Showing posts with label Global Housing Watch. Show all posts

Friday, January 12, 2018

Housing View – January 12, 2018

On cross-country:

- Q3 2017: Continued strong house price rises in Europe, Canada and parts of Asia, but globally housing markets are slowing sharply – Global Property Guide

- High house prices pose persistent risks in countries with housing markets slow to react to homeownership costs – Moody’s

- Real and financial cycles in EU countries: Stylised facts and modelling implications – European Central Bank

- Housing finance – International Growth Centre

- What if Real Estate Investors Are Looking at the Housing Market All Wrong? – Bloomberg

On the US:

- Pent-Up Demand and Continuing Price Increases: The Outlook for Housing in 2018 – Federal Reserve Bank of Kansas

- The Effects of Rent Control Expansion on Tenants, Landlords, and Inequality: Evidence from San Francisco – NBER

- The Housing Market Crash and Wealth Inequality in the U.S. – NBER

- Are Lemons Sold First? Dynamic Signaling in the Mortgage Market – NBER

- Portfolio Choice with House Value Misperception – Federal Reserve Bank of Boston

- The Impact of Interest Rates on House Prices and Housing Demand: Evidence from a Quasi-Experiment – American Enterprise Institute

- Housing Voucher Policy Designed to Expand Opportunity Targets Areas That Need It – Center on Budget and Policy Priorities

- Rent Control: Econ 101 Applies – Cato Institute

On other countries:

- [Brazil] No more roller coaster ride for Brazilian housing market? – Global Property Guide

- [Cambodia] Cambodia Finds New Target for Real Estate: Chinese Investors – New York Times

- [China] A Reexamination of Housing Price and Household Consumption in China: The Dual Role of Housing Consumption and Housing Investment – The Journal of Real Estate Finance and Economics

- [Germany] German house prices are accelerating! – Global Property Guide

- [Hungary] Property boom in Hungary continues in 2017 – Global Property Guide

- [India] Mumbai Home Prices Post First Drop in Decade Amid Modi Crackdown – Bloomberg

- [Ireland] Irish house prices will outpace all Europe over next 2 years – Global Property Guide

- [Italy] Italy an outlier as property prices continue to fall, data show – Financial Times

- [Montenegro] Montenegro’s housing market recovering, amidst booming tourism – Global Property Guide

- [Peru] House prices in Lima plunged in Q1 2017 – Global Property Guide

- [Thailand] Thailand’s housing market losing steam – Global Property Guide

- [Uruguay] House prices rising in Montevideo – Global Property Guide

Photo by Aliis Sinisalu

On cross-country:

- Q3 2017: Continued strong house price rises in Europe, Canada and parts of Asia, but globally housing markets are slowing sharply – Global Property Guide

- High house prices pose persistent risks in countries with housing markets slow to react to homeownership costs – Moody’s

- Real and financial cycles in EU countries: Stylised facts and modelling implications – European Central Bank

- Housing finance – International Growth Centre

- What if Real Estate Investors Are Looking at the Housing Market All Wrong?

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, January 5, 2018

Housing View – January 5, 2018 [2018 AEA Annual Meeting Special Edition]

On international house pricing:

- Measuring House Prices in the Long Run: Insights from Dublin, 1900-2015 – AEA

- A Tale of Two Countries: Comparing Booms, Busts and Bubbles in the United States and Chinese Housing Markets – Paper

- Analyzing the Changes in the Distribution of House Prices in Beijing – AEA

- Locally Weighted Quantile House Price Indices and Distribution in Japanese Cities, 1986 – AEA

- Do Airbnb Properties Affect House Prices? – Paper

- The Sharing Economy and Housing Affordability: Evidence from Airbnb – Paper

- Think Globally, Aggregate Locally: Index Consistency in the Presence Asymmetric Appreciation – Paper

- S. Metropolitan House Price Dynamics – Paper

- Did Investors Price Regional Housing Bubbles? A Tale of Two Markets – Paper

- Monetary Policy and the Housing Market – Paper

- Teardowns, Popups and Bump-outs: What Do Building Permits Say About Housing Supply? – Paper

