Showing posts with label Forecasting Forum. Show all posts

Thursday, February 1, 2018

How Well Do Economists Forecast Recessions? A Groundhog Day Update

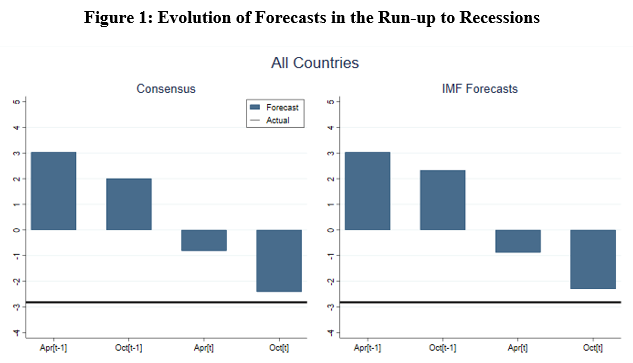

In 2000, I wrote in the Financial Times that “the record of failure to predict recessions is virtually unblemished.” In time for Groundhog Day, my colleague Zidong An, Joao Jalles and I have updated my analysis so that it now covers the years 1992 to 2014 and 63 countries. We find that there is little reason to change my assessment. Like Bill Murray, I am reliving the same moment.

In 2000, I wrote in the Financial Times that “the record of failure to predict recessions is virtually unblemished.” In time for Groundhog Day, my colleague Zidong An, Joao Jalles and I have updated my analysis so that it now covers the years 1992 to 2014 and 63 countries. We find that there is little reason to change my assessment. Like Bill Murray, I am reliving the same moment.

Posted by at 10:53 AM

Labels: Forecasting Forum

Wednesday, January 24, 2018

FocusEconomics Announces 2017 Analyst Forecast Awards Winners

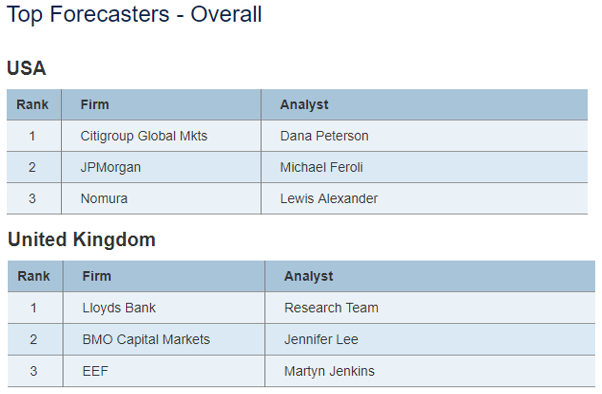

FocusEconomics announces the winners of our 2017 Analyst Forecast Awards. “The Awards recognize the most accurate forecasters for the main macroeconomic indicators across 87 countries and 29 commodity prices in 2016. Details of the awards and the list of winners are available at: www.focus-economics.com/awards.”

FocusEconomics announces the winners of our 2017 Analyst Forecast Awards. “The Awards recognize the most accurate forecasters for the main macroeconomic indicators across 87 countries and 29 commodity prices in 2016. Details of the awards and the list of winners are available at: www.focus-economics.com/awards.”

Posted by at 6:43 PM

Labels: Forecasting Forum

Thursday, January 4, 2018

GDP growth forecasts and information flows: Is there evidence of overreactions?

In a new paper, Daniel Aromi shows that “excessive optimism after the arrival of positive information” for a few years about a country’s prospects can lead to large forecast errors when the information turns negative but forecasts don’t.

“[…] some years before the Asian crisis, Krugman (1994) warned against ‘popular enthusiasm about Asia’s boom’. More recently, Pritchett and Summers (2014) indicate that growth expectations regarding the Chinese and Indian economies might suffer from excessive extrapolation of recent trajectories. In addition to these warnings, further motivation is provided by macroeconomic episodes in which improved economic prospects are followed by crises. For instance, several European economies, among them Greece and Ireland, went through this type of trajectory. Another case is given by recent events in Brazil, where prominent optimism regarding economic prospects was later proven wrong in a stark manner.”

“The empirical analysis shows a significant association between mean forecast errors and earlier information flows. The sign of the documented relationship is consistent with the overreaction hypothesis. More positive information is followed, on average, by higher forecast errors, that is, by increments in the mean difference between forecast growth and realized growth.”

“It is worth noting that the strongest evidence is documented for information flows and forecasts errors that are between 4 and 8 years apart. In other words, the evidence indicates the presence of a process that develops at a frequency that is lower than the usual business cycle frequency.”

“This work documents the presence of systematic errors in growth forecasts. Mean forecast errors are positively associated with the tone of information flows observed in previous periods.”

“The inefficient use of information and the associated errors in decision-making could explain economically significant aggregate fluctuations. In particular, excessive optimism after the arrival of positive information can contribute to the emergence of vulnerabilities that increase the likelihood of economic crises.”

The article is available from the International Finance.

In a new paper, Daniel Aromi shows that “excessive optimism after the arrival of positive information” for a few years about a country’s prospects can lead to large forecast errors when the information turns negative but forecasts don’t.

