Showing posts with label Forecasting Forum. Show all posts

Tuesday, May 22, 2018

The FOMC versus the Staff, Revisited: When do Policymakers Add Value?

A new paper finds that “policymakers’ value-added is greater when economic conditions are unfavorable or uncertain.” “[…] in certain circumstances, the value of the FOMC’s informational advantage and judgement-based adjustments to the staff forecasts is greater. The use of explicit formal models for quantitative macroeconomic forecasting proliferated in the 1960s, but forecasters typically adjust the model-based forecasts using their own judgment (Wallis, 1989). There is mixed evidence on the value of “judgmental adjustments,” which can introduce psychological biases but can also compensate for model limitations, and

may be especially valuable when economic events lack close historical precedents (McNees, 1990).”

A new paper finds that “policymakers’ value-added is greater when economic conditions are unfavorable or uncertain.” “[…] in certain circumstances, the value of the FOMC’s informational advantage and judgement-based adjustments to the staff forecasts is greater. The use of explicit formal models for quantitative macroeconomic forecasting proliferated in the 1960s, but forecasters typically adjust the model-based forecasts using their own judgment (Wallis, 1989). There is mixed evidence on the value of “judgmental adjustments,”

Posted by at 11:11 AM

Labels: Forecasting Forum

Thursday, May 17, 2018

Biggest fear for world growth is fear itself as markets fret

A new Bloomberg post by Anchalee Worrachate and David Goodman says that: “While policy makers insist the global economy’s low-inflation expansion looks intact despite a first quarter slowdown, investors are presenting challenges. Rising bond yields, a jump in the price of oil beyond $70 a barrel, skittish stocks and cracks in credit could all end up undermining growth.” “The worry is that unless markets start buying into the more optimistic outlook, their pessimism will become self-fulfilling by causing consumers and companies to lose confidence and slow spending. The Bank for International Settlements warned last year that the next recession will perhaps be triggered by a financial cycle bust, mirroring the events of 2001 and 2008.”

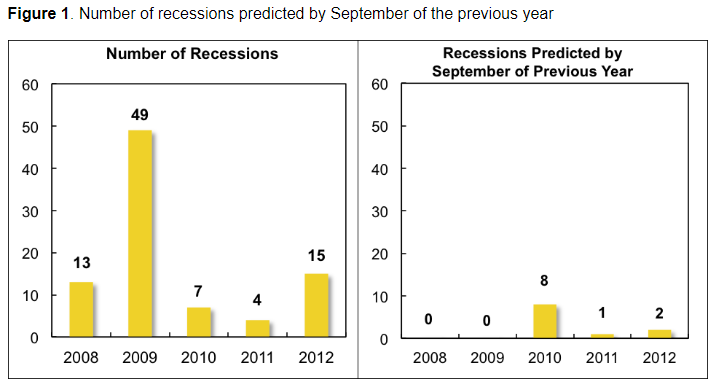

This post also notes my research that “the optimism of analysts may be cold comfort to some investors. A 2014 study by Prakash Loungani of the International Monetary Fund found that not one of 49 recessions suffered around the world in 2009 had been predicted by the consensus of economists a year earlier.”

Continue reading here. My Vox post is available here. My new paper on forecasting recessions is available here.

A new Bloomberg post by Anchalee Worrachate and David Goodman says that: “While policy makers insist the global economy’s low-inflation expansion looks intact despite a first quarter slowdown, investors are presenting challenges. Rising bond yields, a jump in the price of oil beyond $70 a barrel, skittish stocks and cracks in credit could all end up undermining growth.” “The worry is that unless markets start buying into the more optimistic outlook, their pessimism will become self-fulfilling by causing consumers and companies to lose confidence and slow spending.

