Showing posts with label Global Housing Watch. Show all posts

Friday, March 29, 2019

Housing Market in Sweden

From the IMF’s latest report on Sweden:

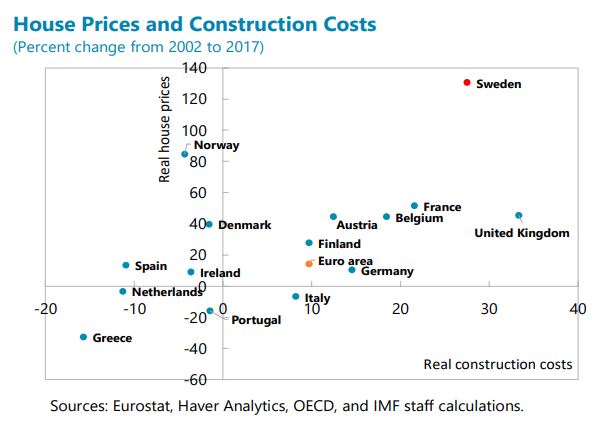

“High housing prices and high market rents increase vulnerabilities and inequality. Despite their recent moderation, house prices have tripled in real terms since the mid-1990s, lifting

the price-to-income (PTI) ratio to almost 30 percent above its 20-year average, with Stockholm’s PTI nearly twice the national average and among the highest worldwide. New purchasers must take on high debts relative to income (DTI), typically at floating rates, a macrofinancial vulnerability (…). Moreover, long queues for rent-controlled apartments meant that those unable to purchase housing had to pay much higher rents on subletted or newly constructed apartments, that are estimated to be 65 percent higher on average. An “insider-outsider” problem arises as labor mobility to the main centers is most impaired for those without parents able to assist with large down payments, impeding growth and exacerbating intergenerational and regional inequality.The “January agreement” includes promising steps but comprehensive housing reforms are needed given the scale of the problem. Key elements of a reform package include:

- Making the rental market work: in addition to fully liberalizing rents of newly constructed apartments, there is a need to phase out existing controls. A common approach is to apply market rents when there is a change in tenant. Access to the housing allowance could be expanded to cushion this adjustment (see below), while also applying a temporary “windfall” tax on significant rental income gains. To help reduce market rents more quickly, rental supply should be increased, such as by reducing impediments to sub-letting and to households renting out their own apartments, while containing macrofinancial risks from buy-to-let housing.

- Taxing property to rebalance the housing market: Sweden’s property tax was capped in 2008 to be among the lowest in the OECD, limiting the cost to households of occupying housing beyond their needs. A broad-based increase in the ceiling on the property tax would be most efficient, but an increase targeted to the main centers could be considered to incentivize mobility where it is most needed. Abolishing the interest on deferrals of capital gains taxes will help ease deterrents to mobility. An additional step to be considered is to tax only a portion of the capital gains on primary dwellings. Implementing a phase out of mortgage interest deductibility—which boosts housing demand and prices—would have limited impact on household finances currently given the low level of interest rates.

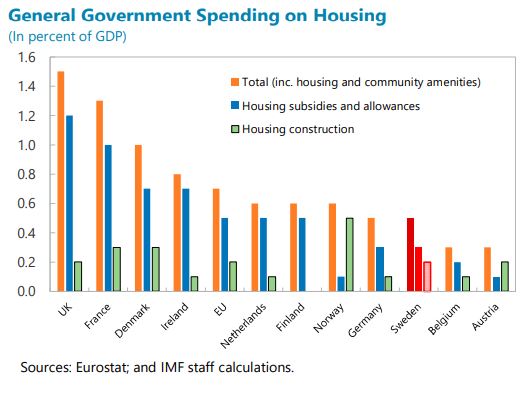

- Producing housing that is affordable: it is important to simplify the planning process to reduce the cost of construction which have risen by over 28 percent in real terms over the past 15 years, compared with 10 percent in the euro area. Productivity in the construction sector should be enhanced by strengthening competition, including by harmonizing land sale procedures across the municipalities and preventing requirements beyond national building standards in the approval process. The government should also expand existing subsidies for construction of affordable rental apartments, together with those for student and elderly housing in view of changing demographics.

