Showing posts with label Forecasting Forum. Show all posts

Monday, October 15, 2018

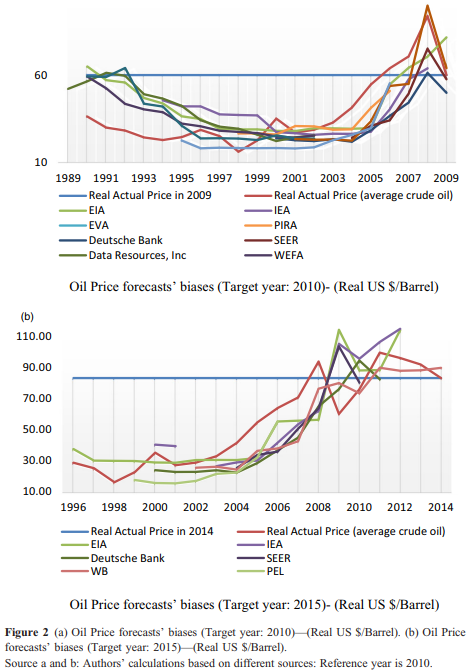

Are published oil price forecasts efficient?

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth. Another behavioural explanation in source of inefficiencies is that forecasters prefer to harmonise their forecasts with other forecasters in order to be not an outlier.”

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth.

Posted by at 10:19 AM

Labels: Forecasting Forum

Thursday, September 27, 2018

What is the yield curve forecasting?

From a new post by David Andolfatto:

“Does the recent flattening of the yield curve portend recession? Not necessarily. The flattening of the real yield curve may simply reflect the fact that real consumption growth is not expected to accelerate or decelerate from the present growth rate of about 1% per annum. On the other hand, a 1% growth rate is substantially lower than the historical average of 2% in the United States. Because of this, the risk that a negative shock (of comparable magnitude to past shocks) sends the economy into technical recession is increased. While the exact date at which the shock arrives is itself is unpredictable, the likelihood of recession is higher relative to a high real interest rate, high growth economy.”

From a new post by David Andolfatto:

“Does the recent flattening of the yield curve portend recession? Not necessarily. The flattening of the real yield curve may simply reflect the fact that real consumption growth is not expected to accelerate or decelerate from the present growth rate of about 1% per annum. On the other hand, a 1% growth rate is substantially lower than the historical average of 2% in the United States.

Posted by at 5:48 PM

Labels: Forecasting Forum

Tuesday, September 4, 2018

RIP Herman Stekler, A Forecasting Giant

Herman Stekler, a giant in the field of forecasting, has passed away. He was known for insisting that “the cost of a recession is so great that a forecaster should never miss one. Some people argue that turning points are unpredictable. I disagree. I have never had trouble predicting recessions. In fact, I have predicted n+x of the last n recessions.”

Herman shuttled between academia and policy institutions throughout his career. His interest was in business and applied economics; in fact, during his graduate school years at MIT he complained to Paul Samuelson about his “frustration and concern that economics was too abstract. There were not enough applications to the real world.” This interest in practical applications led him to spend a summer during his graduate school years at the Rand Corporation helping to devise an early warning radar system to alert the US and Canada in the event of an attack from the USSR. This experience nurtured some of Herman’s interest in leading indicators for economic activity, and it also led to a lasting interest in the defense industry.

For his starting job after graduate school, however, he chose academia over business because he “did not like some of the culture of the business community: During my visit to IBM, I was struck by the fact that every professional had to have his shoes polished before lunch.” He started instead at the University of California, Berkeley, in the business school, in 1959.

In July 1966, he moved to the Fed, starting work in the National Income Section of the Research and Statistics Division. Economic forecasts had just started to be included in the Fed’s so-called ‘Greenbook’ in the fourth quarter of 1965. Herman’s task at the Fed was to help prepare the Greenbook forecasts and sometimes to write an explanation for the rationale behind the forecasts. While the experience was exhilarating, Herman eventually left the Fed as the process of preparing the forecasts – at that time FOMC meetings were held every three weeks – left little time for research (including research on the assessment of the Fed’s forecasts, which Herman spent a lot of time on in the years that followed).

In 1968, Herman joined the faculty at the State University of New York–Stony Brook as a full professor. Reflecting his interest in the defense industry, he later moved to the Industrial College of the Armed Forces (ICAF), where he taught until the early 1990s. As he was planning to retire in 1994, George Washington University tempted him with a research professor position for a year. For every year since then, Herman incorrectly forecast the date of his retirement, which he always said would be “next year.” Nearly, twenty five years later, Herman was still at George Washington, writing papers and advising students to the very end of his days.

Herman published widely in nearly every branch of forecasting, including sports forecasting. A colleague of his once said that Herman “is willing to forecast anything that moves and everything that stands still.”

Herman, my dear friend, it is sad to see you stand still.

**

The Stekler Award for Courage in Forecasting

Herman’s views and his relentless push to get forecasters to predict “early and clearly” led me to institute a Stekler Award for Courage in Forecasting. The recipients of the award thus far are given below:

Groundhog Day Tradition: 2017 Stekler Award for Courage in Forecasting

A Groundhog Day Tradition: The Stekler Award for Courage in Forecasting

The Stekler Award for Courage in Forecasting (Recessions Inaccurately)

Special section in International Journal of Forecasting honoring Herman

In 2012, Herman’s colleagues and friends organized a workshop (Honoring a Forecasting Giant) on the occasion of his 80th birthday, the proceedings of which were published in a special section (On Groundhog Day, Honoring A Forecasting Giant) in the International Journal of Forecasting. The preface to that section describes Herman’s professional work, from which I quote below.

In a famous paper in the American Economic Review (Stekler, 1972), Herman tried to understand why forecasters fail to predict recessions. The evidence that forecasters prefer to miss turning points that occur rather than to predict recessions that do not occur led him to suggest asymmetric loss functions as one possible explanation. (For the record, in October 2007 Herman correctly predicted the onset of the Great Recession and also predicted that the ensuing recovery would be quite weak).

Herman had an abiding interest in improving the ability of economic forecasters to predict turning points. This was the theme of his Ph.D. thesis at MIT. Building on work by his advisor Sidney Alexander, Herman tried to develop a procedure that could be used to forecast turning points in real time. His idea was to predict a turning point if a composite indicator of economic activity was below (above) its previous peak (trough) for a certain number of months. Obviously, a longer lead was more desirable but it also increased the odds of calling a false turning point; Herman’s thesis analyzed the tradeoff between the length of the forecasting lead and the frequency of false signals (Alexander & Stekler, 1959).

In subsequent work, Herman found that forecasters’ record of predicting turning points left a lot to be desired. This was true regardless of the method of forecasting—whether through leading indicators, econometric models or judgmental methods. In the 1960s, he did a consulting project where his ‘”task was to evaluate every econometric model then in existence and determine whether any of them provided accurate forecasts [of turning points]. They did not” (this quote and others in this overview are from an interview with Herman—see Joutz, 2010).

Herman Stekler, a giant in the field of forecasting, has passed away. He was known for insisting that “the cost of a recession is so great that a forecaster should never miss one. Some people argue that turning points are unpredictable. I disagree. I have never had trouble predicting recessions. In fact, I have predicted n+x of the last n recessions.”

Herman shuttled between academia and policy institutions throughout his career.

Posted by at 2:30 PM

Labels: Forecasting Forum

Friday, August 17, 2018

Forecasting Failures and the Need for Automatic Stabilizers

From a new post by Chris Dillow:

“Simon has a good discussion on whether fiscal or monetary policy is better at stabilizing output. I’d suggest, though, that neither is in practice particularly good and that what we need instead are stronger automatic stabilizers.

I say so for a simple reason: recessions are unpredictable. Back in 2000 Prakash Loungani studied the record of private sector consensus forecasts for GDP and concluded that “the record of failure to predict recessions is virtually unblemished” – a fact which remained true thereafter.

The ECB, for example, raised rates in 2007 and 2008, oblivious to the impending disaster. The Bank of England did little better. In February 2008, its “fan chart” attached only a slight probability to GDP failing in year-on-year terms at any time in 2008 or 2009 when in fact it fell 6.1% in the following 12 months. Because of this, it didn’t cut Bank Rate to 0.5% until March 2009.

Given that it takes around two years for changes in interest rates to have its maximum effect upon output, this means that monetary policy does a better job of repairing the economy after a recession than it does of preventing recession in the first place. And of course, as there’s no evidence that governments can predict recessions any better than the private sector or central banks, the same is true for fiscal policy.

All this suggests to me that if we want to stabilize in the face of unpredictable recessions, we need not just discretionary monetary or fiscal policy but rather better automatic stabilizers.”

From a new post by Chris Dillow:

“Simon has a good discussion on whether fiscal or monetary policy is better at stabilizing output. I’d suggest, though, that neither is in practice particularly good and that what we need instead are stronger automatic stabilizers.

I say so for a simple reason: recessions are unpredictable. Back in 2000 Prakash Loungani studied the record of private sector consensus forecasts for GDP and concluded that “the record of failure to predict recessions is virtually unblemished”

Posted by at 10:10 AM

Labels: Forecasting Forum

Saturday, August 4, 2018

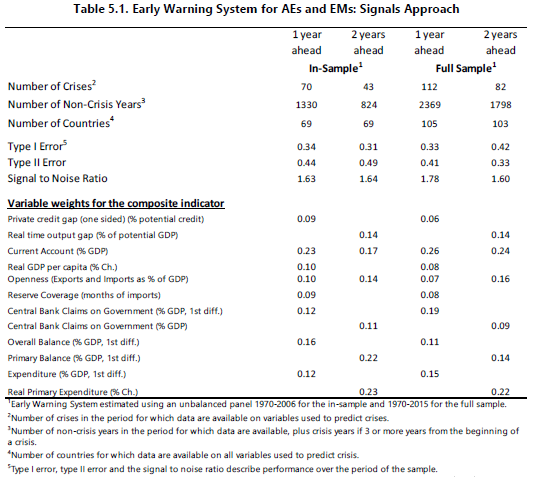

Predicting Fiscal Crises

A new IMF working paper finds that “both nonfiscal (external and internal imbalances) and fiscal variables help predict crises among advanced and emerging economies.”

“Our analysis identifies robust indicators of vulnerabilities that can help signal a high probability of the onset of a crisis in the near future. Building early warning indicators that help predict future fiscal crises is inherently difficult, including because countries may take mitigating action as they see the growing vulnerabilities. However, we find that some types of vulnerabilities are consistently relevant to explain fiscal crises. This raises the question why governments do not act as they see signals. In large measure they do, as crises among advanced economies are rare. Still, the occurrence of crises may reflect overly optimistic projections about the future (e.g., economic growth, cost of debt), and as such governments underestimate the risks and fail to take mitigating measures. Another possibility could be that other shocks or crisis (e.g., banking) could lead to fiscal pressures”

A new IMF working paper finds that “both nonfiscal (external and internal imbalances) and fiscal variables help predict crises among advanced and emerging economies.”

“Our analysis identifies robust indicators of vulnerabilities that can help signal a high probability of the onset of a crisis in the near future. Building early warning indicators that help predict future fiscal crises is inherently difficult, including because countries may take mitigating action as they see the growing vulnerabilities.

Posted by at 5:35 PM

Labels: Forecasting Forum

Subscribe to: Posts