Showing posts with label Global Housing Watch. Show all posts

Tuesday, April 24, 2018

Housing in Africa: A Crisis or An Opportunity?

Global Housing Watch Newsletter: April 2018

In this interview, Issa Faye, El-Hadj M. Bah, and Zekebweliwai F. Geh discuss their new book—Housing Market Dynamics in Africa. Faye is currently a Director at the International Finance Corporation and formerly a Manager at the African Development Bank. Bah is Principal Research Economist also at the African Development Bank. And Geh is a Policy Advisor also at the African Development Bank.

On the main message…

Hites Ahir: The opening line of this new book says: “(…) this book comes at a very critical time for Africa.” Can you elaborate on this?

Authors: The aftershocks of the global economic downturn continue to stymie growth. Low commodity prices and a sluggish global economic growth has slowed down the growth momentum in several African countries. At the same time, the continent’s rising urbanization is putting immense pressure on the already stretched urban infrastructure in various cities, while growing debt level is lowering the ability of governments to mobilize external sources of finance. Moreover, Africa’s growing youth unemployment is a rising threat that demands urgent action. Addressing these problems require an economic transformation that will create jobs, reduce poverty and inequality. Leveraging the abundant workforce for manufacturing and labor-intensive industries should therefore be encouraged.

Hites Ahir: In a nutshell, what is the main message of this book?

Authors: Five key messages emanate from our research. First, Africa is facing a looming housing crisis as the affordable housing supply dwarfs demand, particularly in the formal sector. This annual shortage is adding to the existing large deficits observed in many cities across the continent. This has led to the proliferation of slums. Second, while addressing the affordable housing shortage will be a huge challenge, it also presents an opportunity for structural transformation and inclusive growth in Africa. Third, creating an enabling environment for the supply of affordable rental housing should be part of any national housing strategy. Fourth, strong political leadership is crucial for transforming the sector. Governments need to effectively implement their role as regulators, input providers, and facilitators. Last but not the least, we argue that development financial institutions have a catalytic role to play by assisting governments in fulfilling their various roles, as well as provide long-term financing needed for the development of affordable housing finance markets.

Hites Ahir: How different is this book compared to the work that the Center for Affordable Housing Finance in Africa, the World Bank, and others have done on Africa?

Authors: This book offers the most comprehensive coverage of issues related to housing development in Africa. It is the result of not only desk research but also of extensive consultation with stakeholders on the ground. This has guided the proposed solutions.

On large housing deficits…

Hites Ahir: The book says: “The rapid urbanization rates and lack of urban planning have resulted in very large housing deficits, defined as the difference between the number of households, and the number of permanent dwellings.”. Can you tell us in numbers how big is the housing deficit in Africa?

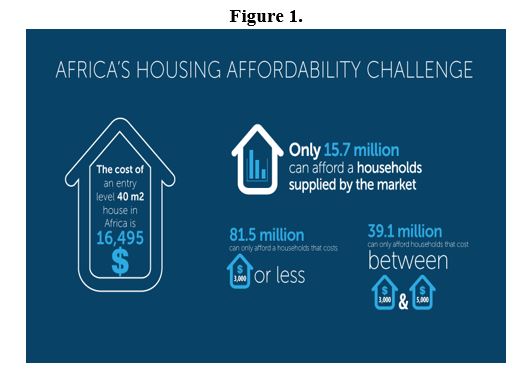

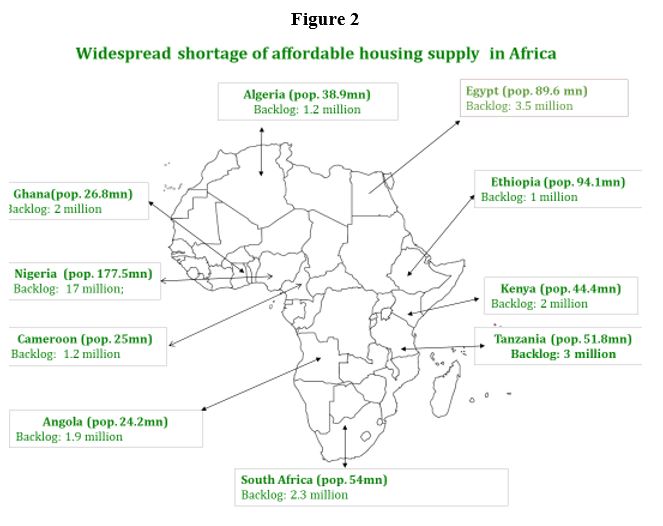

Authors: We conservatively estimate the deficit to be at least 50 million housing units (50.6 million to be precise). We should emphasize that this is a rough estimate given the absence of recent housing census data in all countries. Generally, the most populous countries have larger deficits.

