Showing posts with label Forecasting Forum. Show all posts

Wednesday, May 9, 2018

GDP Growth Rate Projection in Asia Pacific

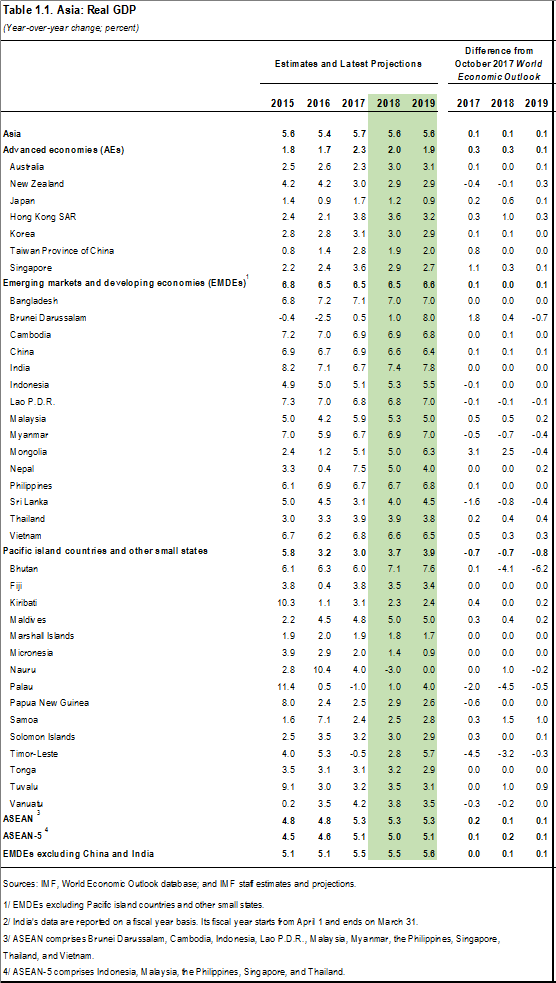

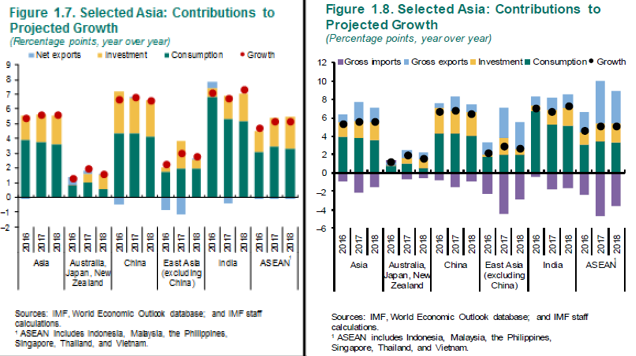

The new IMF Regional Economic Outlook for Asia Pacific says that “Growth in Asian economies has picked up in line with global developments. Asia grew by 5.7 percent in 2017, up 0.3 of a percent from the year before, with the pickup broad-based across the region (Table 1.1). Asia continues to be both the fastest-growing region in the world and the main engine of the world’s economy, contributing more than 60 percent of global growth (three-quarters of which comes from China and India) (Figure 1.6). Consumption and investment continue to be major contributors. The contribution of net exports remained small, but the strong growth of gross exports and imports suggests that the recovery in external demand (both inside and outside the region) was an important driver of GDP growth in Asia (Figures 1.7 and 1.8).”

The new IMF Regional Economic Outlook for Asia Pacific says that “Growth in Asian economies has picked up in line with global developments. Asia grew by 5.7 percent in 2017, up 0.3 of a percent from the year before, with the pickup broad-based across the region (Table 1.1). Asia continues to be both the fastest-growing region in the world and the main engine of the world’s economy, contributing more than 60 percent of global growth (three-quarters of which comes from China and India) (Figure 1.6).

