Labels: Global Housing Watch

Friday, September 29, 2017

Housing View – September 29, 2017

On cross-country:

- Will house prices continue to rise forever? – ING

- Q2 2017: Europe’s boom continues, but sharp slowdown in the Middle East, Latin America, New Zealand and some parts of Asia – Global Property Guide

- Chinese Money Is Still Leaking Into the World’s Housing Markets – Bloomberg

- UBS Global Real Estate Bubble Index – UBS

On the US:

- Anti-vagrancy laws are not the best way to reduce homelessness – Economist

- Flood Risk Belief Heterogeneity and Coastal Home Price Dynamics: Going Under Water? – NBER

- Apartment Demand for the Next 15 Years: Can We Meet the Need? – U.S. Department of Housing and Urban Development

- 2017 Global Real Estate Portal Report – Mike DelPrete

- Pending Home Sales Dive: Economists Miss the Boat by Over 2 Percentage Points! – MishTalk

- Land Use Regulation and Good Intentions – Journal of Land Use & Environmental Law

On other countries:

- [Canada] 2017 Housing Finance Symposium – CMHC

- [China] Chinese property developers’ shares hit by new house sales curbs – Financial Times

- [China] Chinese Developers Plunge After Officials Tighten Housing Curbs – Bloomberg

- [France] Housing Europe expresses concern about the housing strategy presented by the French government – Housing Europe

- [Sweden] House price responses to a national property tax reform – SSRN

- [United Kingdom] Priced Out? The affordability crisis in London – The Progressive Policy Think Tank

- [United States] Policy changes make landlords wary of the UK housing market – Global Property Guide

On cross-country:

- Will house prices continue to rise forever? – ING

- Q2 2017: Europe’s boom continues, but sharp slowdown in the Middle East, Latin America, New Zealand and some parts of Asia – Global Property Guide

- Chinese Money Is Still Leaking Into the World’s Housing Markets – Bloomberg

- UBS Global Real Estate Bubble Index – UBS

On the US:

- Anti-vagrancy laws are not the best way to reduce homelessness – Economist

- Flood Risk Belief Heterogeneity and Coastal Home Price Dynamics: Going Under Water?

Posted by at 11:18 AM

Labels: Global Housing Watch

Subscribe to: Posts