Hites Ahir: What explains these large housing deficits across countries?

Authors: Several factors explain the large housing deficits observed in the continent. Rapid urbanization fueled by rural to urban migration and endogenous population growth is raising the demand for housing. However, the supply of housing has been insufficient for several reasons. First, poor urban planning is hampering urban expansion through limited supply of land and infrastructure. Second, multiple land tenure regimes, and inadequate land administration and governance systems contribute to land tenure insecurity and the high costs of urban land. Third, high construction costs make housing unaffordable to the majority of low and middle-income households. Furthermore, underdeveloped housing finance markets imply that most Africans can only rely on self-financing and incremental construction mechanisms to acquire housing.

Hites Ahir: What are the social and economic consequences of housing deficits?

Authors: Housing deficits in Africa mean that a large percentage of Africans live in slums, which is characterized by poor housing conditions and lack of basic infrastructure such as roads, electricity, piped water and sewage. A large literature has shown that those living conditions lead to poor health conditions (e.g. malaria, cholera, tuberculosis, respiratory diseases, stress and depression), lower educational attainment, insecurity and an overall poor contentment with life. These poor health outcomes lead to lower work productivity and increases the disease burden of countries. Moreover, lower educational opportunities for children in slums implies lower overall human capital in the future. Large housing deficits also imply higher housing costs, which means that overall savings and investment in productive activities will be lower.

Hites Ahir: What can be done?

Authors: A one-size fits all approach will not resolve Africa’s housing deficit. Possible solutions should take into account country specific challenges. However, comprehensive policies should simultaneously address constraints on the supply and the demand sides. The challenge on the supply side is how to increase the availability of affordable housing. Actions that will have great impact include updating urban plans, taking into account recent socioeconomic developments; reforming land administration and governance systems with the aim of improving tenure security, increasing the supply of well-located plots and lower overall land costs; and lowering construction costs. On the demand side, financing mechanisms, including guarantees, are needed to enable households to undertake the acquisition of housing overtime.

Hites Ahir: How much will it cost?

Authors: We estimate that eliminating the housing backlog of 50.6 million in 10 years will cost at least US$2.08 trillion. This estimate is based on the average construction cost for Africa and an assumption on the typology of housing needed and housing demand. While this number is large, such spending would add at least US$5.07 trillion to Africa’s GDP.

On the link between construction and inclusive growth…

Hites Ahir: Even with all the challenge that you have mentioned earlier, there is also an opportunity for Africa. The book says: “housing construction is a source of inclusive growth”. Can you elaborate on this?

Authors: Housing construction is labor-intensive with the construction of one housing unit creating between two and six full-time equivalent (FTE) jobs for at least a year. In addition, the sector employs a large number of young people with low skills. The strong forward and backward linkages also means that growth in the construction sector will stimulate growth in other sectors such as manufacturing.

Hites Ahir: The book points out that construction costs are high in Africa compared to other part of the world. What explains this?

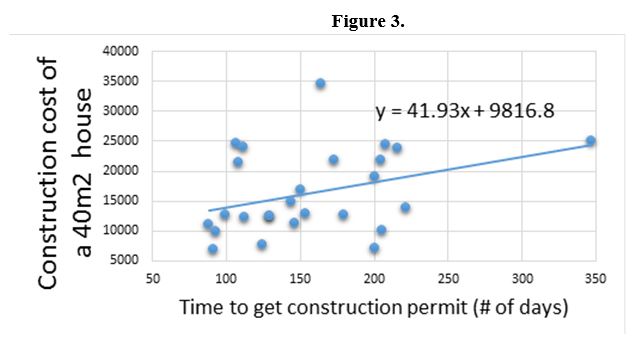

Authors: Failures at different steps of the construction value chain explain the high construction costs. The largest factor is the high costs of building materials, which represents more than 50 percent of the construction costs. Limited supply of construction materials, monopoly pricing and a large share of imports contribute to high building material prices. Government regulation and administrative burdens also plays an important role. For instance, we find that the time required to obtain construction permits is positively correlated with construction costs. Another factor is the lack of capacity of construction companies and lower technical skills of construction workers. In most countries, housing construction is dominated by small and medium enterprises with little or no capacity to deliver 500 housing units per year.