“[…] some years before the Asian crisis, Krugman (1994) warned against ‘popular enthusiasm about Asia’s boom’. More recently, Pritchett and Summers (2014) indicate that growth expectations regarding the Chinese and Indian economies might suffer from excessive extrapolation of recent trajectories.

Posted by at 10:41 AM

Labels: Forecasting Forum

David Hendry on Why Forecasting Fails

The noted econometrician writes: “The intermittent failure of economic forecasts to ‘foresee’ the future reflects both imperfect knowledge and a non-stationary and evolving world that is far from ‘general equilibrium’ and closer to ‘general disequilibrium’.”

“[This has] disastrous consequences for dynamic stochastic general equilibrium (DSGE) systems, which transpire to be the least structural of all possible model forms as their derivation entails they are bound to ‘break down’ when the underlying distributions of economic variables shift. This serious problem is highlighted by Hendry and Muellbauer (2017) in their critique of the Bank of England quarterly econometric model (BEQEM–pronounced Beckem: […] a DSGE which, as in the film ‘Bend it Like Beckham’, bent in the Financial Crisis, but so much that it broke and had to be replaced.”

“Surprisingly, despite that abject failure, it was replaced by yet another DSGE (COMPASS: Central Organising Model for Projection Analysis and Scenario Simulation […]. Unfortunately, […] COMPASS had already failed to characterize data available before it was even developed. Persisting with such an approach introduces a triple whammy as:

a] the derivations sustaining DSGEs use an invalid mathematical basis;

b] imposing a so-called ‘equilibrium’ fails to take account of past shifts;

c] the DSGE approach assumes agents act in the same incorrect way as the modeller, so assumes agents have failed to learn that imperfect knowledge about location shifts forces revisions to their plans.”

“During a visit to LSE in 2009, Queen Elizabeth II asked Luis Garicano “why did no one see the credit crisis coming?” to which a part of his answer should have been that DSGE models dominated economic agencies and essentially ruled out such major financial crises by assuming away imperfect knowledge. Prakash Loungani (2001) argued “The record of failure to predict recessions is virtually unblemished.””

The article is available from the here.

The noted econometrician writes: “The intermittent failure of economic forecasts to ‘foresee’ the future reflects both imperfect knowledge and a non-stationary and evolving world that is far from ‘general equilibrium’ and closer to ‘general disequilibrium’.”

“[This has] disastrous consequences for dynamic stochastic general equilibrium (DSGE) systems, which transpire to be the least structural of all possible model forms as their derivation entails they are bound to ‘break down’ when the underlying distributions of economic variables shift.

Posted by at 10:33 AM

Labels: Forecasting Forum

Thursday, December 14, 2017

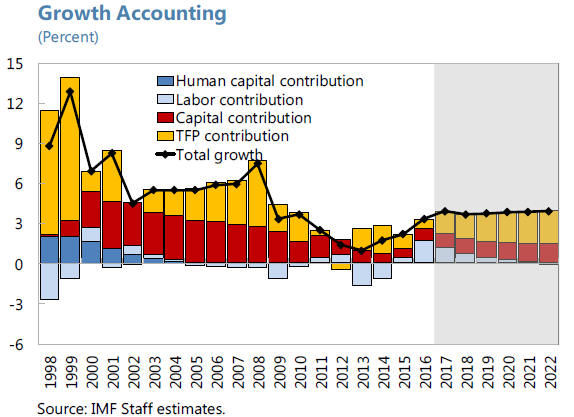

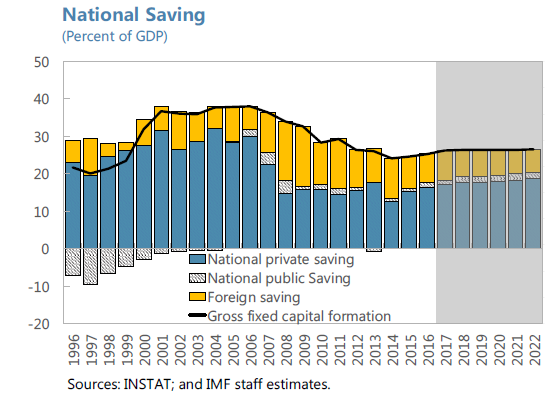

Medium Term Growth in Albania

IMF’s latest report says that “Growth in Albania is recovering but has recently been driven by large FDI projects, raising concerns about the sustainability of the recovery and underlying growth potential. This study assesses the prospects and challenges for medium term growth. While Albania’s external conditions are favorable, low savings and demographic trends are expected to weigh on investment and labor utilization. However, EU accession literature suggests that institutional reforms as an EU candidate country can catalyze productivity improvements and potential growth in Albania.”

IMF’s latest report says that “Growth in Albania is recovering but has recently been driven by large FDI projects, raising concerns about the sustainability of the recovery and underlying growth potential. This study assesses the prospects and challenges for medium term growth. While Albania’s external conditions are favorable, low savings and demographic trends are expected to weigh on investment and labor utilization. However, EU accession literature suggests that institutional reforms as an EU candidate country can catalyze productivity improvements and potential growth in Albania.”

Posted by at 10:31 AM

Labels: Forecasting Forum, Inclusive Growth

Subscribe to: Posts