Showing posts with label Global Housing Watch. Show all posts

Friday, February 23, 2018

Housing View – February 23, 2018

On the US:

- Jon Gray: Blackstone’s real estate chief turns heir apparent – Financial Times

- The Role of Technology in Mortgage Lending – Federal Reserve Bank of New York

On other countries:

- [Australia] Housing Market Imbalances in Australia: Development, Prospects, and Policies – IMF

- [Australia] Household Indebtedness and Mortgage Stress – Reserve Bank of Australia

- [Canada] Canada province readies housing plan amid affordability crisis – Reuters

- [Canada] British Columbia takes aim at housing speculation – Reuters

- [Canada] Vancouver’s Hot Housing Market Gets Tougher for Wealthy Chinese – Bloomberg

- [China] Housing Price, Consumption, and Financial Market: Evidence from Urban Household Data in China – ASCE

- [Malaysia] Unsold residential units in Malaysia at highest level for a decade – Global Property Guide

- [Spain] Mortgage Finance and Culture – IZA Institute of Labor Economics

- [Switzerland] Geneva’s ‘safe-haven’ houses look vulnerable – Financial Times

- Out of Sync Subnational Housing Markets and Macroprudential Policies – CESifo Group Munich

- [United Kingdom] UK’s Housing Market – IMF

- [United Kingdom] House prices and rents in the UK – mainly macro

- [United Kingdom] London, Residential Market Outlook, Spring 2018 – Cluttons

- [United Kingdom] A Fix to the U.K. Housing Crunch: Have More Money – Citylab

Photo by Aliis Sinisalu

On the US:

- Jon Gray: Blackstone’s real estate chief turns heir apparent – Financial Times

- The Role of Technology in Mortgage Lending – Federal Reserve Bank of New York

On other countries:

- [Australia] Housing Market Imbalances in Australia: Development, Prospects, and Policies – IMF

- [Australia] Household Indebtedness and Mortgage Stress – Reserve Bank of Australia

- [Canada] Canada province readies housing plan amid affordability crisis – Reuters

- [Canada] British Columbia takes aim at housing speculation – Reuters

- [Canada] Vancouver’s Hot Housing Market Gets Tougher for Wealthy Chinese – Bloomberg

- [China] Housing Price,

Posted by at 6:53 AM

Labels: Global Housing Watch

Wednesday, February 21, 2018

Mortgage Finance and Culture

From a new paper by Núria Rodríguez-Planas (IZA Institute of Labor Economics):

“Using a nationally representative sample of 12,344 immigrants from 41 different countries of ancestry living in Spain in 2007, we find that the higher the housing-loan penetration in the country of ancestry, the higher the likelihood of having a mortgage in Spain. Similarly, the higher the mortgage depth in the country of ancestry, the higher the present value of the monthly mortgage payments. Our results suggest that social norms regarding mortgage finance in the country of ancestry matter in determining immigrants’ mortgage finance in the host country. More specifically, the effect of social norms on the decision to have a mortgage (the extensive margin) and the amount of the mortgage payments (the intensive margin) is about one third and tenth the size of the effect of having a college degree on mortgage debt, respectively. Evidence of strong persistence of culture among those with longer tenure in the host country, those who immigrated as children or young adults, and second-generation immigrants suggests that vertical transmission of beliefs (from parents to children) is a plausible channel of transmission. Perhaps most importantly, we find that cultural attitudes regarding property rights are most relevant when explaining individuals’ decision to get a mortgage, but those regarding credit information matter most when explaining the amount of the mortgage debt.”

From a new paper by Núria Rodríguez-Planas (IZA Institute of Labor Economics):

“Using a nationally representative sample of 12,344 immigrants from 41 different countries of ancestry living in Spain in 2007, we find that the higher the housing-loan penetration in the country of ancestry, the higher the likelihood of having a mortgage in Spain. Similarly, the higher the mortgage depth in the country of ancestry, the higher the present value of the monthly mortgage payments.

Posted by at 1:40 PM

Labels: Global Housing Watch

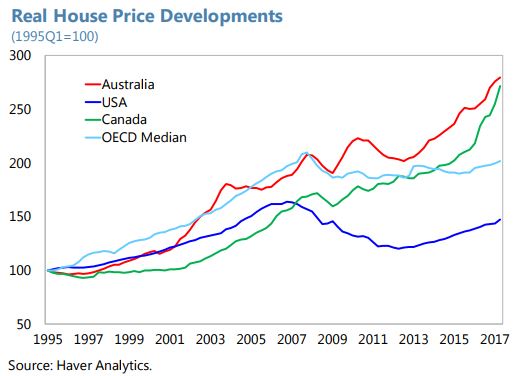

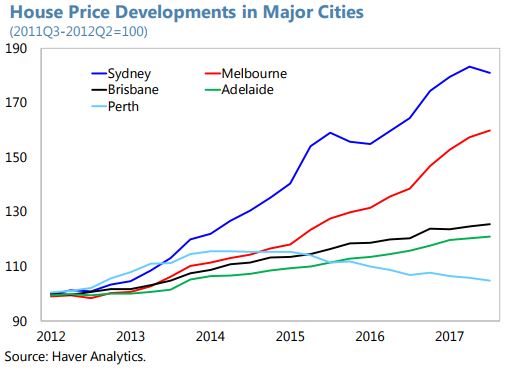

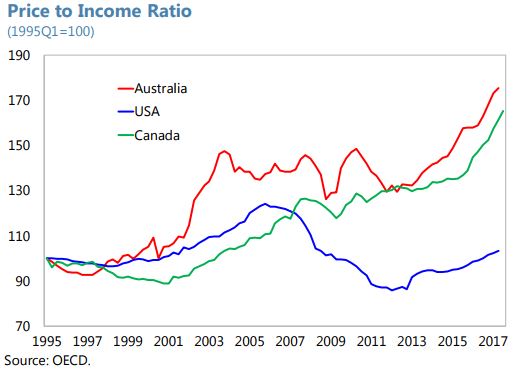

Housing Market Imbalances in Australia: Development, Prospects, and Policies

From the IMF’s latest report on Australia:

“After a housing boom over the past 6 years, Australia’s housing market imbalances and the macro-financial impact of their possible resolution have become a concern. House prices in the country’s eight capital cities have increased by 50 percent since early 2012, raising the value of Australian residential property from around 4 to over 5 times gross household disposable income and household debt to around twice the level of that income.

The housing boom has primarily been a regional boom, driven by demand shifts, and amplified by legacy imbalances and a slow supply response. Developments in Sydney and Melbourne have driven national house prices, reflecting shifts in the strength of regional economic activity and population growth since the end of the mining investment boom.

While housing markets may stabilize soon, housing affordability issues will likely remain a concern given prospects for further population growth in the eastern capitals. With such growth, the capitals need to prepare for affordable housing supply in the future, as both short-and long-term price elasticities of supply are low. In the long-term, urbanization, labor mobility, and productivity can be closely linked.

Housing-related policies have begun to address related imbalances and could usefully be complemented by tax reform. Reducing the imbalances requires a multi-pronged approach amid strong demand fundamentals. The combination of more infrastructure investment and recent zoning and planning regulatory reform should contribute to increase the supply of developable land and enable its more efficient use. Prudential policies have increased the resilience of household balance sheets and the banking sector to housing and other shocks. But household debt remains high, and continued prudential policies are important to manage the risks to domestic financial stability. Housing tax reform would support the effectiveness of the overall policy response.”

From the IMF’s latest report on Australia:

“After a housing boom over the past 6 years, Australia’s housing market imbalances and the macro-financial impact of their possible resolution have become a concern. House prices in the country’s eight capital cities have increased by 50 percent since early 2012, raising the value of Australian residential property from around 4 to over 5 times gross household disposable income and household debt to around twice the level of that income.

Posted by at 1:32 PM

Labels: Global Housing Watch

Friday, February 16, 2018

Housing View – February 16, 2018

On cross-country:

- Recent house price increases and housing affordability – European Central Bank

- European Mortgage Markets at Risk from Policy Tightening – Continuum 360

- Sovereign wealth funds quadruple investment in student housing – Financial Times

- Which foreign countries will grant me citizenship if I invest? – Financial Times

On the US:

- Housing Sentiment at New Survey High on Higher Home Price Expectations – Fannie Mae

- To increase employment among housing-assisted families, don’t pull the rug out from under them – Urban Institute

- Cut HUD, Fix Housing – Cato Institute

- Construction Wages: Who Makes the Most and Where? – BuildZoom

- A closer look at the fifteen-year drop in black homeownership – Urban Institute

- Mortgage Supply and Housing Rents – The Review of Financial Studies

On other countries:

- [Canada] British Columbia to curb housing speculation, crack down on tax cheats – Reuters

- [Canada] B.C. throne speech—government vows action on high house prices, but ignores their cause – Fraser Institute

- [Canada] Speculation is best hope for housing supply, developers say – Business Vancouver

- [China] China is trying new ways of skimming housing-market froth – Economist

- [Malaysia] Unsold homes in Malaysia rise to decade high in 2017 – Reuters

- [Sweden] Reduced housing construction is subduing GDP growth – Riksbank

- [Sweden] Household Finances Exposed to Falling House Prices – Continuum Economics

Photo by Aliis Sinisalu

On cross-country:

- Recent house price increases and housing affordability – European Central Bank

- European Mortgage Markets at Risk from Policy Tightening – Continuum 360

- Sovereign wealth funds quadruple investment in student housing – Financial Times

- Which foreign countries will grant me citizenship if I invest? – Financial Times

On the US:

- Housing Sentiment at New Survey High on Higher Home Price Expectations – Fannie Mae

- To increase employment among housing-assisted families,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, February 14, 2018

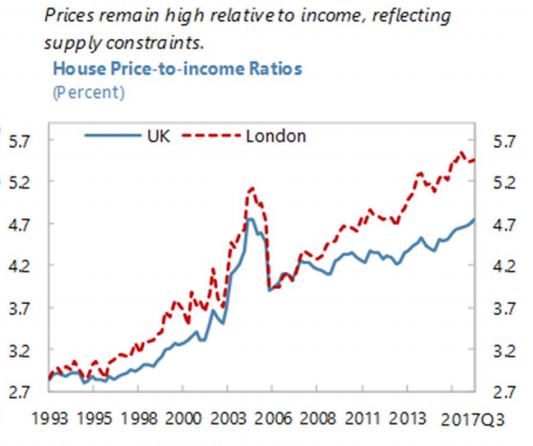

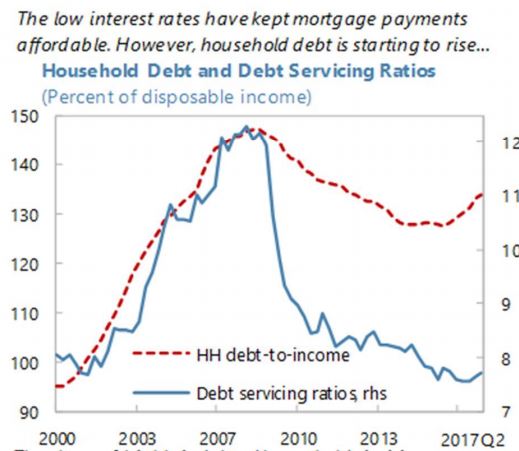

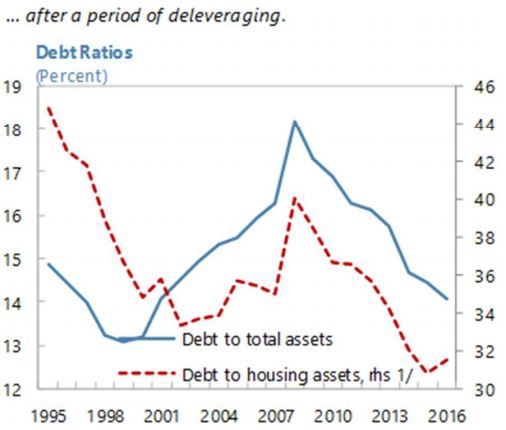

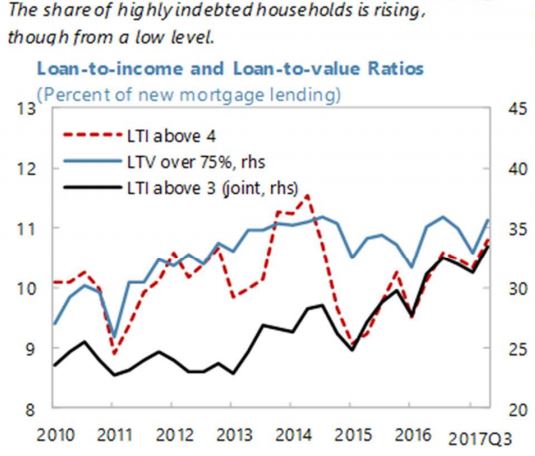

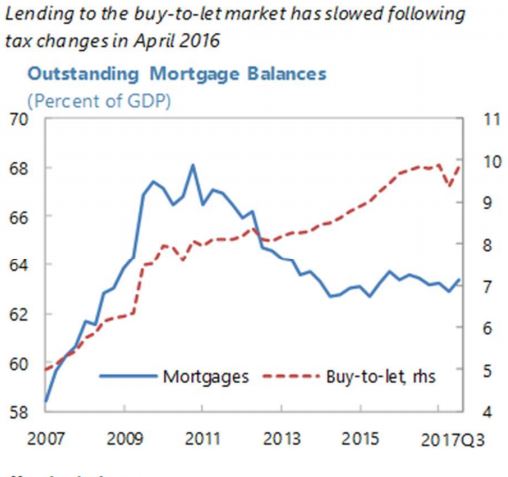

UK’s Housing Market

From the IMF’s latest report on the UK:

“Housing supply. Efforts should continue to boost housing supply, including by easing planning restrictions and reforming property taxes to encourage more efficient use of the housing stock. Increasing supply would support near-term growth, facilitate labor mobility across regions, support financial stability by making homes more affordable, and promote social cohesion by reducing wealth inequality.”

From the IMF’s latest report on the UK:

“Housing supply. Efforts should continue to boost housing supply, including by easing planning restrictions and reforming property taxes to encourage more efficient use of the housing stock. Increasing supply would support near-term growth, facilitate labor mobility across regions, support financial stability by making homes more affordable, and promote social cohesion by reducing wealth inequality.”

Posted by at 10:17 AM

Labels: Global Housing Watch

Subscribe to: Posts