Hites Ahir: What have countries done to reduce constructions costs? Are there any quick and easy remedies that policymakers can implement?

Authors: The book discusses seven actions that can reduce construction costs. Here, we will mention just three. Labor-intensive industrialized construction has great potential to lower costs and accelerate housing delivery. This approach is being pursued in Ethiopia. Local production of building materials can also have dramatic effects on construction costs. For instance, in Zambia, cement prices decreased by 40% between 2014 and 2015 following the commissioning of a new production plant. Alternative building technologies, including the use of local building materials such as compressed stabilized earth blocks have shown that they can reduce construction costs. However, cultural biases and outdated building codes among other have prevented these technologies from taking off.

Concluding thoughts…

Hites Ahir: When working on this book, what would you say was the biggest surprising finding?

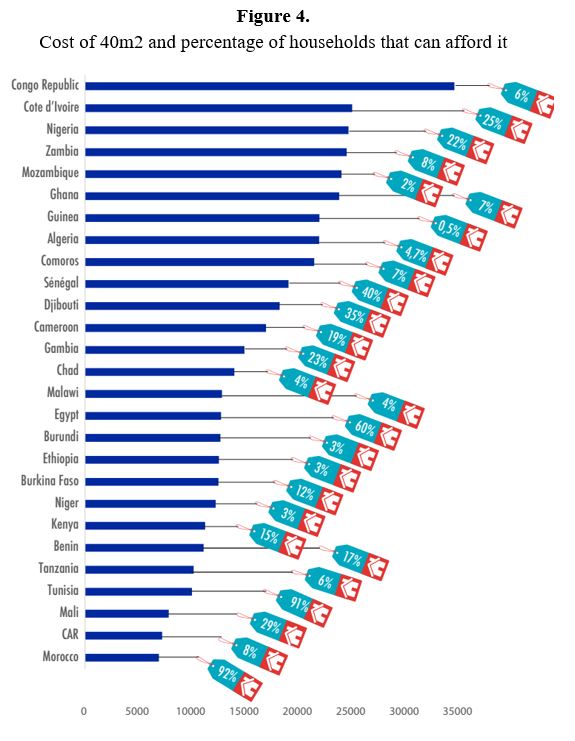

Authors: The cross-country variation of construction costs is perhaps the most surprising finding. It costs 5 times more to build a house in Congo than in Morocco.

Hites Ahir: With all the challenges that you have briefly described, which one you think will be the hardest to tackle? Why?

Authors: Government regulations and administrative burden is probably the hardest to tackle. Our analysis of the housing value chain shows that government failures are at the heart of many constraints on both the supply and demand sides. While a number of governments are undertaking regulatory reforms, effective implementation remains limited.

Hites Ahir: Is there a success story emerging from Africa—a country that is doing well in managing the housing market?

Authors: Ethiopia and Morocco are two countries that have shown great leadership and experienced great successes.

A final note: In our view, creating a conducive enabling environment, adopting and implementing a comprehensive housing strategy, as well as the existence of strong political will are prerequisites for addressing the continents housing crisis.

Global Housing Watch Newsletter: April 2018

In this interview, Issa Faye, El-Hadj M. Bah, and Zekebweliwai F. Geh discuss their new book—Housing Market Dynamics in Africa. Faye is currently a Director at the International Finance Corporation and formerly a Manager at the African Development Bank. Bah is Principal Research Economist also at the African Development Bank. And Geh is a Policy Advisor also at the African Development Bank.

Posted by at 5:00 AM

Labels: Global Housing Watch

Housing, Urban Development, and the Macroeconomy

Global Housing Watch Newsletter: April 2018

This post is written by Kilian Heilmann, and Andrea Nocera. Both are Postdoctoral Research Associate at the Dornsife Institute for New Economic Thinking (INET) at the University of Southern California.