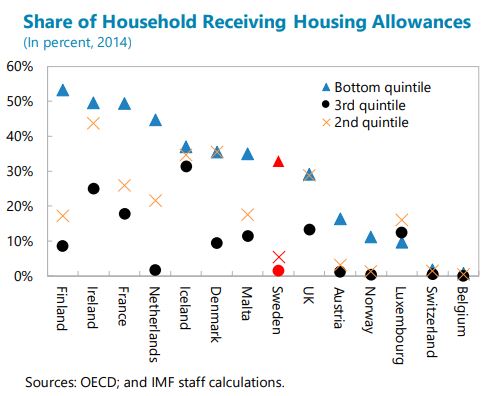

Protecting households in the transition is important to help build broad consensus on comprehensive reforms. On average, the share of rental expenditure in disposable income would increase from 24 percent to 31 percent, with most impact on households in the lowest income decile, which could be cushioned by expanding payments under the existing housing allowance. However, this allowance is seldom paid to households in the second or third income quintiles, contributing to relatively low total expenditure on housing allowances in Sweden. There is a need to review the coverage and amounts of housing allowances to give confidence that a transition to market rents will be manageable.

The authorities recognize the long-standing structural weaknesses in the Swedish housing market. They emphasized that housing policies were politically contentious in Sweden, limiting the feasibility of some reforms that could be most effective in principle, such as raising property taxation. Nevertheless, implementing the measures included in the “January agreement” during the term of the government would represent a step forward.”

From the IMF’s latest report on Sweden:

“High housing prices and high market rents increase vulnerabilities and inequality. Despite their recent moderation, house prices have tripled in real terms since the mid-1990s, lifting

the price-to-income (PTI) ratio to almost 30 percent above its 20-year average, with Stockholm’s PTI nearly twice the national average and among the highest worldwide. New purchasers must take on high debts relative to income (DTI), typically at floating rates,

Posted by at 10:25 AM

Labels: Global Housing Watch

Housing View – March 29, 2019

On cross-country:

- Scared of Stocks? Buy a House Instead – Bloomberg

- Can Upzoning Increase Housing Supply and Affordability? – Planetizen

- Changing the Housing Story – the Shaping Futures report – SF21

On the US:

- Why Housing Policy Is Climate Policy – New York Times

- Three Scenarios for Growth in Homeowner and Renter Households – Harvard Joint Center for Housing Studies

- How Poor Americans Get Exploited by Their Landlords – Citylab

- A Growing Problem in Real Estate: Too Many Too Big Houses – Wall Street Journal

- Rural America Faces a Housing Cost Crunch – Pew Charitable Trusts

- Zoned Out? The Determinants of Manufactured Housing Rents: Evidence from North Carolina – Journal of Housing Economics

- U.S. housing, consumer confidence data point to slowing economy – Reuters

- A Decade After the Housing Bust, the Exurbs Are Back – Wall Street Journal

On other countries:

- [Australia] Australia central bank research shows income, not just property weakness, key for policy – Reuters

- [Australia] Australia’s Property Stocks Are Ignoring the Housing Slump – Bloomberg

- [Canada] Trudeau housing plan ignores local drivers of affordability – Fraser Institute

- [Canada] The Big Short’s Steve Eisman raises bets against Canadian banks – Financial Times

- [Canada] Housing Is a Magnet for Money Launderers in Toronto: Study – Bloomberg

- [China] That Property Boom Could Be the Reason Employees Are Goofing Off – Bloomberg

- [Denmark] World’s Cheapest Mortgage May Be Around the Corner in Denmark – Bloomberg

- [Finland] Finland’s housing market remains weak – Global Property Guide

- [Italy] Italy House Price Drop Adds Woe for Economy in Recession – Bloomberg

- [Netherlands] Brexit Is Making It Even Harder to Find a Flat in Amsterdam – Bloomberg

- [United Arab Emirates] How Dubai can solve its lack of affordable housing – World Economic Forum

On cross-country:

- Scared of Stocks? Buy a House Instead – Bloomberg

- Can Upzoning Increase Housing Supply and Affordability? – Planetizen

- Changing the Housing Story – the Shaping Futures report – SF21

On the US:

- Why Housing Policy Is Climate Policy – New York Times

- Three Scenarios for Growth in Homeowner and Renter Households – Harvard Joint Center for Housing Studies

- How Poor Americans Get Exploited by Their Landlords – Citylab

- A Growing Problem in Real Estate: Too Many Too Big Houses – Wall Street Journal

- Rural America Faces a Housing Cost Crunch – Pew Charitable Trusts

- Zoned Out?

Posted by at 10:05 AM

Labels: Global Housing Watch

Tuesday, March 26, 2019

Housing Market in San Marino

From the IMF’s latest report on San Marino:

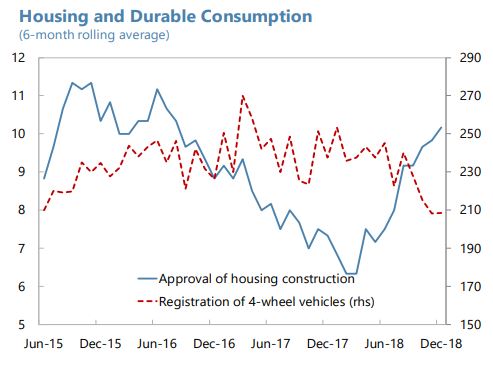

“Housing construction picked up from low levels while car registration has dropped.”

From the IMF’s latest report on San Marino:

“Housing construction picked up from low levels while car registration has dropped.”

Posted by at 11:20 AM

Labels: Global Housing Watch

Friday, March 22, 2019

House Prices in Bulgaria

From the IMF’s latest report on Bulgaria:

“Credit growth has picked up. Both consumer and mortgage loan growth has been buoyant, accompanied by strong housing price increases (averaging 7.5 percent y/y since 2016). Credit to corporates has also been recovering and reached 5.4 percent y/y in 2018, the highest level since 2013, while credit standards have slightly tightened or remained unchanged recently. But non-financial corporate debt remains high among the new member states (NMS)—notwithstanding a marked decline from 106 percent of GDP in 2008 to 80 percent of GDP in 2017. Overall credit-to-GDP ratio remains below the historical trend, with the ratio substantially below the peak reached in 2010.”

From the IMF’s latest report on Bulgaria:

“Credit growth has picked up. Both consumer and mortgage loan growth has been buoyant, accompanied by strong housing price increases (averaging 7.5 percent y/y since 2016). Credit to corporates has also been recovering and reached 5.4 percent y/y in 2018, the highest level since 2013, while credit standards have slightly tightened or remained unchanged recently. But non-financial corporate debt remains high among the new member states (NMS)—notwithstanding a marked decline from 106 percent of GDP in 2008 to 80 percent of GDP in 2017.

Posted by at 4:32 PM

Labels: Global Housing Watch

Housing View – March 22, 2019

On cross-country:

- The Total Risk Premium Puzzle – NBER

- Book review: Order without Design: How Markets Shape Cities by Alain Bertaud – New Geography

- New driveway? Home improvements lead AI to hidden gentrification – Reuters

- Inclusionary Housing Policies in Gothenburg, Sweden, and Stuttgart, Germany: The importance of Norms and Institutions – Nordic Journal of Surveying and Real Estate Research

- We don’t have enough to buy a house. How can we invest with similar returns to real estate? – Globe and Mail

On the US:

- The Fed has exacerbated America’s new housing bubble – Financial Times

- The Affordable Home Crisis Continues, But Bold New Plans May Help – Citylab

- US new home sales fall more than forecast in January – Financial Times

- RE Lending Risks Monitor – Federal Reserve Bank of San Francisco

- Do Credit Conditions Move House Prices? – MIT

- Mortgage Loss Severities: What Keeps Them So High? – Federal Reserve Bank of Philadelphia

- Part 3: Renting Vs. Buying. How Important Is Owning A Home? – wbur

- Bay Area leads charge on fixing housing crisis. Will it work for the rest of California? – Los Angeles Times

- Storper Challenges Blanket Upzoning as Solution to Housing Crisis – UCLA

- How Do Homeowners Spend Their Remodeling Dollars? – Harvard Joint Center for Housing Studies

On other countries:

- [Australia] Property, Debt and Financial Stability – Reserve Bank of Australia

- [Australia] Australia’s falling home prices not yet a threat to banks: RBA – Reuters

- [Australia] Australian Housing Slide Deepens as RBA Worries About Consumers – Bloomberg

- [Australia] Australia’s Housing Slump Isn’t Fazing Mortgage Bond Investors – Bloomberg

- [Australia] How Do Crime Rates Affect Property Prices? – Infrastructure Victoria

- [Australia] Foreign investment in Australian residential properties: House prices and growth of housing construction sector – University of Technology, Melbourne

- [Canada] The Age of Leverage – Bank of Canada

- [Canada] Previous housing data understated amount of non-resident buyers in Vancouver and Toronto – Globe and Mail

- [Canada] Trudeau Targets Home-Buying Millennials With Equity Plan – Bloomberg

- [Canada] Not in my neighbour’s back yard? Laneway homes and neighbours’ property values – University of British Columbia

- [China] Housing Policy and Economic Growth in China – Reserve Bank of Australia

- [China] Deeper Cracks in China’s Housing Foundations – Wall Street Journal

- [China] China new house prices pick up pace in February – Financial Times

- [Czech Republic] Czech apartment price rise continues – ING

- [Iceland] Iceland’s house prices rises decelerating rapidly – Global Property Guide

- [India] As property prices rise, more Indian women claim inheritance – Reuters

- [Ireland] Irish house prices cool further as wider inflation remains muted – Reuters

- [Italy] Renaissance Venice had its own “Airbnb problem”—and a solution … – Quartz

- [Japan] Japan’s Regional Land Prices Rise for First Time Since Property Bubble Burst in ’90s – Bloomberg

- [Malaysia] Housing prices in peninsular Malaysia: supported by income, foreign inflow or speculation? – Tunku Abdul Rahman University College

- [Mexico] Mexico’s housing market is strengthening – Global Property Guide

- [Netherlands] Amsterdam Is Trying to Crack Down on Its Rentals Market – Bloomberg

- [Slovak Republic] Slovak Republic’s house price rises continue – Global Property Guide

- [Switzerland] World’s Lowest Interest Rate Brews Trouble for Swiss Property – Bloomberg

- [United Kingdom] Revealed: the fastest ‘double your money’ years for UK property – Financial Times

- [United Kingdom] Properties, prices and pesky Instagrammers – Financial Times

- [United Kingdom] Elephant and Castle shifts from social housing to ‘build to rent’ – Financial Times

- [United Kingdom] How does the land supply system affect the business of UK speculative housebuilding? – UK Collaborative Centre for Housing Evidence

- [Venezuela] Crisis en Venezuela: la tentadora oferta de viviendas de lujo a precio de saldo (y qué tiene que ver el “efecto Guaidó”) – BBC

On cross-country:

- The Total Risk Premium Puzzle – NBER

- Book review: Order without Design: How Markets Shape Cities by Alain Bertaud – New Geography

- New driveway? Home improvements lead AI to hidden gentrification – Reuters

- Inclusionary Housing Policies in Gothenburg, Sweden, and Stuttgart, Germany: The importance of Norms and Institutions – Nordic Journal of Surveying and Real Estate Research

- We don’t have enough to buy a house.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts