Showing posts with label Forecasting Forum. Show all posts

Sunday, July 29, 2018

Difficulties of Making Predictions: Global Power Politics Edition

A new post by Timothy Taylor says that “Making predictions is hard, especially about the future. It’s a comment that seems to have been attributed to everyone from Nostradamus to Niels Bohr to Yogi Berra. But it’s deeply true. Most of us have a tendency to make statements about the future with a high level of self-belief, avoid later reconsidering how wrong we were, and then make more statements. […] The questions of how to predict for what you don’t expect, and how to plan for what you don’t expect, are admittedly difficult. The ability to pivot smoothly to face the new challenge may be one of the most underrated skills in politics and management. ”

Continue reading here.

A new post by Timothy Taylor says that “Making predictions is hard, especially about the future. It’s a comment that seems to have been attributed to everyone from Nostradamus to Niels Bohr to Yogi Berra. But it’s deeply true. Most of us have a tendency to make statements about the future with a high level of self-belief, avoid later reconsidering how wrong we were, and then make more statements. […] The questions of how to predict for what you don’t expect,

Posted by at 3:45 PM

Labels: Forecasting Forum

Saturday, July 21, 2018

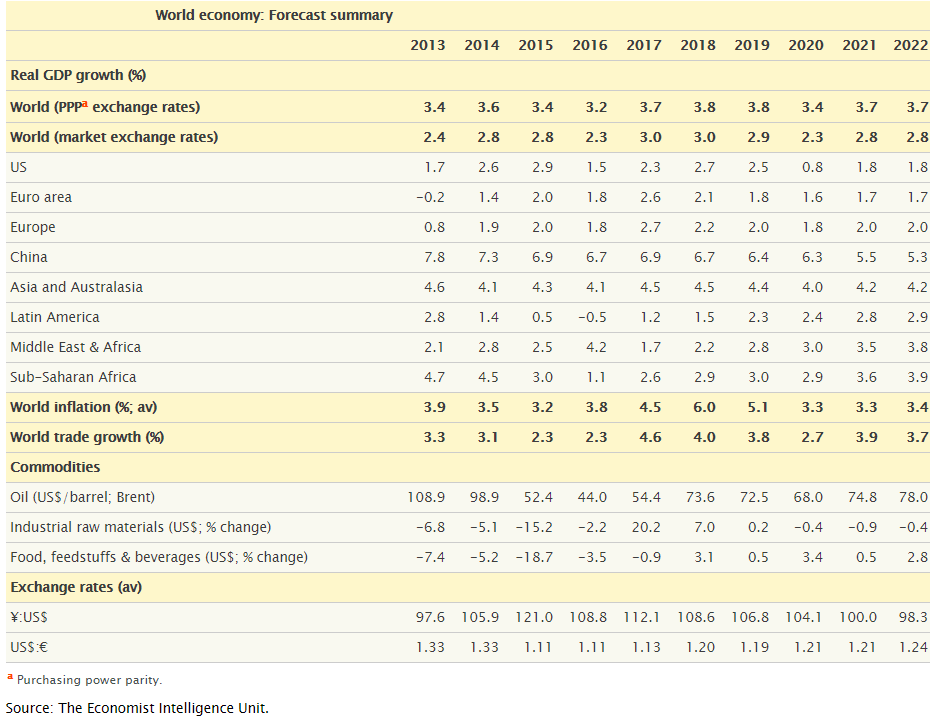

EIU global forecast – Growth will slow in 2019

From the most recent EIU global forecast:

Posted by at 4:36 PM

Labels: Forecasting Forum

Is the Cycle the Trend? Evidence from the Views of International Forecasters

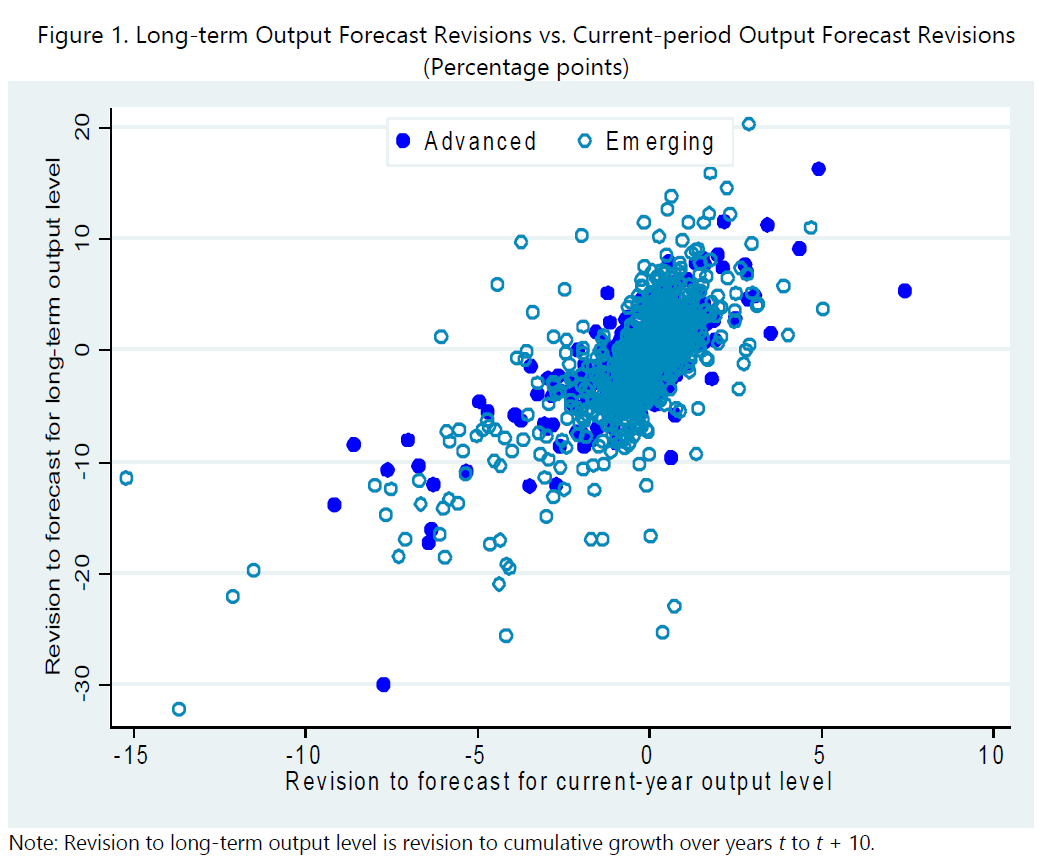

A new IMF working paper by John Bluedorn and Daniel Leigh revisits “the conventional view that output fluctuates around a stable trend by analyzing professional long-term forecasts for 38 advanced and emerging market economies. If transitory deviations around a trend dominate output fluctuations, then forecasters should not change their long-term output level forecasts following an unexpected change in current period output. By contrast, an analysis of Consensus Economics forecasts since 1989 suggest that output forecasts are super-persistent—an unexpected 1 percent upward revision in current period output typically translates into a revision of ten year-ahead forecasted output by about 2 percent in both advanced and emerging markets. Drawing upon evidence from the behavior of forecast errors, the persistence of actual output is typically weaker than forecasters expect, but still consistent with output shocks normally having large and permanent level effects.”

A new IMF working paper by John Bluedorn and Daniel Leigh revisits “the conventional view that output fluctuates around a stable trend by analyzing professional long-term forecasts for 38 advanced and emerging market economies. If transitory deviations around a trend dominate output fluctuations, then forecasters should not change their long-term output level forecasts following an unexpected change in current period output. By contrast, an analysis of Consensus Economics forecasts since 1989 suggest that output forecasts are super-persistent—an unexpected 1 percent upward revision in current period output typically translates into a revision of ten year-ahead forecasted output by about 2 percent in both advanced and emerging markets.

Posted by at 1:11 PM

Labels: Forecasting Forum

Monday, July 16, 2018

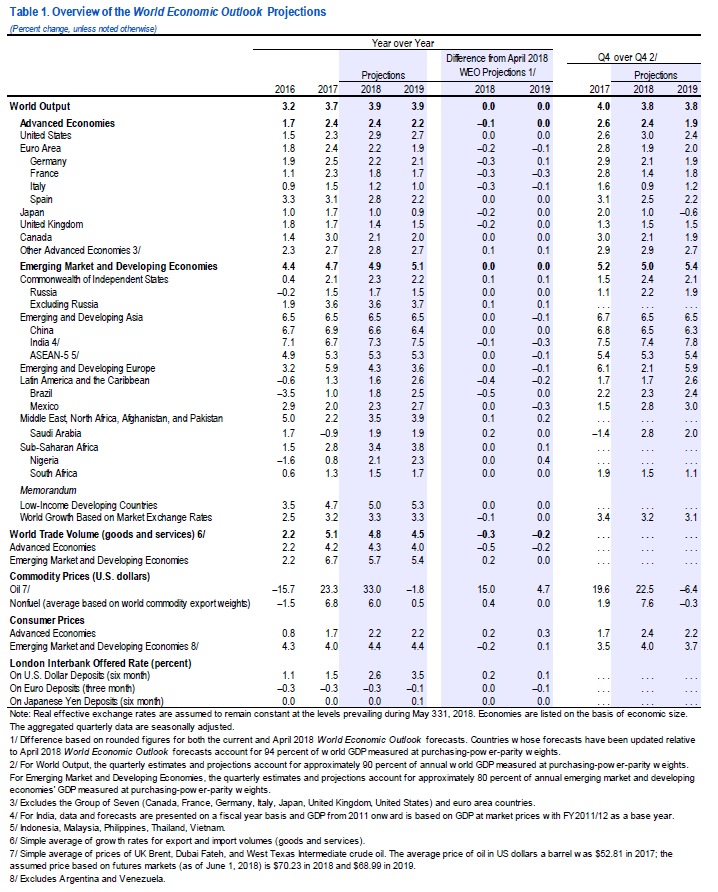

WEO July 2018: Less Even Expansion, Rising Trade Tensions

From the World Economic Outlook Update, July 2018:

“Global growth is projected to reach 3.9 percent in 2018 and 2019, in line with the forecast of the April 2018 World Economic Outlook (WEO), but the expansion is becoming less even, and risks to the outlook are mounting. The rate of expansion appears to have peaked in some major economies and growth has become less synchronized. In the United States, near-term momentum is strengthening in line with the April WEO forecast, and the US dollar has appreciated by around 5 percent in recent weeks. Growth projections have been revised down for the euro area, Japan, and the United Kingdom, reflecting negative surprises to activity in early 2018. Among emerging market and developing economies, growth prospects are also becoming more uneven, amid rising oil prices, higher yields in the United States, escalating trade tensions, and market pressures on the currencies of some economies with weaker fundamentals. Growth projections have been revised down for Argentina, Brazil, and India, while the outlook for some oil exporters has strengthened.

The balance of risks has shifted further to the downside, including in the short term. The recently announced and anticipated tariff increases by the United States and retaliatory measures by trading partners have increased the likelihood of escalating and sustained trade actions. These could derail the recovery and depress medium-term growth prospects, both through their direct impact on resource allocation and productivity and by raising uncertainty and taking a toll on investment. Financial market conditions remain accommodative for advanced economies—with compressed spreads, stretched valuations in some markets, and low volatility—but this could change rapidly. Possible triggers include rising trade tensions and conflicts, geopolitical concerns, and mounting political uncertainty. Higher inflation readings in the United States,where unemployment is below 4 percent but markets are pricing in a much shallower path of interest rate increases than the one in the projections of the Federal Open Market Committee,could also lead to a sudden reassessment of fundamentals and risks by investors. Tighter financial conditions could potentially cause disruptive portfolio adjustments, sharp exchange rate movements, and further reductions in capital inflows to emerging markets, particularly those with weaker fundamentals or higher political risks.

Avoiding protectionist measures and finding a cooperative solution that promotes continued growth in goods and services trade remain essential to preserve the global expansion. Policies and reforms should aim at sustaining activity, raising medium-term growth, and enhancing its inclusiveness. But with reduced slack and downside risks mounting, many countries need to rebuild fiscal buffers to create policy space for the next downturn and strengthen financial resilience to an environment of possibly higher market volatility.”

From the World Economic Outlook Update, July 2018:

“Global growth is projected to reach 3.9 percent in 2018 and 2019, in line with the forecast of the April 2018 World Economic Outlook (WEO), but the expansion is becoming less even, and risks to the outlook are mounting. The rate of expansion appears to have peaked in some major economies and growth has become less synchronized. In the United States, near-term momentum is strengthening in line with the April WEO forecast,

Posted by at 11:13 PM

Labels: Forecasting Forum, Inclusive Growth

Friday, July 6, 2018

Climate Change and NYU Volatility Institute

From Francis Diebold’s Blog:

“There is little doubt that climate change — tracking, assessment, and hopefully its eventual mitigation — is the burning issue of our times. Perhaps surprisingly, time-series econometric methods have much to offer for weather and climatological modeling (e.g., here), and several econometric groups in the UK, Denmark, and elsewhere have been pushing the agenda forward.

Now the NYU Volatility Institute is firmly on board. A couple months ago I was at their most recent annual conference, “A Financial Approach to Climate Risk”, but it somehow fell through the proverbial (blogging) cracks. The program is here, with links to many papers, slides, and videos. Two highlights, among many, were the presentations by Jim Stock (insights on the climate debate gleaned from econometric tools, slides here) and Bob Litterman (an asset-pricing perspective on the social cost of climate change, paper here). A fine initiative!”

From Francis Diebold’s Blog:

“There is little doubt that climate change — tracking, assessment, and hopefully its eventual mitigation — is the burning issue of our times. Perhaps surprisingly, time-series econometric methods have much to offer for weather and climatological modeling (e.g., here), and several econometric groups in the UK, Denmark, and elsewhere have been pushing the agenda forward.

Now the NYU Volatility Institute is firmly on board.

Posted by at 5:32 PM

Labels: Energy & Climate Change, Forecasting Forum

Subscribe to: Posts