- House Price Beliefs and Leverage Choice – Paper

- Do Gasoline Prices Affect Residential Property Values? – Paper

- Bank Risk-taking and the Real Economy: Evidence From the Housing Boom and its Aftermath – AEA

- Do Financial Constraints Cool a Housing Boom? Theory and Evidence From a Macroprudential Policy on Million Dollar Homes – Paper

- Housing Appreciation and Marginal Land Supply in Monocentric Cities with Topography – Paper

- Prospect Theory, Reverse Disposition Effect and the Housing Market – Paper

- How Do Households Discount Over Centuries? Evidence From Singapore’s Private Housing Market – Paper

- Property Right Restriction and House Prices – Paper and Presentation

- Cyclical Housing Prices in Flatland – Paper and Presentation

- House Prices, Mortgage Debt and Labor Mobility – AEA

- Model-Free Estimation of the Hedonic Price for Housing Space – Paper

On household finance:

- Household Finance and Consumer Behavior – Paper

- The Housing Crisis and the Rise in Student Loans – Paper

- Home Equity and the Timing of Claiming Social Security Retirement Income – AEA

- The Effect of Debt on Default and Consumption: Evidence From Housing Policy in the Great Recession – Paper

- Housing Wealth Effects: The Long View – Paper

On mortgages:

- Time to Homeownership and Mortgage Design: Income Sharing and Saving Incentive – Paper

- The Effect of Changing Mortgage Payments on Default and Prepayment: Evidence From HAMP Resets – Paper and Presentation

- The Effect of Interest Rates on Home Buying: Evidence From a Discontinuity in Mortgage Insurance Premiums – Paper and Presentation

- Liquidity Provision, Credit Risk and the Bond Spread: New Evidence From the Subprime Mortgage Market – Paper

- Collateral Damage: The Impact of Shale Gas on Mortgage Lending – Paper

- Are Mortgage Regulations Affecting Entrepreneurship? – Paper

- Eyes Wide Shut? Mortgage Insurance During the Housing Boom – AEA

- Effects of FHA Loan Limit Increases by ESA 2008: Housing Demand and Adverse Selection – AEA

- The Macroeconomic Effect of Government Asset Purchases: Evidence From Post-war United States Housing Credit Policy – Paper and Presentation

- How Much Are Car Purchases Driven by Home Equity Withdrawal? – Paper

- How Home Equity Extraction and Reverse Mortgages Affect the Credit Outcomes of Senior Households – AEA

- An Empirical Study of Termination Behavior of Reverse Mortgages – Paper

- Mortgage Default with Positive Equity – Paper

- Lending Competition and Non-Traditional Mortgages – Paper

On behavioral real estate:

- How Do the CEO Political Leanings Affect REIT Business Decisions? – Paper

- Outshine to Outbid: Weather-induced Sentiments on Housing Market – Paper and Presentation

- Contact High: The External Effects of Retail Marijuana Establishments on House Prices – AEA

- Relational Contracts, Reputational Concerns, and Appraiser Behavior: Evidence from the Housing Market – Paper

On affordable housing:

- Neighbors and Networks: The Role of Social Interactions on the Residential Choices of Housing Choice Voucher Holders – Paper

- Neighborhood Choices, Neighborhood Effects and Housing Vouchers – AEA

- Waiting for Affordable Housing – Paper

- Long-Run Outcomes of HOPE VI Public Housing Demolitions for Children – AEA

- The Effects of Residential Evictions on Low-Income Adults – Paper

On property taxes:

- Greener on the Other Side? Spatial Discontinuities in Property Tax Rates and their Effects on Tax Morale – AEA

- The Hated Property Tax: Salience, Tax Rates, and Tax Revolts – AEA

- Measuring Both Direct and Spillover Effects of Taxation: Evidence From a Property Tax Break for First-Time Buyers – Paper

- Impact of Housing Tax Preferences on Home Values and Neighborhood Sorting – AEA

- Do Local Governments Tax Homeowner Communities Differently? – Paper

On agency and bargaining:

- Why Disclose Less Information? Toward Resolving a Disclosure Puzzle in the Housing Market – Paper

- Examining Both Sides of the Transaction: Bargaining in the Housing Market – Paper