Posted by at 11:08 AM

Labels: Forecasting Forum

Thursday, May 10, 2018

Lawrence R. Klein and the making of large-scale macro-econometric modeling, 1938-1955

From new Documentos CEDE by Erich Pinzón-Fuchs:

“Lawrence R. Klein was the father of macro-econometric modeling, the scientific practice that dominated macroeconomics throughout the second half of the twentieth century. Therefore, understanding how Klein developed his identity as a macro-econometrician and how he conceived and forged macro-econometric modeling at the same time, is essential to draw a clear picture of the origins and subsequent development of this scientific practice in the United States. To this aim, I focus on Klein’s early trajectory as a student of economics and as an economist (from 1938-1955), and I particularly examine the extent to which the people and institutions Klein encountered helped him shape his professional identity. Klein’s experience at places like Berkeley, MIT, Cowles, and the University of Michigan, as well as his early acquaintance with people such as Griffith Evans, Paul Samuelson, and Trygve Haavelmo were decisive in the formation of his idea on how econometrics, expert knowledge, mathematical rigor, and a specific institutional configuration should enter macro-econometric modeling. Although Klein’s identity defined some of the most important characteristics of this practice, by the end of the 1950s, macro-econometric modeling became a scientific practice independent of Klein’s enthusiasm and with a “life of its own,” ready to be further developed and adapted to specific contexts by the community of macroeconomists.” Picture from Nobelprize.org.

Picture from Nobelprize.org.

From new Documentos CEDE by Erich Pinzón-Fuchs:

“Lawrence R. Klein was the father of macro-econometric modeling, the scientific practice that dominated macroeconomics throughout the second half of the twentieth century. Therefore, understanding how Klein developed his identity as a macro-econometrician and how he conceived and forged macro-econometric modeling at the same time, is essential to draw a clear picture of the origins and subsequent development of this scientific practice in the United States.

Posted by at 10:50 AM

Labels: Forecasting Forum, Profiles of Economists

Macroeconomic Forecasting in Germany has changed after the Great Recession?

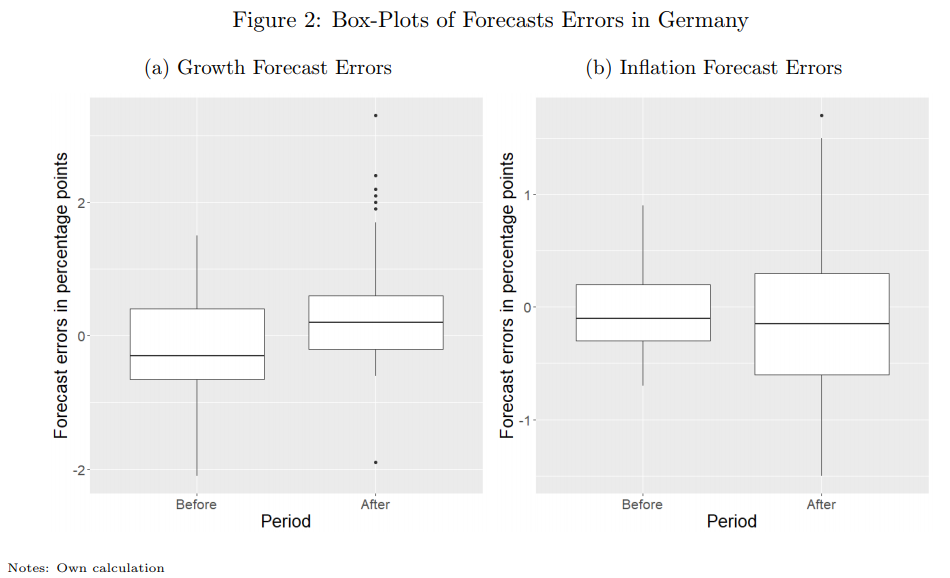

From a new paper by Jörg Döpke, Ulrich Fritsche, and Karsten Müller:

“Based on a panel of annual data for 17 growth and inflation forecasts from 14 institutions for Germany, we analyse forecast accuracy for the periods before and after the Great Recession, including measures of directional change accuracy based on Receiver Operating Curves (ROC). We find only small differences on forecast accuracy between both time periods. We test whether the conditions for forecast rationality hold in both time periods. We document an increased crosssection variance of forecasts and a changed correlation between inflation and growth forecast errors after the crisis, which might hint to a changed forecaster behaviour. This is also supported by estimated loss functions before and after the crisis, which suggest a stronger incentive to avoid overestimations (growth) and underestimations (inflation) after the crisis. Estimating loss functions for a 10—year rolling window also reveal shifts in the level and direction of loss asymmetry and strengthens the impression of a changed forecaster behaviour after the Great Recession.”

From a new paper by Jörg Döpke, Ulrich Fritsche, and Karsten Müller:

“Based on a panel of annual data for 17 growth and inflation forecasts from 14 institutions for Germany, we analyse forecast accuracy for the periods before and after the Great Recession, including measures of directional change accuracy based on Receiver Operating Curves (ROC). We find only small differences on forecast accuracy between both time periods. We test whether the conditions for forecast rationality hold in both time periods.

Posted by at 10:43 AM

Labels: Forecasting Forum

Wednesday, May 9, 2018

GDP Growth Rate Projection in Asia Pacific

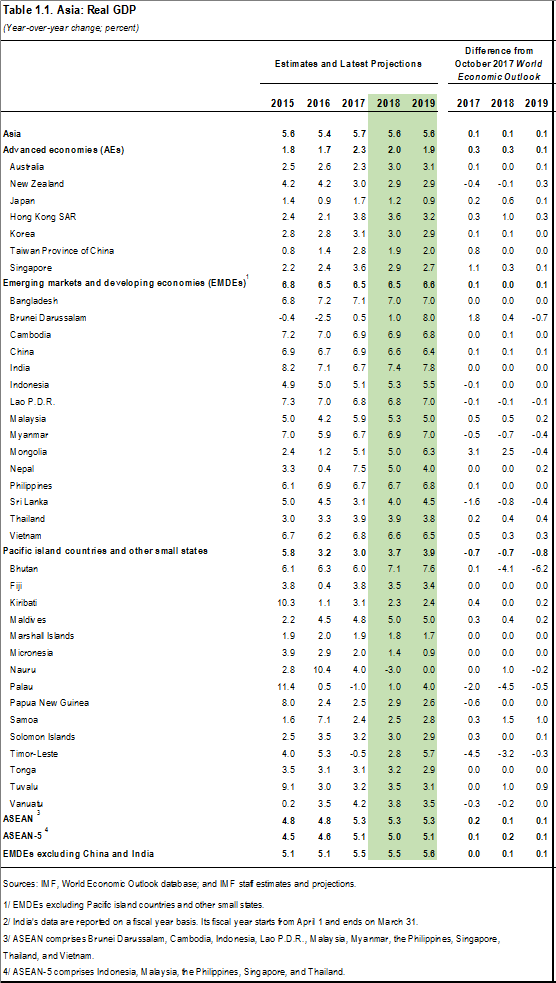

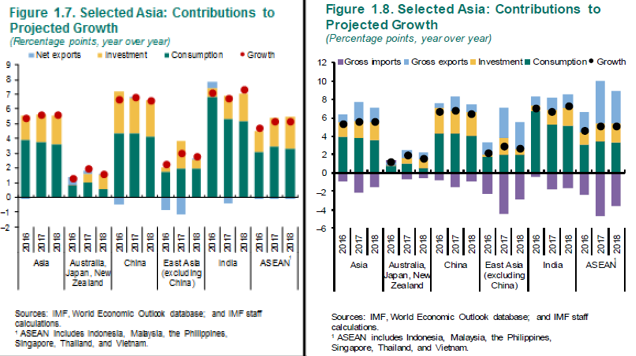

The new IMF Regional Economic Outlook for Asia Pacific says that “Growth in Asian economies has picked up in line with global developments. Asia grew by 5.7 percent in 2017, up 0.3 of a percent from the year before, with the pickup broad-based across the region (Table 1.1). Asia continues to be both the fastest-growing region in the world and the main engine of the world’s economy, contributing more than 60 percent of global growth (three-quarters of which comes from China and India) (Figure 1.6). Consumption and investment continue to be major contributors. The contribution of net exports remained small, but the strong growth of gross exports and imports suggests that the recovery in external demand (both inside and outside the region) was an important driver of GDP growth in Asia (Figures 1.7 and 1.8).”

The new IMF Regional Economic Outlook for Asia Pacific says that “Growth in Asian economies has picked up in line with global developments. Asia grew by 5.7 percent in 2017, up 0.3 of a percent from the year before, with the pickup broad-based across the region (Table 1.1). Asia continues to be both the fastest-growing region in the world and the main engine of the world’s economy, contributing more than 60 percent of global growth (three-quarters of which comes from China and India) (Figure 1.6).

Posted by at 3:46 PM

Labels: Forecasting Forum

Subscribe to: Posts