Showing posts with label Forecasting Forum. Show all posts

Monday, February 2, 2015

On Groundhog Day, Honoring A Forecasting Giant

Herman believes that forecasters should predict recessions early and often: “… the cost of a recession is so great that a forecaster should never miss one … Some people argue that turning points are unpredictable. I disagree. I have never had trouble predicting recessions. In fact, I have predicted n+x of the last n recessions.”

Herman’s colleagues and friends organized a conference on his 80th birthday and the proceedings have just been published in a special issue of the International Journal of Forecasting. The conference versions of the papers are available here.

The issue has an article by Fred Joutz, Tara Sinclair and me, which summarizes Herman’s extraordinary career—the early work on forecasting turning points and why forecasters seem to miss nearly every one of them; the first forecasting assessments of the Fed’s Greenbook forecasts; and much more.

Forecasting is difficult and I honor the people who have to do it. My own interest in the topic was triggered by my awful forecasts for growth in the Asian crisis economies in 1997-98. I have continued my own “astonishing record of complete failure” by completely failing to forecast the recent sharp decline in oil prices. I did call the Patriots-Seahawks outcome correctly.

This Groundhog Day I want to honor economic forecasters—and one in particular, Herman Stekler—rather than make fun of them, which is what I’ve tended to do on past Groundhog Days. Herman has had a 60-year career in forecasting and is still making predictions on everything that moves, including Super Bowl games. He recalls that the interview for his first job at Berkeley “occurred during the famous NY Giants–Baltimore Colts championship football game of 1959. Read the full article…

Posted by at 2:21 PM

Labels: Forecasting Forum

Tuesday, April 15, 2014

“There will be growth in the spring”: How well do economists predict turning points?

Forecasters have a poor reputation for predicting recessions. This Vox column quantifies their ability to do so, and explores several reasons why both official and private forecasters may fail to call a recession before it happens.

Forecasters have a poor reputation for predicting recessions. This Vox column quantifies their ability to do so, and explores several reasons why both official and private forecasters may fail to call a recession before it happens.

Posted by at 12:19 PM

Labels: Forecasting Forum

Tuesday, April 8, 2014

IMF’s World Economic Outlook–April 2014

Posted by at 9:38 PM

Labels: Forecasting Forum

Wednesday, March 19, 2014

IMF Releases Independent Assessment of its Forecast Accuracy

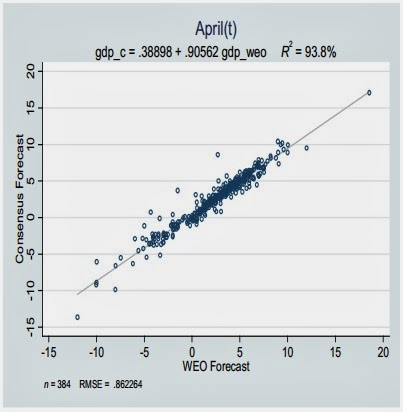

The IMF’s independent evaluation office released its study of IMF Forecasts: Process, Quality, and Country Perspectives. It concludes that “the accuracy of IMF short-term forecasts is comparable to that of private forecasts. Both tend to over predict GDP growth significantly during regional or global recessions, as well as during crises in individual countries.” The study thus confirms the two main findings of my 2001 paper: first, “the record of failure to predict recessions is virtually unblemished,” as I wrote; second, a statistical horse race between private sector and official sector forecasts ends up in a photo finish. My recent work with Hites Ahir looks at the record of professional forecasters in predicting recessions over the period 2008-12, also confirming both findings. The figure shows the close correspondence between Consensus (private sector) and IMF forecasts.

The IMF’s independent evaluation office released its study of IMF Forecasts: Process, Quality, and Country Perspectives. It concludes that “the accuracy of IMF short-term forecasts is comparable to that of private forecasts. Both tend to over predict GDP growth significantly during regional or global recessions, as well as during crises in individual countries.” The study thus confirms the two main findings of my 2001 paper: first, “the record of failure to predict recessions is virtually unblemished,” as I wrote;

Posted by at 12:57 PM

Labels: Forecasting Forum

Friday, August 16, 2013

The Stock Market ‘Prediction Charade’

“The next time you are tempted to rely on forecasts of experts in making investment decisions, remember these words attributed to Prakash Loungani of the International Monetary Fund: “The record of failure to predict recessions is virtually unblemished.” Read the full story here.

“The next time you are tempted to rely on forecasts of experts in making investment decisions, remember these words attributed to Prakash Loungani of the International Monetary Fund: “The record of failure to predict recessions is virtually unblemished.” Read the full story here.

Posted by at 2:07 PM

Labels: Forecasting Forum

Subscribe to: Posts