The USC Dornsife Institute for New Economic Thinking (INET) organized a conference on “Housing, Urban Development, and the Macroeconomy” on April 6th and 7th at the University of Southern California. The conference brought together researchers from a wide range of fields to discuss recent developments in the research on housing. Organized into 7 sessions of similar thematic overlap, 7 invited speakers, and 17 contributing speakers presented their papers over two days. The presenters came from a diverse background, and represented academic institutions, and central banks from America, Europe, and Australia.

On the relationship between housing and credit…

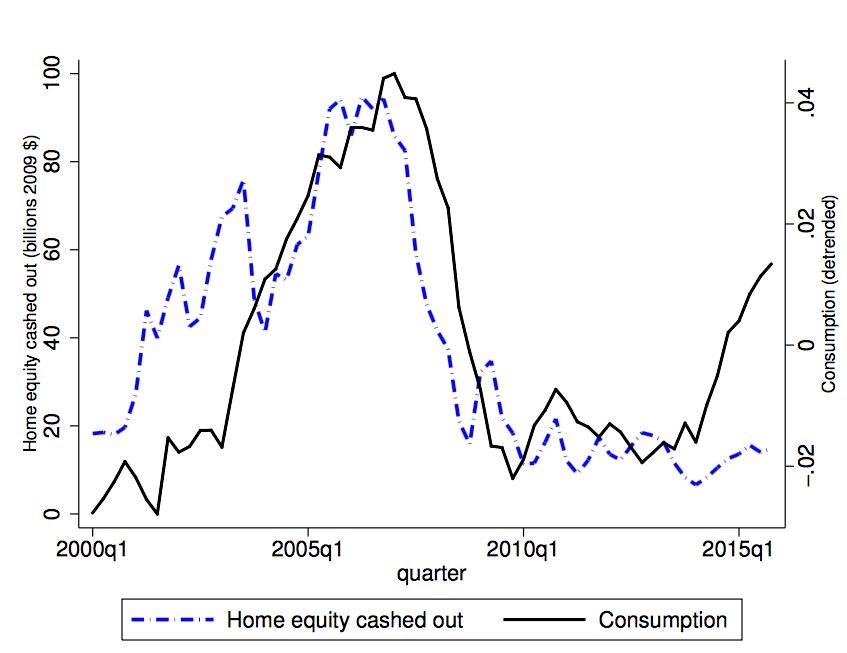

After the opening remarks by INET Director M. Hashem Pesaran, the first session focused on the relationship between housing and credit. Matteo Iacoviello (Federal Reserve Board) led the discussion presenting his joint work with Ricardo Nunes and Andrea Prestipino, titled “Optimal Credit Market Policy”. The authors advocated a simple countercyclical housing tax to avoid excessive under/overborrowing (presentation). Edward Kung (UCLA, “Interest Rates and Housing Market Dynamics in a Housing Search Model” with Elliot Anenberg) provided new evidence on the role of mortgage rates in the housing market. Xiaoqing Zhou (Bank of Canada, “Home Equity Extraction and the Boom-Bust Cycle in Consumption and Residential Investment”) questioned the common view that higher mortgage loans contributed to higher consumption arguing that their main use was to finance housing investments (presentation). Further contributions to this important topic were given by Isaac Gross (Oxford University, “Anticipated Changes in Household Debt and Consumption”) who suggested that households that anticipate a house purchase may have low or even negative marginal propensities to consume, and discussed possible implications of tax credits for first-time home buyers.

Note: Home equity and consumption. Taken from: Zhou (2018), Home Equity Extraction and the Boom-Bust Cycle in Consumption and Residential Investment

On crises and housing market dynamics…

Crises and housing market dynamics were at the center of the second session which started with Chandler Lutz (Copenhagen Business School). His paper “A Crisis of Missed Opportunities? Foreclosure Costs and Mortgage Modification During the Great Recession” (joint with Stuart Gabriel and Matteo Iacoviello) investigates the housing impacts of the 2000s crisis-period California Foreclosure Prevention Laws. Tom Schmitz (Bocconi University, “The Financial Transmission of Housing Bubbles: Evidence from Spain”, with Alberto Martin and Enrique Moral-Benito) documented both crowding-out, and crowding-in effects of the Spanish housing bubble on the credit market (presentation). The session concluded with Jacob Cosman (Johns Hopkins) whose paper “Concentration and market cycles in the production of new housing” (with Luis Quintero) sheds new light on the impact of increasing concentration in local residential construction markets on housing cycle dynamics (presentation).

On housing regulation and migration…

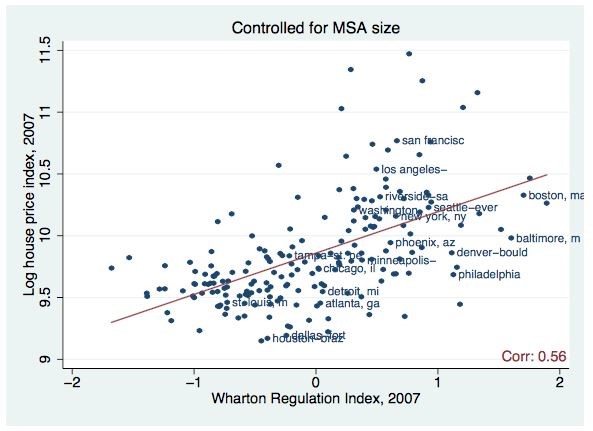

In the third session “Issues in Housing Regulation and Migration”, Morris Davis (Rutgers) presented new evidence on “Gross Migration and Urban Population Dynamics” (joint with Jonas Fisher and Marcelo Veracierto). Andrii Parkhomenko (USC) discussed “The Rise of Housing Supply Regulation in the US: Local Causes and Aggregate Implications”, and highlighted the connection between housing supply regulations, and aggregate productivity. Christoph Hedtrich presented a model that studies the relationship between living costs, and investment in automation (“Automation, Spatial Sorting, and Job Polarization”, with Jan Eeckhout and Roberto Pinheiro). In the last presentation, Wukuang Cun (USC) spoke on “Land Use Regulations, Migration and Rising House Prices Dispersion in the US” (joint with Hashem Pesaran).

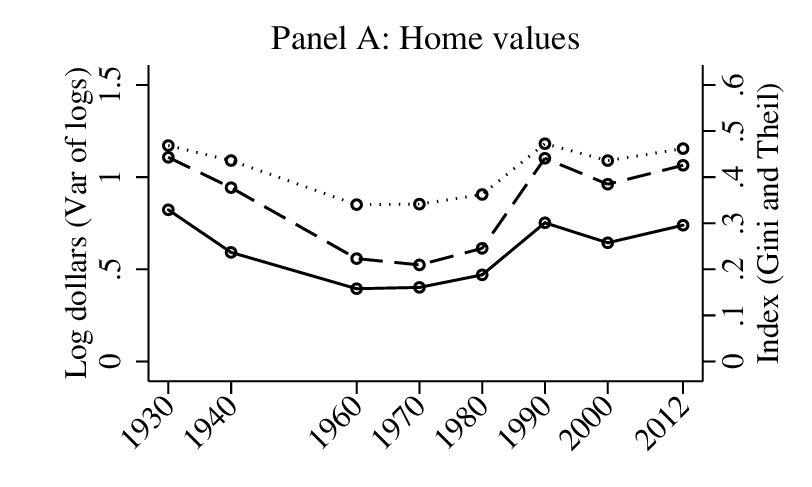

Note: Historic evolution of home value inequality. Taken from: Albouy et al (2018), Housing Inequality

Note: Regulation and House Prices. Taken from: Parkhomenko (2018), The Rise of Housing Supply Regulation in the U.S.: Local Causes and Aggregate Implications

On neighborhood dynamics…

The last session of the day concerned issues in neighborhood dynamics. David Albouy (UIUC) presented new facts on historical housing inequality and constructed measures based on data from censuses dating back to 1930 (presentation). The results show evidence for a post WWII “great compression” in housing consumption, and highlighted the importance of within-MSA inequality (“Housing Inequality” with Aditya Aladangady and Mike Zabek). Jeffrey Brinkman (Fed Philadelphia, “Freeway Revolts!” with Jeffrey Lin) highlighted the heterogeneous effects of transportation infrastructure in the context of freeway construction. Amine Ouazad (HEC Montreal, “Dynamic Location Choice, Housing Market Frictions, and Real Estate Dynamics” with Romaine Ranciere) contributed with a paper that studies the impact of credit market frictions on neighborhood location choice. Lastly, Lorenzo Neri’s (Queen Mary University) paper on “School Performance, Score Inflation and Economic Geography” (joint with Erich Battistin) measured the effect of a noisy measure of school quality on housing prices.

