Showing posts with label Forecasting Forum. Show all posts

Wednesday, August 21, 2019

Attempting to Avoid a Recession: Fortune or Folly?

An intriguing analysis by the SEI Knowledge Center on forecasting recessions:

“To explore this possibility, we looked at the last 13 recessions in the US dating back to 1937. US data was used due to availability of a longer history; we believe the core conclusions of the analysis should be the same for any geography or market. We considered a range of sell-and-buy scenarios surrounding the official start and end dates of each recession, as determined by the National Bureau of Economic Research (or NBER, a private, non-profit, non-partisan organisation). The timing of our hypothetical decisions to sell out of the market and buy back into the market varied by up to eight quarters before and after each actual recession start and end date. This gave us a grand total of 2,577 scenarios to consider, as highlighted in Exhibit 1.”

Exhibit 1: Endless Possibilities

Source: Bloomberg, SEI

An intriguing analysis by the SEI Knowledge Center on forecasting recessions:

“To explore this possibility, we looked at the last 13 recessions in the US dating back to 1937. US data was used due to availability of a longer history; we believe the core conclusions of the analysis should be the same for any geography or market. We considered a range of sell-and-buy scenarios surrounding the official start and end dates of each recession,

Posted by at 12:29 PM

Labels: Forecasting Forum

Friday, July 19, 2019

Recession Forecasts Are So Bad, They’re Good

From Bloomberg:

“Economists, notoriously terrible at predicting downturns, may be inadvertently providing a useful service.

It’s no secret that economists are terrible at predicting recessions: a host of studies, along with a raft of anecdotal evidence, reveals a track record that is astonishingly bad. This has prompted a growing number of market watchers to conclude that forecasting recessions is a fool’s game.

But there’s another way to look at this dismal record. What if economists are so bad at predicting recessions that they’re actually good? What if a profession that consistently, almost universally, gets something wrong is inadvertently getting something right?

Prakash Loungani and his colleagues at the International Monetary Fund conducted the most sophisticated studies of economic forecasting, assessing the accuracy of economists in 63 countries between the years of 1992 and 2014. The results, as my colleagues at Bloomberg have noted (see here and here) are mind-blowingly awful. In fact, every single country displayed the exact same bad track record of predicting recessions. Moreover, as Loungani and his co-authors noted, “the forecasts of the private sector and public sector are virtually identical; thus, both are equally good at missing recessions.”

Good at missing recessions. Think about that for a moment. Economic forecasts consistently miss the onset of recessions.

This means that their failure to predict is a problem altogether different from the failures emphasized by the random-walk hypothesis and other critiques of prognostication. Economists predict the future incorrectly, but their failures are, well, predictable. Does that mean they may be telling us something important after all?

To understand the implications of this question, consider the typical progression of erroneous forecasts over the course of a recession’s first year. Loungani found that forecasts made on the eve of a recession (when almost no one imagines there’s trouble brewing) are more or less in line with the previous year’s predictions.”

Continue reading here.

From Bloomberg:

“Economists, notoriously terrible at predicting downturns, may be inadvertently providing a useful service.

It’s no secret that economists are terrible at predicting recessions: a host of studies, along with a raft of anecdotal evidence, reveals a track record that is astonishingly bad. This has prompted a growing number of market watchers to conclude that forecasting recessions is a fool’s game.

But there’s another way to look at this dismal record.

Posted by at 11:20 AM

Labels: Forecasting Forum

Friday, May 3, 2019

The next US recession is likely to be around the corner

From a VOX article:

“Business economists argue that the length of an expansion is a good indicator of when a recession will hit. Using both parametric and non-parametric measures, this column finds strong support for the theory from post-WWII data on the US economy. The findings suggest there is good reason to expect a US recession in the next two years.”

“[…] we estimate in Beaudry and Portier (2019) the probability of the US economy entering a recession in the following year (or following two years), conditional on the expansion having lasted q quarters. This can be done in a parametric way based on the Weibull distribution, or non-parametrically using Kaplan and Meier’s estimator of the survival function. Regardless of the method, and using post-WW2 US data, there is consistent evidence of age-dependence, as shown in Figure 1. For an expansion that has lasted only five quarters, the probability of entering a recession in the next year is around 10%, while this increases to 30-40% if the expansion has lasted over 35 quarters. Similarly, if looking at a two years window, we find the probability of entering a recession in the next two years raises from 25-30% to around 50-80% as the expansion extends from five quarters to 32 quarters (the exact probability depends on whether we use a parametric or a non-parametric approach). ”

From a VOX article:

“Business economists argue that the length of an expansion is a good indicator of when a recession will hit. Using both parametric and non-parametric measures, this column finds strong support for the theory from post-WWII data on the US economy. The findings suggest there is good reason to expect a US recession in the next two years.”