Posted by at 3:46 PM

Labels: Forecasting Forum

Thursday, May 3, 2018

Retail Apocalypse Postponed Not Cancelled

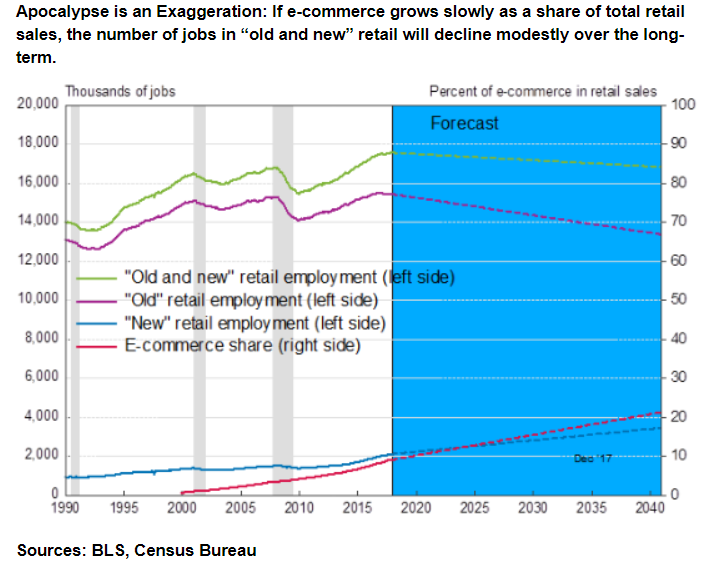

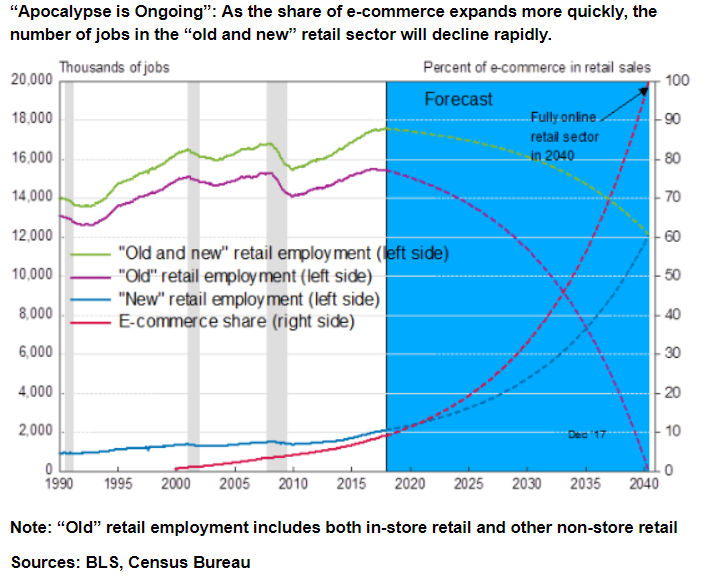

A new post by Brian Schaitkin says that “Economist Michael Mandel of the Progressive Policy Institute tells a reassuring story about what will happen to retail employment. Jobs behind retail counters and stocking store aisles will simply be replaced by jobs at warehouses, e-commerce facilities, and as delivery drivers.” How quickly will this happen? He provides forecasts under the “Apocalypse is an Exaggeration” and “Apocalypse is Ongoing” scenarios:

“[…] Under an “Apocalypse is an Exaggeration” scenario, e-commerce will grow at a modest pace as a share of total retail sales because many of the lowest hanging e-commerce fruit have already been plucked. Therefore, the transformation from in-store retail to e-commerce would take quite a long time. The logistical challenge of shipping books to individual customers is orders of magnitude less complicated than delivering groceries. The “in-store” experience also provides special value to some consumers, especially when the ability to touch and feel merchandise and consult with experts is part of the value proposition stores and their workers provide. Firms will learn how to adapt to the challenge of e-commerce in less easily adapted industries, but because of these challenges, growth in the e-commerce share may increase by only 6.8 percent every 13 years, as happened between 2005 and 2017. Under this scenario, the share of e-commerce in retail sales would be 21 percent by the end of 2040, and the “old and new” retail sector will employ 16.8 million workers, compared to 17.6 million today. A disappointing job trajectory to be sure, but hardly apocalyptic.”

“The 2005 to 2017 period though lights the way to a bolder, yet in my view more likely “Apocalypse is Ongoing” scenario. This scenario assumes that exponential growth of the e-commerce share will continue as it did from 2005 to 2017 meaning that the e-commerce share of retail will double every 6.5 years. Incentives for firms to adapt new sectors to e-commerce will be tremendous due to the convenience and efficiency commerce without stores can provide. Companies can apply the lessons from developing one form of e-commerce to new product areas with knowledge of the pitfalls they are likely to encounter. Under this scenario, e-commerce would represent 18 percent of retail sales by the middle of 2024, 36 percent by the end of 2030, and 100 percent by the middle of 2040. Initially, job losses resulting from the shift to e-commerce would be small in “old and new” retail with 738,000 jobs disappearing between now and the end of 2025. By 2040, however, only 12.1 million workers, all employed by “new” retail sectors, would be able to manage all retail sales activities, a loss of 5.5 million jobs.”

Continue reading here.

