Showing posts with label Energy & Climate Change. Show all posts

Wednesday, July 6, 2016

Norway: The Transition from Oil and Gas

By IMF colleague: Giang Ho

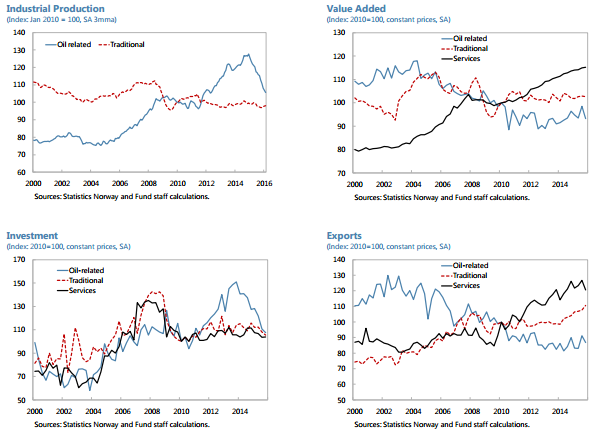

“As offshore investment drops from its peak and oil prices retreat from their high in 2014, the Norwegian economy is going through a transition away from oil dependence,” according to an IMF report. “The transition from oil and gas is a gradual process, and more time would be required before a credible assessment can be made of its progress. The preliminary data show an ongoing marked decline in oil-related production and investment, whereas activity in the traditional goods sector is holding up but not sufficiently to pick up the slack. The divergent performance is perhaps most pronounced within manufacturing between oil-related industries (i.e. machinery and equipment, ships, boats and oil platforms) and nonoil industries. Overall, although the real value added share of the oil-related sector has shrunk from over 36 percent on average during 2000–13 to about 29 percent during 2014–15, much of this appears to have been picked up by the business services sector. The traditional goods producing sector remains a relatively small part of the economy, with value added share at a little over 7 percent and hours worked share declining to 11 percent.”

By IMF colleague: Giang Ho

“As offshore investment drops from its peak and oil prices retreat from their high in 2014, the Norwegian economy is going through a transition away from oil dependence,” according to an IMF report. “The transition from oil and gas is a gradual process, and more time would be required before a credible assessment can be made of its progress. The preliminary data show an ongoing marked decline in oil-related production and investment,

Posted by at 9:02 AM

Labels: Energy & Climate Change

Thursday, March 24, 2016

Oil Prices and the Global Economy: It’s Complicated

Oil prices have been persistently low for well over a year and a half now, but as the April 2016 World Economic Outlook will document, the widely anticipated “shot in the arm” for the global economy has yet to materialize. We argue that, paradoxically, global benefits from low prices will likely appear only after prices have recovered somewhat, and advanced economies have made more progress surmounting the current low interest rate environment.

Since June 2014 oil prices have dropped about 65 percent in U.S. dollar terms (about $70) as growth has progressively slowed across a broad range of countries. Even taking into account the 20 percent dollar appreciation during this period (in nominal effective terms), the decline in oil prices in local currency has been on average over $60. This outcome has puzzled many observers including us at the Fund, who had believed that oil-price declines would be a net plus for the world economy, obviously hurting exporters but delivering more-than-offsetting gains to importers. The key assumption behind that belief is a specific difference in saving behavior between oil importers and oil exporters: consumers in oil importing regions such as Europe have a higher marginal propensity to consume out of income than those in exporters such as Saudi Arabia.

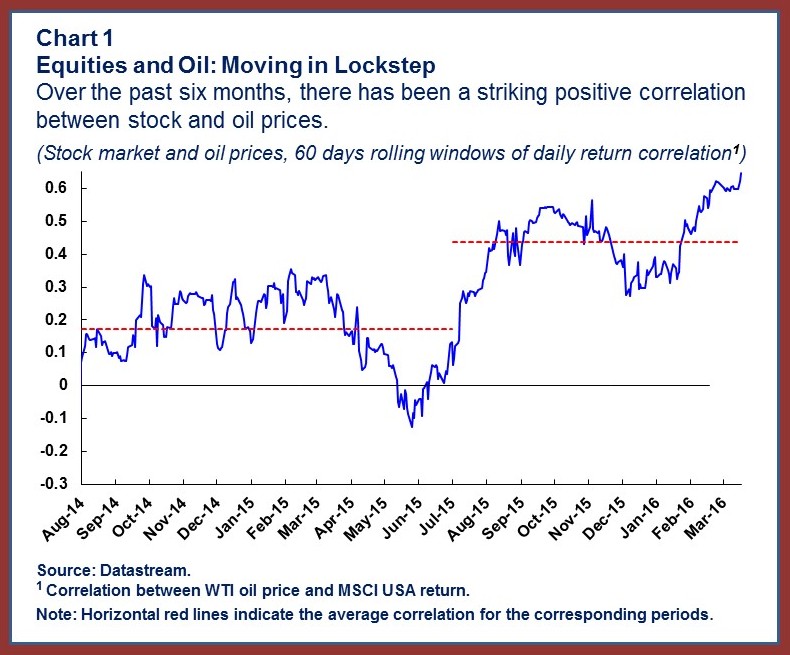

World equity markets have clearly not subscribed to this theory. Over the past six months or more, equity markets have tended to fall when oil prices fall—not what we would expect if lower oil prices help the world economy on balance. Indeed, since August 2015 the simple correlation between equity and oil prices has not only been positive (Chart 1), it has doubled in comparison to an earlier period starting in August 2014 (though not to an unprecedented level).

Past episodes of sharp changes in oil prices have tended to have visible countercyclical effects—for example, slower world growth after big increases. Is this time different? Several factors affect the relation between oil prices and growth, but we will argue that a big difference from previous episodes is that many advanced economies have nominal interest rates at or near zero.

Supply versus demand

One obvious problem in predicting the effects of oil-price movements is that a fall in the world price can result either from an increase in global supply or a decrease in global demand. But in the latter case, we would expect to see exactly the same pattern as in recent quarters—falling prices accompanied by slowing global growth, with lower oil prices cushioning, but likely not reversing, the growth slowdown.

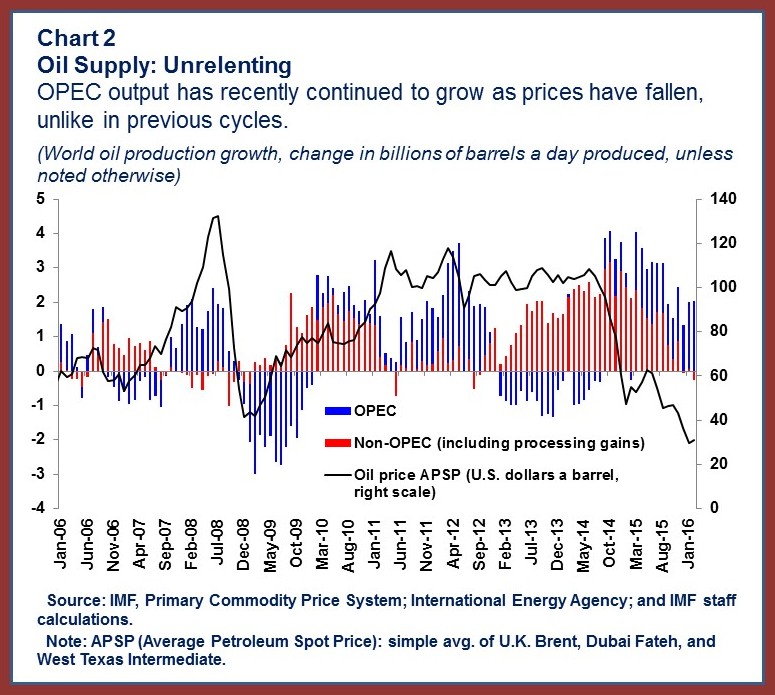

Slowing demand is no doubt part of the story, but the evidence suggests that increased supply is at least as important. More generally, oil supply has been strong owing to record high output from members of the Organization of the Petroleum Exporting Countries (OPEC) including, now, exports from Iran, as well as from some non-OPEC countries. In addition, the U.S. supply of shale oil initially proved surprisingly resilient in the face of lower prices. Chart 2 shows how OPEC output has recently continued to grow as prices have fallen, unlike in some previous cycles.

Continue reading here.

Below is an iMFdirect post by Maurice Obstfeld, Gian Maria Milesi-Ferretti, and Rabah Arezki:

Oil prices have been persistently low for well over a year and a half now, but as the April 2016 World Economic Outlook will document, the widely anticipated “shot in the arm” for the global economy has yet to materialize. We argue that, paradoxically, global benefits from low prices will likely appear only after prices have recovered somewhat,

Posted by at 12:07 PM

Labels: Energy & Climate Change

Sunday, November 29, 2015

Sovereign wealth funds in the new era of oil

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. This column goes through the evidence, suggesting that the low price environment is likely to test the relationship between governments in oil-exporting countries and their sovereign wealth funds, at a time when spending is going up.

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. The growth in the assets of their sovereign wealth funds, which were rising at a rapid rate until recently, is now slowing – and some have started drawing on their buffers.

Figure 1. Brent crude price, 2014-2015 (US dollars per barrel)

In the short run, this phenomenon is not cause for alarm. Most oil exporters have enough buffers to withstand a temporary drop in oil prices. But what will happen if low oil prices persist, and how will policymakers react? We explore here the fallout from low oil prices on sovereign wealth funds in oil-exporting countries and find that that they have important domestic implications. The impact on global asset prices will depend on the extent of unwinding of the sovereign wealth funds of oil exporters that will not be compensated by portfolio adjustment in other parts of the world that will in turn depend on their economic prospects.

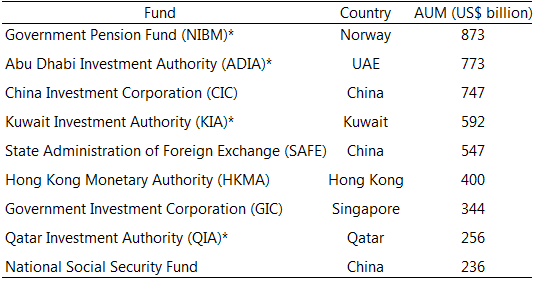

Figure 2. World’s biggest sovereign wealth funds, 2015 estimates

The rise of sovereign wealth funds

In the early 2000s, high oil prices brought about a massive redistribution of income to oil exporters, resulting in current account surpluses and a rapid buildup of foreign assets. Governments established new sovereign wealth funds or increased the size of existing ones to help manage the larger pool of financial assets. The total assets of sovereign wealth funds are concentrated in a few countries. As of March 2015, it is estimated at $7.3 trillion, of which $4.2 trillion are oil and gas related. While there are large differences across sovereign wealth funds, available information on their asset allocation points to a significant share in equities and bonds.

From Vox by Rabah Arezki, Adnan Mazarei, and Ananthakrishnan Prasad

As a result of the oil price plunge, the major oil-exporting countries are facing budget deficits for the first time in years. This column goes through the evidence, suggesting that the low price environment is likely to test the relationship between governments in oil-exporting countries and their sovereign wealth funds, at a time when spending is going up.

As a result of the oil price plunge,

Posted by at 11:49 AM

Labels: Energy & Climate Change

Monday, September 14, 2015

Metals and Oil: A Tale of Two Commodities

“It was the best of times, it was the worst of times.” With these words Charles Dickens opens his novel “A Tale of Two Cities”. Winners and losers in a “tale of two commodities” may one day look back with similar reflections, as prices of metals and oil have seen some seismic shifts in recent weeks, months and years.

This blog seeks to explain how demand — but also supply and financial market conditions — are affecting metals prices. We will show some contrast with oil, where supply is the major factor. Stay tuned for a deeper analysis of the trends in a special commodities feature, which will be included in next month’s World Economic Outlook.

Metals matter

Base metals — such as iron ore, copper, aluminum and nickel — are the lifeblood of global industrial production and construction. Shaped by shifts in supply and demand, they are a valuable weathervane of change in the world economy.

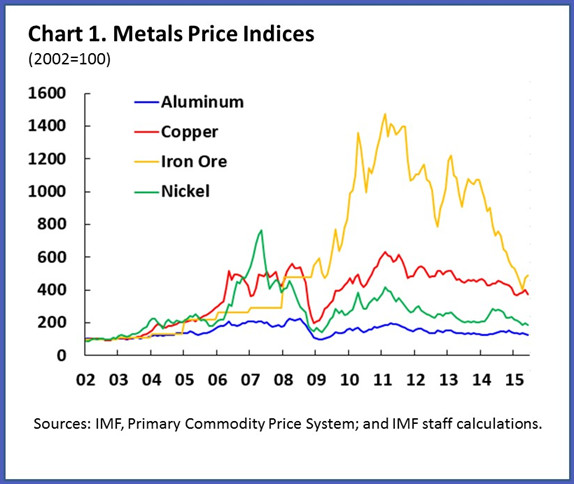

There is no doubt about the direction of the prevailing wind for metals in recent years. Prices have been gradually declining since 2011 (chart 1). While oil prices have also dropped, the decline is more recent (prices peaked in 2014), and more abrupt. That said, in both cases the downward pressure on prices result broadly from abundant production from the era of high prices. This is now coming to roost with lower demand from both emerging markets and advanced economies. There are importance nuances however in the relative strength and nature of those forces.

Appetite for production

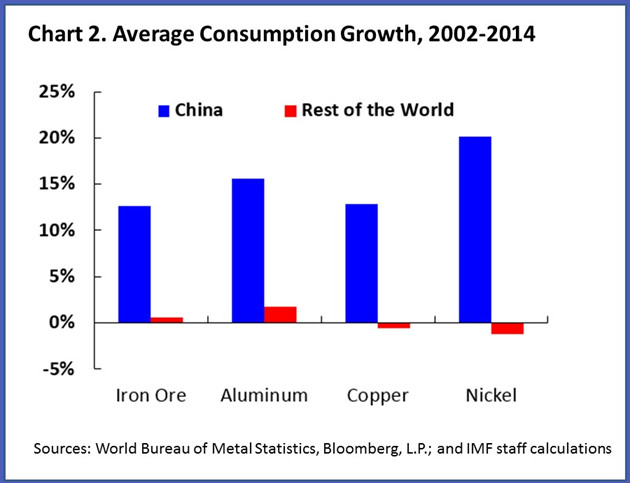

In the early 2000s, demand for metals shifted from advanced economies in the West to emerging markets in the East. China, by far the main driving force, now accounts for half of global base metal consumption (chart 2). Compare that with China’s more modest consumption of 14% of the world’s oil which is almost exclusively used for transportation.

It is therefore no surprise that metals prices are heavily influenced by demand, and the needs of one economic giant in particular. India, Russia and South Korea have also increased their metal consumption, but remain far behind China. The slower pace of investment in China in the last few years, however, compounded by concerns over future demand amid the sharp stock market decline and currency devaluation this summer, have been exerting downward pressure on metal prices.

Oil supply glut

Oil prices tell a different tale. Our view is that supply factors are playing a bigger role than demand. See also our blog from last December. OPEC’s decision to maintain its level of production and strong shale oil production in the United States — in addition to the large production capacity from earlier investment — have contributed to an unprecedented supply glut.

By IMF colleagues: Rabah Arezki and Akito Matsumoto

“It was the best of times, it was the worst of times.” With these words Charles Dickens opens his novel “A Tale of Two Cities”. Winners and losers in a “tale of two commodities” may one day look back with similar reflections, as prices of metals and oil have seen some seismic shifts in recent weeks, months and years.

This blog seeks to explain how demand — but also supply and financial market conditions — are affecting metals prices.

Posted by at 5:31 PM

Labels: Energy & Climate Change

Wednesday, September 9, 2015

Norway: Peak in Oil Fortunes?

“Norway’s half century of good fortune from its oil and gas wealth may have peaked,” according to an IMF report. “Oil and gas production will continue for many decades on current projections, but output and investment have flattened out, and the spillovers from the offshore oil and gas production to the mainland economy may have turned from positive to negative. Thus far, economic policy has needed to focus on managing the windfall, and Norway’s institutions have been a model for other countries. Read the full article…

Posted by at 5:35 PM

Labels: Energy & Climate Change

Subscribe to: Posts