Showing posts with label Forecasting Forum. Show all posts

Tuesday, April 9, 2019

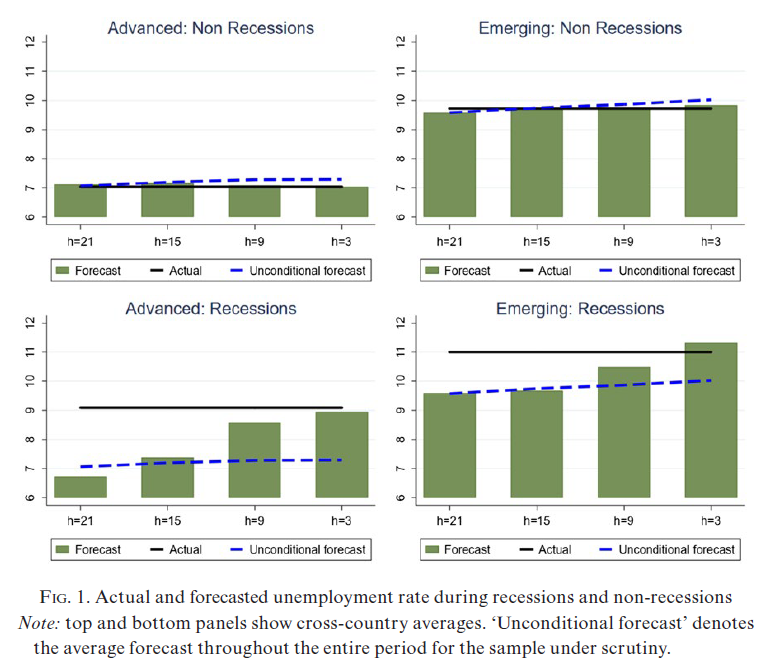

An Assessment of the IMF’s Unemployment Forecasts

My new paper with Zidong An and Joao Jalles was just published in Manchester School:

“This paper assesses the performance of the IMF’s unemployment forecasts for 84 countries, both advanced and emerging market economies, between 1990 and 2015. The forecasts are reported in the World Economic Outlook, a leading IMF publication. The forecasts display a small amount of bias—they tend to predict lower unemployment outcomes than occur—which arises because the forecasters fail to predict accurately the sharp increase in unemployment during downturns. Forecasts are characterized by inefficiency (errors of the past are repeated in the present) and rigidity (forecast revisions are serially correlated). There is little to choose between IMF and Consensus Forecasts, a source of private sector forecasts, for the small subset of 12 countries for which both sets of forecasts are available.”

My new paper with Zidong An and Joao Jalles was just published in Manchester School:

“This paper assesses the performance of the IMF’s unemployment forecasts for 84 countries, both advanced and emerging market economies, between 1990 and 2015. The forecasts are reported in the World Economic Outlook, a leading IMF publication. The forecasts display a small amount of bias—they tend to predict lower unemployment outcomes than occur—which arises because the forecasters fail to predict accurately the sharp increase in unemployment during downturns.

Posted by at 10:45 PM

Labels: Forecasting Forum

Subjective Models of the Macroeconomy: Evidence From Experts and a Representative Sample

From a new working paper:

“We propose a method to measure people’s subjective models of the macroeconomy. Using a representative sample of the US population and a sample of experts we study how expectations about the unemployment rate and the inflation rate change in response to four different hypothetical exogenous shocks: a monetary policy shock, a government spending shock, a tax shock, and an oil price shock. While expert predictions are mostly quantitatively aligned with standard dynamic stochastic general equilibrium models and vector auto-regression evidence, there is strong heterogeneity in the predictions in the representative panel. While households predict changes in unemployment that are qualitatively in line with the experts for all four shocks, their predictions of changes in inflation are at odds with those of experts both for the tax shock and the interest rate shock. People’s beliefs about the micro mechanisms through which the different macroeconomic shocks are propagated in the economy strongly affect how aligned their predictions are with those of the experts. More educated and older respondents form their expectations more in line with experts, consistent with roles for cognitive limitations and learning over the life-cycle. Our findings inform the validity of central assumptions about the expectation formation process and have important implications for the optimal design of fiscal and monetary policy.”

From a new working paper:

“We propose a method to measure people’s subjective models of the macroeconomy. Using a representative sample of the US population and a sample of experts we study how expectations about the unemployment rate and the inflation rate change in response to four different hypothetical exogenous shocks: a monetary policy shock, a government spending shock, a tax shock, and an oil price shock. While expert predictions are mostly quantitatively aligned with standard dynamic stochastic general equilibrium models and vector auto-regression evidence,

Posted by at 10:33 PM

Labels: Forecasting Forum

Thursday, March 28, 2019

News-driven inflation expectations and information rigidities

From a new working paper:

“In most democracies the fourth estate, i.e., the news media, plays an important role in society. The media not only has the capacity of advocacy and implicit ability to frame political and economic issues, but it is also the primary source from which most people get information. In macroeconomics, expectations are center stage. But, expectations are shaped by information, and information does not travel unaffected through the ether. Rather, it is digested, filtered, and colored by the media. Surprisingly, however, the potential independent role of the media in the expectation formation process has received relatively little attention in macroeconomics, both in theory and in applied work.

In this paper we build on a growing literature providing evidence for a departure from the full information rational expectation (FIRE) assumption towards a theory of information rigidities (Coibion and Gorodnichenko (2012), Dovern et al. (2015), Coibion and Gorodnichenko (2015a), Armantier et al. (2016)), and investigate the potential role played by the media for households’ inflation expectations in this setting.”

From a new working paper:

“In most democracies the fourth estate, i.e., the news media, plays an important role in society. The media not only has the capacity of advocacy and implicit ability to frame political and economic issues, but it is also the primary source from which most people get information. In macroeconomics, expectations are center stage. But, expectations are shaped by information, and information does not travel unaffected through the ether.

Posted by at 4:38 PM

Labels: Forecasting Forum

Tuesday, March 12, 2019

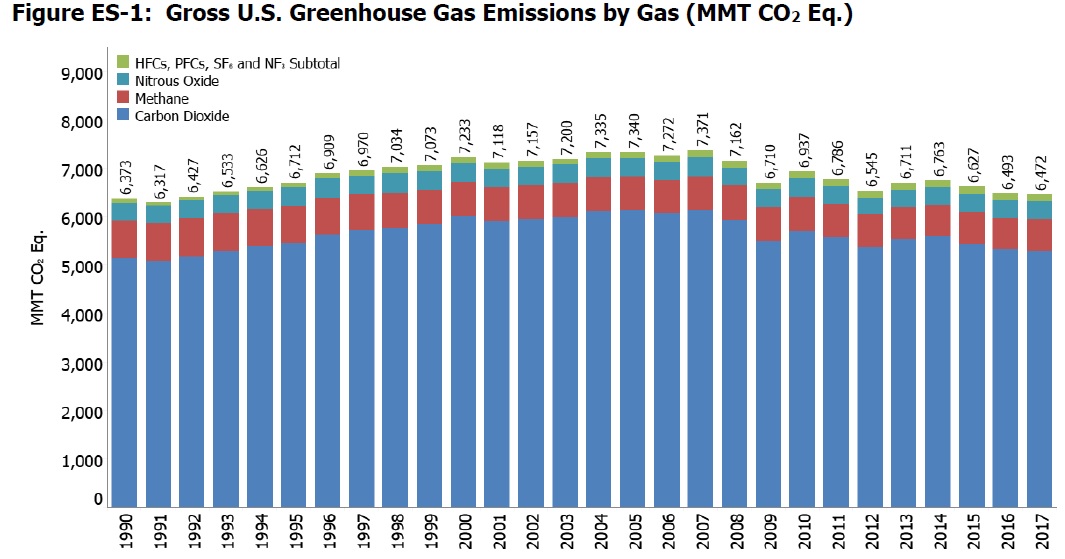

Sources of US Greenhouse Gas Emissions

From a new post by Timothy Taylor:

“Each year the Environmental Protection Agency produces an Inventory of U.S. Greenhouse Gas Emissions and Sinks. The draft version of the report for 1990-2017 was published in February 2019.

Here’s a figure showing gross emissions of greenhouse gases in the US. Emissions that are not carbon dioxide have been converted to its “equivalent.”

Several themes jump out from the figure. One is that the overwhelming share of emissions are plain old carbon dioxide, rather than methane or other gases. Another is that the total emissions have been dropping in the last few years, and are more-or-less back to 1990 levels, which one can interpret either through the lens of “could be worse” or “should be better,” as you are so inclined.

Given the predominance of carbon dioxide emissions, let’s dig into those a little deeper. Most of the carbon dioxide emissions come from burning fossil fuels. This table shows the breakdown into a few main sectors.

Total US emissions of greenhouse gases in 2017 were 6472 million metric tons of carbon dioxide-equivalent. Thus, transportation and the electric power sector combined account for more than half of all emissions. It seems to me both appropriate to focus on reducing emissions in those sectors, but also to remember that, combined, they are only about half of the problem. Emissions from industrial, residential, and commercial activities are also pretty significant.

Moreover, methane emissions landfill, leakages in natural gas systems, and the digestive tracts of livestock make up the equivalent of 449 million metric tons of carbon dioxide emissions in 2017. Agricultural soil management released nitrogen oxides that are the equivalent of 266 million metric tons of carbon dioxide in 2017, roughly equivalent to fossil fuel-related carbon emissions from the residential or the commercial sector. Hydrofluorocarbons that are being used to to replace ozone-depleting substances account for another 152 million metric tons of CO2-equivalent emissions.

This EPA report is a tabulation of greenhouse gas emissions. It isn’t about questions of how emissions of greenhouse gases might affect climate, or estimating economics costs from changes in climate, or about what methods of addressing greenhouse gas emissions are likely to be more or less cost-effective. For discussions of these points, I recommend a three-paper “Symposium on Climate Change” in the Fall 2018 issue of the Journal of Economic Perspectives. (Full disclosure: My actual paid job, as opposed to my blogging avocation, is Managing Editor of the JEP.) The papers are:

- “An Economist’s Guide to Climate Change Science,” by Solomon Hsiang and Robert E.Kopp

- “Quantifying Economic Damages from Climate Change.” by Maximilian Auffhammer

- “The Cost of Reducing Greenhouse Gas Emissions,” by Kenneth Gillingham and James H.Stock”

From a new post by Timothy Taylor:

“Each year the Environmental Protection Agency produces an Inventory of U.S. Greenhouse Gas Emissions and Sinks. The draft version of the report for 1990-2017 was published in February 2019.

Here’s a figure showing gross emissions of greenhouse gases in the US. Emissions that are not carbon dioxide have been converted to its “equivalent.”

Several themes jump out from the figure.

Posted by at 6:43 PM

Labels: Forecasting Forum

Tuesday, February 19, 2019

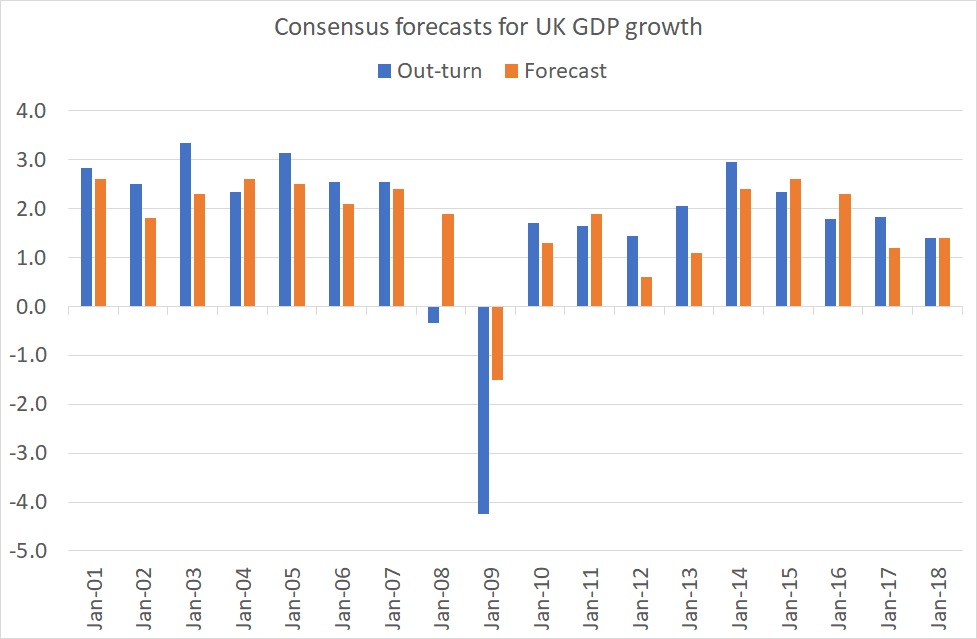

The forecasting record

From a new post:

“The ONS says GDP grew by 1.4% last year. 1.4% is a significant number: it is exactly what the private sector economists surveyed by the Treasury predicted in December 2017 that growth would be in 2018.

Granted, this bulls-eye might not survive future revisions to GDP estimates. But it reminds us that economists’ forecasts for growth are often not too bad.

My chart shows the point. It compares forecasts made in December for growth the following year to actual growth since 2001. Most of the time, the forecasts aren’t too far out. Where they go badly wrong is in recessions. Economists don’t see these coming. In December 2007 they forecast that GDP would grow 1.9 per cent in 2008. In fact it shrank. And even in December 2008 – after the banking crisis – they grossly under-predicted the depth of the recession.

This fitted the pattern. Back in 2000 Prakash Loungani wrote:

The record of failure to predict recessions is virtually unblemished. Only two of the 60 recessions that occurred around the world during the 1990s were predicted a year in advance. That may seem like a tough standard to impose on forecast accuracy. Maybe so—but two-thirds of those recessions remained un-detected seven months before they occurred.

In December 1990, for example, UK economists forecast growth of 0.3% in 1991. In fact, we got a 1% drop.

Economic forecasts, then, are reasonably OK except when we really need them.

Why? One possibility, suggested by Loungani, is that economists are slow to update their forecasts in light of news. One bit of evidence for this is that they also under-predicted the boom of 1988 (probably because they over-estimated the adverse effect of the 1987 stock market crash). Another possibility is that mainstream forecasters lack incentives to break with the consensus and predict recessions: it’s better to be wrong in a crowd. It’s for this reason that it is mavericks and those wanting to make a name for themselves who predict doom.

I suspect, though, that there’s something else. It’s that recessions are caused by things which are hard for macroeconomists to discern. For example, Xavier Gabaix shows how they can be caused by failures at large firms. And Daron Acemoglu and colleagues have described how they can be amplified by network effects: trouble at a firm at the centre of a hub can spill over into other firms whereas trouble at a spoke does not. These are both part of the story of the 2008-09 crisis.

Macroeconomists are tolerably good at predicting fluctuations in aggregate demand. It is other things – such as supply shocks, network and peer effects or banking crises – they’re not so good at foreseeing.

It doesn’t automatically follow, however, that recessions are wholly unpredictable. US evidence strongly suggests that inverted yield curves lead (with a variable lag) to economic downturns. I suspect this is for the same reason that consumption-wealth ratios help predict bad times. It’s because such data aggregates the dispersed and fragmentary knowledge of countless individuals. There some specific conditions when the wisdom of crowds works better than experts.”

From a new post:

“The ONS says GDP grew by 1.4% last year. 1.4% is a significant number: it is exactly what the private sector economists surveyed by the Treasury predicted in December 2017 that growth would be in 2018.

Granted, this bulls-eye might not survive future revisions to GDP estimates. But it reminds us that economists’ forecasts for growth are often not too bad.

My chart shows the point.

Posted by at 10:51 AM

Labels: Forecasting Forum

Subscribe to: Posts