- Investor Bargaining Power, Rental Externalities and Housing Prices – Paper

- When are Real Estate Flippers Smarter Than the Crowd? – Paper

On homeownership:

- African-American Mayors, Home Ownership and Mortgage Lending in US Cities – Paper

- Do Homeowners Save More Than Renters? Evidence From the Panel on Household Finances – Paper and Presentation

- Home Sweet Home: (Mis-)Beliefs About the Extent to Which Home Ownership Makes People Happy – Paper

- Job Separation Risk and Home Ownership: Evidence From Assistant Professors – AEA

- Identifying the Benefits from Home Ownership: A Swedish Experiment – Paper

- Owned Now Rented Later? Housing Stock Transitions and Market Dynamics – Paper

- Diverted Homeowners and Rental Affordability – AEA

- School Quality, Latent Demand, and Bidding Wars for Houses – AEA

- Wage Trickle Down vs. Rent Trickle Down: How Does Increase in College Graduates Affect Wages and Rents? – AEA

Photo by Aliis Sinisalu

On international house pricing:

- Measuring House Prices in the Long Run: Insights from Dublin, 1900-2015 – AEA

- A Tale of Two Countries: Comparing Booms, Busts and Bubbles in the United States and Chinese Housing Markets – Paper

- Analyzing the Changes in the Distribution of House Prices in Beijing – AEA

- Locally Weighted Quantile House Price Indices and Distribution in Japanese Cities,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 4, 2018

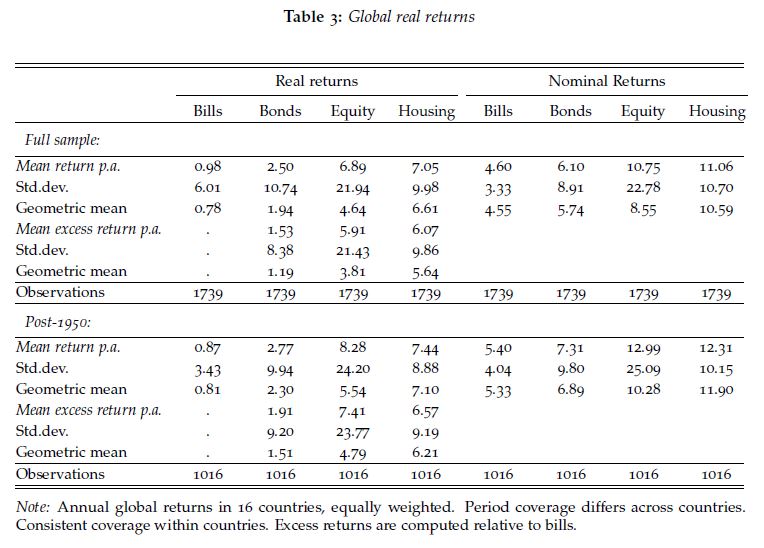

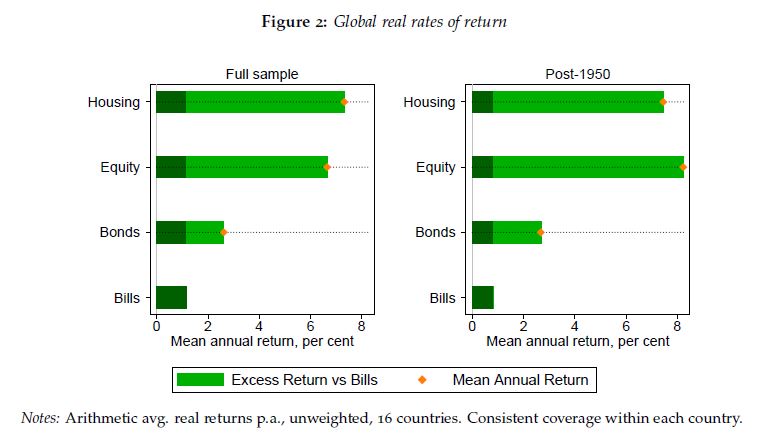

The Rate of Return on Everything: 1870–2015

From a new paper by Oscar Jorda, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor:

“This paper answers fundamental questions that have preoccupied modern economic thought since the 18th century. What is the aggregate real rate of return in the economy? Is it higher than the growth rate of the economy and, if so, by how much? Is there a tendency for returns to fall in the long-run? Which particular assets have the highest long-run returns? We answer these questions on the basis of a new and comprehensive dataset for all major asset classes, including—for the first time—total returns to the largest, but often ignored, component of household wealth, housing. The annual data on total returns for equity, housing, bonds, and bills cover 16 advanced economies from 1870 to 2015, and our new evidence reveals many new insights and puzzles.”

“This paper, perhaps for the first time, investigates the long history of asset returns for all the major categories of an economy’s investable wealth portfolio. Our investigation has confirmed many of the broad patterns that have occupied much research in economics and finance. The returns to risky assets, and risk premiums, have been high and stable over the past 150 years, and substantial diversification opportunities exist between risky asset classes, and across countries. Arguably the most surprising result of our study is that long run returns on housing and equity look remarkably similar. Yet while returns are comparable, residential real estate is less volatile on a national level, opening up new and interesting risk premium puzzles.”

From a new paper by Oscar Jorda, Katharina Knoll, Dmitry Kuvshinov, Moritz Schularick, and Alan M. Taylor:

“This paper answers fundamental questions that have preoccupied modern economic thought since the 18th century. What is the aggregate real rate of return in the economy? Is it higher than the growth rate of the economy and, if so, by how much? Is there a tendency for returns to fall in the long-run? Which particular assets have the highest long-run returns?

Posted by at 7:34 AM

Labels: Global Housing Watch

Friday, December 29, 2017

Housing View – December 29, 2017

On cross-country:

- Demographic Patterns of Reurbanisation and Housing in Metropolitan Regions in the US and Germany – Comparative Population Studies

On the US:

- A Shared Future: Data Democratization and Spatial Heterogeneity in the Housing Market – The Joint Center for Housing Studies

- LTV vs. LTI Constraints: When Did They Bind, and How Do They Interact? – University of Copenhagen

- Asymmetric effects of monetary policy in regional housing markets – Norges Bank

- Fannie and Freddie Continue in Limbo while Congress Looks for a Permanent Fix for the Housing Finance Market – Cato Institute

- Housing Disease and Public School Finances – NBER

- Investors Pile Into Suburban Rental Housing – Wall Street Journal

On other countries:

- [Singapore] Singapore authorities’ housing market warning may fall on deaf ears – Reuters

Photo by Aliis Sinisalu

On cross-country:

- Demographic Patterns of Reurbanisation and Housing in Metropolitan Regions in the US and Germany – Comparative Population Studies

On the US:

- A Shared Future: Data Democratization and Spatial Heterogeneity in the Housing Market – The Joint Center for Housing Studies

- LTV vs. LTI Constraints: When Did They Bind, and How Do They Interact? – University of Copenhagen

- Asymmetric effects of monetary policy in regional housing markets – Norges Bank

- Fannie and Freddie Continue in Limbo while Congress Looks for a Permanent Fix for the Housing Finance Market – Cato Institute

- Housing Disease and Public School Finances – NBER

- Investors Pile Into Suburban Rental Housing – Wall Street Journal

On other countries:

- [Singapore] Singapore authorities’

Posted by at 12:08 PM

Labels: Global Housing Watch

Monday, December 25, 2017

Housing in Bolivia

The IMF’s latest report on Bolivia says that:

“The FSL [Financial Services Law] has resulted in rapid credit growth directed to specific sectors and social housing (…) Housing lending should be closely monitored and the authorities should finalize and publish a housing price index. (…) More market-oriented mechanisms to improve financial access should be considered and the housing loan portfolio monitored closely.”

The IMF’s latest report on Bolivia says that:

“The FSL [Financial Services Law] has resulted in rapid credit growth directed to specific sectors and social housing (…) Housing lending should be closely monitored and the authorities should finalize and publish a housing price index. (…) More market-oriented mechanisms to improve financial access should be considered and the housing loan portfolio monitored closely.”

Posted by at 3:17 PM

Labels: Global Housing Watch

Subscribe to: Posts