On regional heterogeneity and the macroeconomy…

The second day of the conference started with a session on regional heterogeneity and the macroeconomy. Joseph Vavra (Chicago Booth) presented his joint research with Martin Beraja, Andreas Fuster, and Erik Hurst on “Regional Heterogeneity and the Refinancing Channel of Monetary Policy” where they argue that the distribution of housing equity plays a crucial role in the economy’s response to interest rate declines. Knut Are Aastveit’s (Norges Bank and BI Norwegian Business School) paper “Asymmetric Effects of Monetary Policy in Regional Housing Markets” (with Andre Anundsen) suggests that regional house price responses to monetary policy vary over the business cycle, and depend on housing supply elasticities. Francois Gerolf (UCLA, “Property Tax Shocks and Macroeconomics” with Thomas Grjebine) collects data on tax on housing property for OECD countries to measure the impact of property tax shocks on the macroeconomy. Natalia Bailey (Monash University, “Quasi Maximum Likelihood Estimation of Spatial Model with Heterogeneous Coefficients” joint with Miquele Aquaro and Hashem Pesaran) contributed to methodological advances by introducing heterogeneous coefficients in spatial econometric models.

On housing finance risks…

In a session on housing finance risks, Rodney Ramcharan (USC Marshall) presented his paper “Bank Balance Sheets and Liquidation Values” where he investigates the role of bank balance sheets in shaping the liquidation value of real estate collateral. In joint work with Lu Han “Financing Risk and Information Bias in Housing Markets”, Seung-Hyun Hong (University of Illinois) compares sales prices between all-cash transactions, and mortgage transactions in Los Angeles, and identifies financing risk and information bias as new sources of housing market frictions. You Suk Kim’s (Board of Governors of the Federal Reserve System) paper “The Effect of Government Mortgage Guarantees on Home Ownership” (with Serafin Grundl) finds that government mortgage guarantees have a very small effect on home ownership.

On homeownership and demography…

The conference concluded with a session on homeownership and demography. Jorge de la Roca’s (USC) paper “City of Dreams” (with Gianmarco Ottaviano and Diego Puga) highlighted that imperfect assessment of one’s own ability can lead to the observed fact that there is little sorting on ability between cities. In the last presentation of the conference called “Homeownership and Housing Transitions: Explaining the Demographic Composition” (with Eunseong Ma), Sarah Zubairy (Texas A&M) presented new evidence on uneven composition of homeownership rates during its surge from 1995-2005.

In conclusion, the conference reflected the variety of research approaches to the important topic of housing, and its related fields. Both microeconomists and macroeconomists as well as econometricians contributed to the program. The methods presented at the conference ranged from macroeconomic models to microeconomic analysis of historic data to econometric analysis of spatial heterogeneity. This reflected the spirit of the USC Dornsife Institute for New Economic Thinking to consider novel, and diverse approaches to the analysis of significant research questions.

Global Housing Watch Newsletter: April 2018

This post is written by Kilian Heilmann, and Andrea Nocera. Both are Postdoctoral Research Associate at the Dornsife Institute for New Economic Thinking (INET) at the University of Southern California.

The USC Dornsife Institute for New Economic Thinking (INET) organized a conference on “

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, April 20, 2018

Housing View – April 20, 2018

On the US:

- Why America Needs More Social Housing – American Prospect

- Housing: A shortage of cities – City Observatory

- Is Housing a Good Investment? Where You Stand Depends on Where You Sit – Federal Reserve Bank of New York

- Home Remodeling Expected to Remain Strong and Steady into 2019 – Harvard Joint Center for Housing Studies

On other countries:

- [Canada] Not In My Neighbor’s Back Yard: External Effects of Density – University of British Columbia

- [Canada] The Propagation of Regional Shocks in Housing Markets: Evidence from Oil Price Shocks in Canada – Centre for Economic Policy Research

- [China] Effect of land prices on the spatial differentiation of housing prices: Evidence from cross-county analyses in China – Journal of Geographical Sciences

- [Korea] Housing Dynamics in Korea – OECD

- [United Arab Emirates] Abu Dhabi’s housing market cools down – Financial Times

- [United Kingdom] Building more homes requires more than planning tweaks – Financial Times

- [United Kingdom] London house prices mark first annual drop since 2009 – Financial Times

Photo by Aliis Sinisalu

On the US:

- Why America Needs More Social Housing – American Prospect

- Housing: A shortage of cities – City Observatory

- Is Housing a Good Investment? Where You Stand Depends on Where You Sit – Federal Reserve Bank of New York

- Home Remodeling Expected to Remain Strong and Steady into 2019 – Harvard Joint Center for Housing Studies

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, April 17, 2018

Stabilizing China’s Housing Market

From a new IMF Working Paper by Richard Koss and Xinrui Shi:

“The sharp rise of house prices in China’s Tier-1 cities has fostered a great deal of commentary about the possibility of bubbles forming there. However, China’s unique housing market characteristics make it difficult to assess the macroeconomic severity of bursting bubbles, even if they exist. These include the setting of land supply and prices by the government, among many others. The presence of overbuilt “ghost cities” greatly complicates the ability of traditional macroeconomic policies to address these concerns. This paper looks at proposals to shore up the mortgage underwriting and legal infrastructure to help China withstand the impact of falling prices, should this occur.”

From a new IMF Working Paper by Richard Koss and Xinrui Shi:

“The sharp rise of house prices in China’s Tier-1 cities has fostered a great deal of commentary about the possibility of bubbles forming there. However, China’s unique housing market characteristics make it difficult to assess the macroeconomic severity of bursting bubbles, even if they exist. These include the setting of land supply and prices by the government, among many others.

Posted by at 5:07 PM

Labels: Global Housing Watch

Friday, April 13, 2018

Housing View – April 13, 2018

On cross-country:

- For Home Prices in London, Check the Tokyo Listings – IMF

- Global Investors, House Price Dispersion, and Synchronicity – IMF

- Housing as a Financial Asset – IMF

- The Global Housing Crisis – The Atlantic

- Global Residential Cities Index – Q4 2017 – Knight Frank

On the US:

- Housing Recoveries without Homeowners: A Global Perspective – Federal Reserve Bank of St. Louis

- The Housing Supply Puzzle: Part 1, Divergent Markets – Federal Reserve Bank of St. Louis

- The Housing Supply Puzzle: Part 2, Rental Demand – Federal Reserve Bank of St. Louis

- The Unfulfilled Promise of the Fair Housing Act – The New Yorker

- The Fair Housing Act at 50: Not Sufficiently Powerful to Reverse Residential Racial Segregation – Social Education

- The Fair Housing Act at 50 – Harvard Joint Center for Housing Studies

- VIDEO: Housing Segregation In Everything – NPR

- American Houses Keep Getting Bigger — And so Does American Debt – Mises Institute

- What is holding back housing? – Business Economics

- What Would it Take for Housing Subsidies to Overcome Affordability Barriers to Inclusion in All Neighborhoods? – Harvard Joint Center for Housing Studies

- How Will the New Tax Law Affect Homeowners in High Tax States? It Depends – Federal Reserve Bank of New York

- Have Incomes Kept Up with Rising Rents? – Harvard Joint Center for Housing Studies

- A change to California’s housing supply law could spur a big expansion in home building – Los Angeles Times

- A Small Fix for the Housing Crunch Is in Your Backyard – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- For Home Prices in London, Check the Tokyo Listings – IMF

- Global Investors, House Price Dispersion, and Synchronicity – IMF

- Housing as a Financial Asset – IMF

- The Global Housing Crisis – The Atlantic

- Global Residential Cities Index – Q4 2017 – Knight Frank

On the US:

- Housing Recoveries without Homeowners: A Global Perspective – Federal Reserve Bank of St.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts