SOME INVESTORS worry that America will face a recession in the next few years, after one of the longest expansions on record. Stock indices have fallen by 10% since early October. Yields on short-term government bonds exceed those of some longer-dated ones, often a harbinger of a downturn. Despite this, economic forecasters project GDP growth of about 2% in 2020.

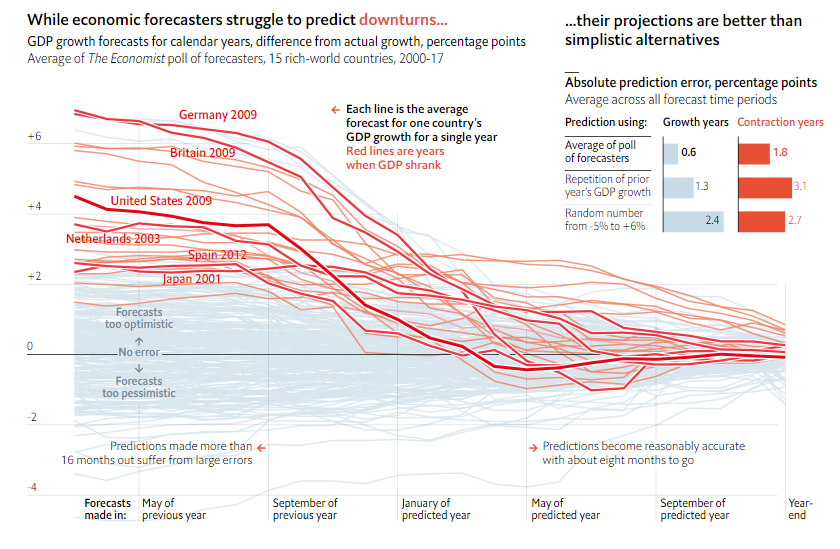

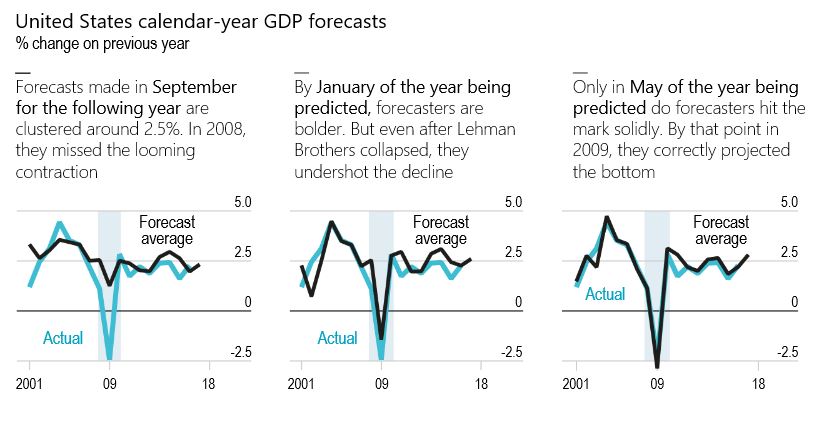

How much confidence should one have in these predictions? For the past 20 years The Economist has kept a database of projections by banks and consultancies for annual GDP growth. It now contains 100,000 forecasts across 15 rich countries. In general, they fared well over brief time periods, but got worse the further analysts peered into the future—a trend unsurprising in direction but humbling in magnitude. If a recession lurks beyond 2019, economists are unlikely to foresee it this far in advance.

Economies are fiendishly complex, but forecasters usually predict short-term trajectories with reasonable accuracy. Projections made in early September for the year ending four months later missed the actual figure by an average of just 0.4 percentage points. Errors rose to 0.8 points when predicting one year out. But over longer horizons forecasts performed far worse. With 22 months of lead time, they misfired by 1.3 points on average—no better than repeating the previous year’s growth rate.

The biggest errors occurred ahead of GDP contractions. The average projection 22 months before the end of a downturn year missed by 3.7 points, four times more than in other years. In part, this is because growth figures are “skewed”: economies usually expand slowly and steadily, but sometimes contract sharply. As a result, forecasters seeking to predict the most likely outcome expect growth. However, they adjust too slowly even once bad news arrives, says Prakash Loungani of the IMF. That suggests they are prone to “anchoring”—over-weighting previous expectations—or to “herding” (keeping their predictions near the consensus).”

Read the full article here.