A new post by Brian Schaitkin says that “Economist Michael Mandel of the Progressive Policy Institute tells a reassuring story about what will happen to retail employment. Jobs behind retail counters and stocking store aisles will simply be replaced by jobs at warehouses, e-commerce facilities, and as delivery drivers.” How quickly will this happen? He provides forecasts under the “Apocalypse is an Exaggeration” and “Apocalypse is Ongoing” scenarios:

“[…] Under an “Apocalypse is an Exaggeration” scenario,

Posted by at 10:13 AM

Labels: Forecasting Forum, Inclusive Growth

Monday, April 30, 2018

Forecasting Forum – April 2018

New Blogs:

Global Economy: Good News for Now but Trade Tensions a Threat – IMF Blog by Maurice Obstfeld

Econometrics, Machine Learning, and Big Data – No Hesitations (Frank Diebold’s Blog)

2018’s Growing and Shrinking Economies – Focus Economics

A brief history of time series forecasting competitions – Hyndsight (Rob Hyndman’s Blog)

IJF special issue on “Forecasting for Social Good” – IIF Blog

Ghysels and Marcellino on Time-Series Forecasting – No Hesitations (Frank Diebold’s Blog)

What impact would a trade war between the U.S. and China have on their economies? – Focus Economics

What Information Does the Yield Curve Yield? – ECONOFACT

New Articles:

Forecasting US GNP growth: The role of uncertainty – Mawuli Segnon, Rangan Gupta, Stelios Bekiros, and Mark E. Wohar, Journal of Forecasting

Are macroeconomic density forecasts informative? – Michael P. Clements, International Journal of Forecasting

The role of accounting fundamentals and other information in analyst forecast errors – Danilo Monte‐Mor, Fernando Galdi, and Cristiano Costa, Journal of International Finance

What do professional forecasters actually predict? – Didier Nibbering, Richard Paap, and Michel van der Wel, International Journal of Forecasting

How well do economists forecast recessions? – Zidong An, Joao Jalles, and Prakash Loungani, International Finance

Evaluating the use of realtime data in forecasting output levels and recessionary events in the USA – Chrystalleni Aristidou, Kevin Lee, and Kalvinder Shields, Journal of the Royal Statistical Society

New Blogs:

Global Economy: Good News for Now but Trade Tensions a Threat – IMF Blog by Maurice Obstfeld

Econometrics, Machine Learning, and Big Data – No Hesitations (Frank Diebold’s Blog)

2018’s Growing and Shrinking Economies – Focus Economics

A brief history of time series forecasting competitions – Hyndsight (Rob Hyndman’s Blog)

IJF special issue on “Forecasting for Social Good” – IIF Blog

Ghysels and Marcellino on Time-Series Forecasting – No Hesitations (Frank Diebold’s Blog)

Posted by at 9:51 AM

Labels: Forecasting Forum

Friday, April 27, 2018

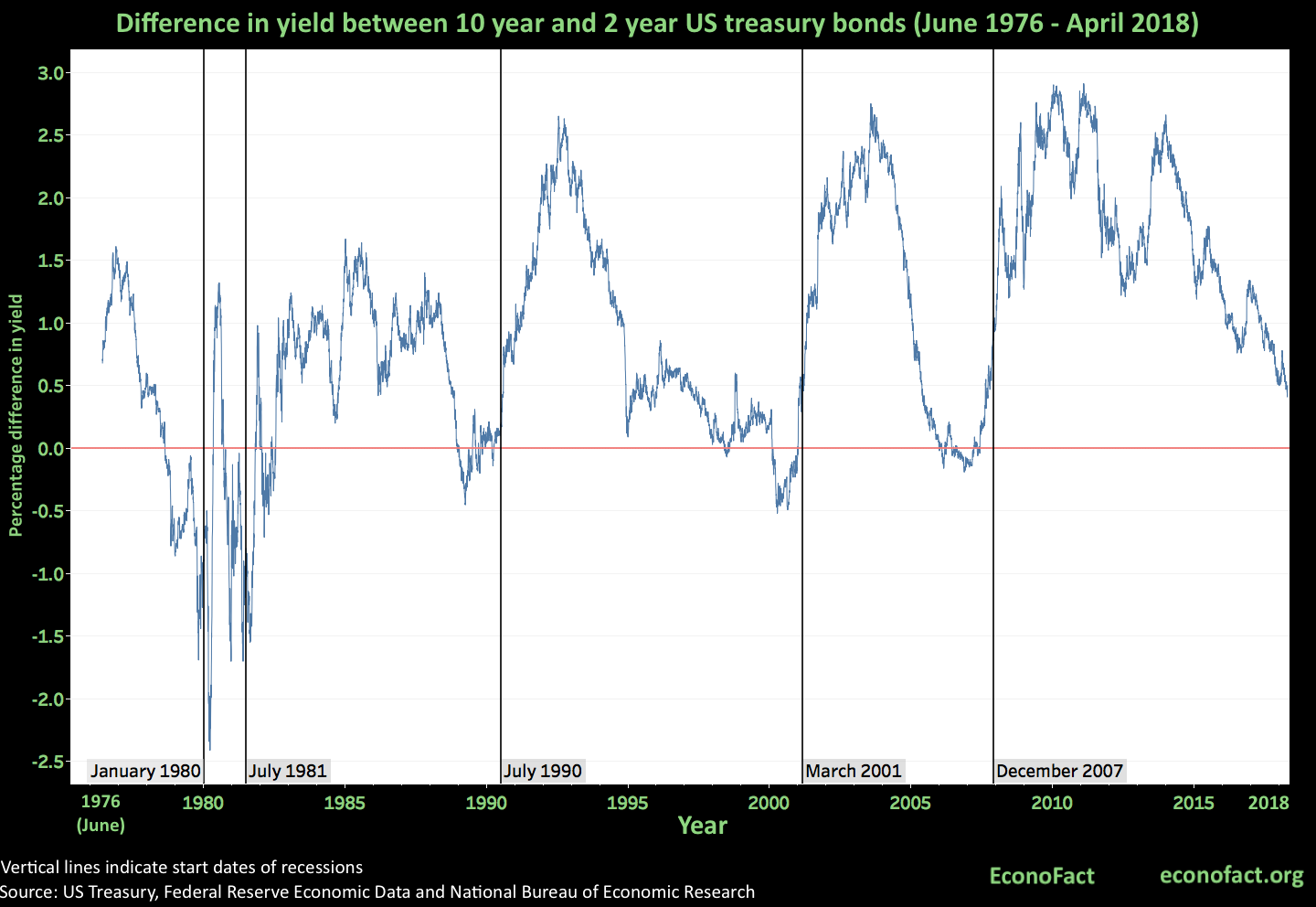

What Information Does the Yield Curve Yield?

A new post by Michael W. Klein shares the concern about the possibility of an upcoming recession that “Forecasting the twists and turns of the economy is difficult. One set of indicators used to gauge where the economy is headed draws on information from financial markets since the yields paid by financial assets reflect the collective market view of the future state of the economy. An inverted yield curve — when interest rates on short-term Treasury bonds exceed those on longer-term Treasury bonds — has in the past proven to be a strong indicator of an oncoming recession. While the U.S. economy is not currently experiencing an inverted yield curve, the difference in yields between shorter- and longer-term Treasury bonds has narrowed. The movements in the yield curve, as well as in other financial market indicators, have raised concerns that the current long expansion of the United States economy may be coming to an end.”

Continue reading here. Also see my previous post on forecasting recessions.

A new post by Michael W. Klein shares the concern about the possibility of an upcoming recession that “Forecasting the twists and turns of the economy is difficult. One set of indicators used to gauge where the economy is headed draws on information from financial markets since the yields paid by financial assets reflect the collective market view of the future state of the economy. An inverted yield curve — when interest rates on short-term Treasury bonds exceed those on longer-term Treasury bonds — has in the past proven to be a strong indicator of an oncoming recession.

Posted by at 3:53 PM

Labels: Forecasting Forum

Monday, April 9, 2018

Financial Times: IMF Shows Poor Track Record at Forecasting Recessions

The FT cites my new working paper with Zidong An and Joao Jalles:

“Recessions are not rare,” echoed Prakash Loungani, a macro-economist at the IMF. “What is rare is a recession that is forecast in advance.” Despite an increased amount of economic data being available, “the ability to predict downturns remains dismal”, he told the FT.”

[…]

The fact that forecasts are “typically over-optimistic for horizons beyond the current year” is not necessarily the result of economist optimism. They “fail to forecast strong booms, just as they fail to predict recessions,” said Mr Loungani, suggesting that economic forecasts “are too rooted in thinking that things stay close to normal or will revert to normal soon”.

[…]

“The IMF’s April outlook is often more accurate. This is because it is easier to get a forecast right for the current year than the following year. The April report is better able to signal a recession for the current year than the October publication, “but one that is much milder than what transpires”, says Mr Loungani, author of several studies.”

Continue reading here.

The FT cites my new working paper with Zidong An and Joao Jalles:

“Recessions are not rare,” echoed Prakash Loungani, a macro-economist at the IMF. “What is rare is a recession that is forecast in advance.” Despite an increased amount of economic data being available, “the ability to predict downturns remains dismal”, he told the FT.”

[…]

The fact that forecasts are “typically over-optimistic for horizons beyond the current year”

Posted by at 11:08 AM

Labels: Forecasting Forum

Subscribe to: Posts