“[…] we estimate in Beaudry and Portier (2019) the probability of the US economy entering a recession in the following year (or following two years),

Posted by at 9:41 AM

Labels: Forecasting Forum

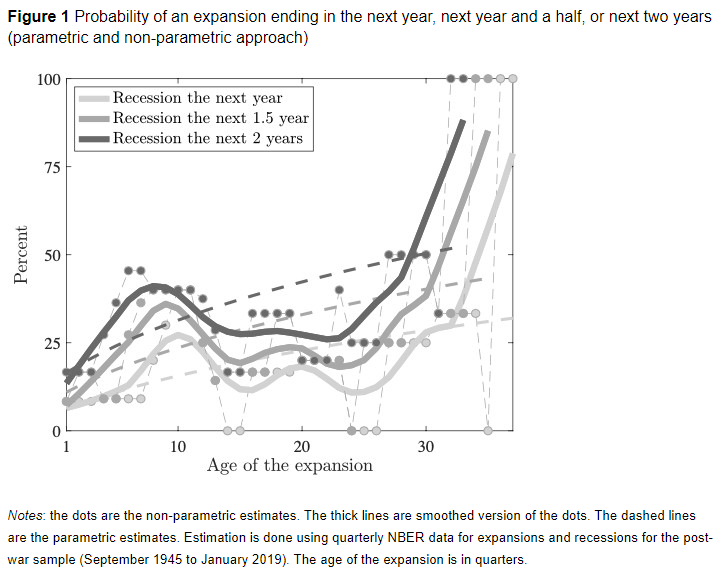

The next US recession is likely to be around the corner

From a VoxEU post by Franck Portier:

“Business economists argue that the length of an expansion is a good indicator of when a recession will hit. Using both parametric and non-parametric measures, this column finds strong support for the theory from post-WWII data on the US economy. The findings suggest there is good reason to expect a US recession in the next two years.

This summer, the current US expansion, which started in June 2009, is likely to break the historical post-WWII record of 120 months long, which is currently held by the March 1991-March 2001 expansion. It is already longer than the post-WWII average of 58 months. Should we be worried? Is the next recession around the corner?

Yes, according to business economists. For example, according to the semi-annual National Association for Business Economics survey released last February, three-quarters of the panellists expect an economic recession by the end of 2021. While only 10% of panellists expect a recession in 2019, 42% say a recession will happen in 2020, and 25% expect one in 2021.

No, according to the conventional wisdom among more academic-oriented economists, who believe that “expansions, like Peter Pan, endure but never seem to grow old”, as Rudebusch (2016) recently argued. As he wrote, “based only on age, an 80-month-old expansion has effectively the same chance of ending as a 40-month-old expansion”. This view was also forcefully expressed last December by the (now ex-) Federal Reserve Board Chair Janet Yellen, who said “… I think it’s a myth that expansions die of old age. I do not think they die of old age. So the fact that this has been quite a long expansion doesn’t lead me to believe that … its days are numbered”.

My research with Paul Beaudry and Dana Galizia tends to favour the former view, that we should be worried about a recession hitting the US economy in the next 18 months.

There are two reasons why we reach this conclusion. The first relies on a statistical analysis that uses only the age of an expansion to predict the probability of a recession. The second digs deeper into the very functioning of market economies.

First, we estimate in Beaudry and Portier (2019) the probability of the US economy entering a recession in the following year (or following two years), conditional on the expansion having lasted q quarters. This can be done in a parametric way based on the Weibull distribution, or non-parametrically using Kaplan and Meier’s estimator of the survival function. Regardless of the method, and using post-WW2 US data, there is consistent evidence of age-dependence, as shown in Figure 1. For an expansion that has lasted only five quarters, the probability of entering a recession in the next year is around 10%, while this increases to 30-40% if the expansion has lasted over 35 quarters. Similarly, if looking at a two years window, we find the probability of entering a recession in the next two years raises from 25-30% to around 50-80% as the expansion extends from five quarters to 32 quarters (the exact probability depends on whether we use a parametric or a non-parametric approach).”

Continue reading here.

From a VoxEU post by Franck Portier:

“Business economists argue that the length of an expansion is a good indicator of when a recession will hit. Using both parametric and non-parametric measures, this column finds strong support for the theory from post-WWII data on the US economy. The findings suggest there is good reason to expect a US recession in the next two years.

This summer, the current US expansion,

Posted by at 9:23 AM

Labels: Forecasting Forum

Thursday, April 25, 2019

18 spectacularly wrong predictions made around the time of first Earth Day in 1970, expect more this year

From a new AEI post by Mark J. Perry:

“Here are 18 examples of the spectacularly wrong predictions made around 1970 when the “green holy day” (aka Earth Day) started:

1. Harvard biologist George Wald estimated that “civilization will end within 15 or 30 years unless immediate action is taken against problems facing mankind.”

2. “We are in an environmental crisis which threatens the survival of this nation, and of the world as a suitable place of human habitation,” wrote Washington University biologist Barry Commoner in the Earth Day issue of the scholarly journal Environment.

3. The day after the first Earth Day, the New York Times editorial page warned, “Man must stop pollution and conserve his resources, not merely to enhance existence but to save the race from intolerable deterioration and possible extinction.”

4. “Population will inevitably and completely outstrip whatever small increases in food supplies we make,” Paul Ehrlich confidently declared in the April 1970 issue of Mademoiselle. “The death rate will increase until at least 100-200 million people per year will be starving to death during the next ten years.”

5. “Most of the people who are going to die in the greatest cataclysm in the history of man have already been born,” wrote Paul Ehrlich in a 1969 essay titled “Eco-Catastrophe! “By…[1975] some experts feel that food shortages will have escalated the present level of world hunger and starvation into famines of unbelievable proportions. Other experts, more optimistic, think the ultimate food-population collision will not occur until the decade of the 1980s.”

6. Ehrlich sketched out his most alarmist scenario for the 1970 Earth Day issue of The Progressive, assuring readers that between 1980 and 1989, some 4 billion people, including 65 million Americans, would perish in the “Great Die-Off.”

7. “It is already too late to avoid mass starvation,” declared Denis Hayes, the chief organizer for Earth Day, in the Spring 1970 issue of The Living Wilderness.

8. Peter Gunter, a North Texas State University professor, wrote in 1970, “Demographers agree almost unanimously on the following grim timetable: by 1975 widespread famines will begin in India; these will spread by 1990 to include all of India, Pakistan, China and the Near East, Africa. By the year 2000, or conceivably sooner, South and Central America will exist under famine conditions….By the year 2000, thirty years from now, the entire world, with the exception of Western Europe, North America, and Australia, will be in famine.”

9. In January 1970, Life reported, “Scientists have solid experimental and theoretical evidence to support…the following predictions: In a decade, urban dwellers will have to wear gas masks to survive air pollution…by 1985 air pollution will have reduced the amount of sunlight reaching earth by one half….”

10. Ecologist Kenneth Watt told Time that, “At the present rate of nitrogen buildup, it’s only a matter of time before light will be filtered out of the atmosphere and none of our land will be usable.”

11. Barry Commoner predicted that decaying organic pollutants would use up all of the oxygen in America’s rivers, causing freshwater fish to suffocate.

12. Paul Ehrlich chimed in, predicting in 1970 that “air pollution…is certainly going to take hundreds of thousands of lives in the next few years alone.” Ehrlich sketched a scenario in which 200,000 Americans would die in 1973 during “smog disasters” in New York and Los Angeles.

13. Paul Ehrlich warned in the May 1970 issue of Audubon that DDT and other chlorinated hydrocarbons “may have substantially reduced the life expectancy of people born since 1945.” Ehrlich warned that Americans born since 1946…now had a life expectancy of only 49 years, and he predicted that if current patterns continued this expectancy would reach 42 years by 1980, when it might level out. (Note: According to the most recent CDC report, life expectancy in the US is 78.8 years).

14. Ecologist Kenneth Watt declared, “By the year 2000, if present trends continue, we will be using up crude oil at such a rate…that there won’t be any more crude oil. You’ll drive up to the pump and say, `Fill ‘er up, buddy,’ and he’ll say, `I am very sorry, there isn’t any.’”

15. Harrison Brown, a scientist at the National Academy of Sciences, published a chart in Scientific American that looked at metal reserves and estimated the humanity would totally run out of copper shortly after 2000. Lead, zinc, tin, gold, and silver would be gone before 1990.

16. Sen. Gaylord Nelson wrote in Look that, “Dr. S. Dillon Ripley, secretary of the Smithsonian Institute, believes that in 25 years, somewhere between 75 and 80 percent of all the species of living animals will be extinct.”

17. In 1975, Paul Ehrlich predicted that “since more than nine-tenths of the original tropical rainforests will be removed in most areas within the next 30 years or so, it is expected that half of the organisms in these areas will vanish with it.”

18. Kenneth Watt warned about a pending Ice Age in a speech. “The world has been chilling sharply for about twenty years,” he declared. “If present trends continue, the world will be about four degrees colder for the global mean temperature in 1990, but eleven degrees colder in the year 2000. This is about twice what it would take to put us into an ice age.””

From a new AEI post by Mark J. Perry:

“Here are 18 examples of the spectacularly wrong predictions made around 1970 when the “green holy day” (aka Earth Day) started:

1. Harvard biologist George Wald estimated that “civilization will end within 15 or 30 years unless immediate action is taken against problems facing mankind.”

2. “We are in an environmental crisis which threatens the survival of this nation,

Posted by at 10:41 AM

Labels: Forecasting Forum

Subscribe to: Posts