Showing posts with label Energy & Climate Change. Show all posts

Tuesday, September 5, 2017

Oil Prices and Inflation Dynamics: Evidence from Advanced and Developing Economies

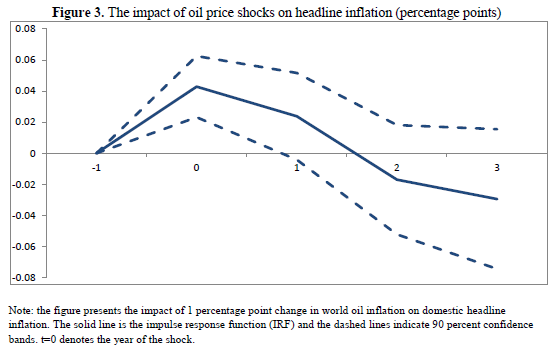

We study the impact of fluctuations in global oil prices on domestic inflation using an unbalanced panel of 72 advanced and developing economies over the period from 1970 to 2015. We find that a 10 percent increase in global oil inflation increases, on average, domestic inflation by about 0.4 percentage point on impact, with the effect vanishing after two years and being similar between advanced and developing economies. We also find that the effect is asymmetric, with positive oil price shocks having a larger effect than negative ones. The impact of oil price shocks, however, has declined over time due in large part to a better conduct of monetary policy. We further examine the transmission channels of oil price shocks on domestic inflation during the recent decades, by making use of a monthly dataset from 2000 to 2015. The results suggest that the share of transport in the CPI basket and energy subsidies are the most robust factors in explaining cross-country variations in the effects of oil price shocks during the this period.

Continue reading here.

We study the impact of fluctuations in global oil prices on domestic inflation using an unbalanced panel of 72 advanced and developing economies over the period from 1970 to 2015. We find that a 10 percent increase in global oil inflation increases, on average, domestic inflation by about 0.4 percentage point on impact, with the effect vanishing after two years and being similar between advanced and developing economies. We also find that the effect is asymmetric,

Posted by at 4:42 PM

Labels: Energy & Climate Change

Tuesday, July 25, 2017

Meeting EU Climate Pledges: Assessing Some Potential Policy Refinements

From a new IMF report:

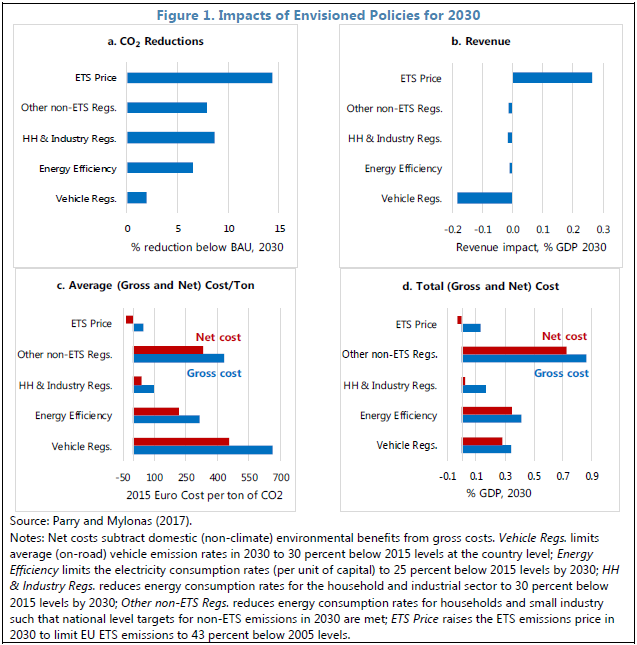

“For the 2015 Paris Agreement on climate change, the European Union (EU) pledged to reduce greenhouse gas (GHG) emissions by at least 40 percent below 1990 levels by 2030. Policies envisioned to achieve this goal include: tightening the Emissions Trading System (ETS) covering large emitting firms; requirements for energy efficiency, vehicle CO2 emission standards, and renewables; and policies to meet national-level targets for small-scale emissions sources outside of the ETS. This note analyses various refinements to the envisioned policy package that might meet the 2030 commitments with lower costs and greater fiscal and domestic environmental benefits (though implications for energy security are not considered). The results suggest potential economic and fiscal benefits from greater reliance on emissions pricing—for example, replacing tighter energy efficiency regulations with a higher ETS emissions price and use of carbon taxes (or tax-like instruments) for emissions outside the ETS sector. Other options, such as equating carbon charges across sectors and across countries, yield some economic benefits at the EU level, but do not raise revenue and, without compensating measures, impose uneven burdens across countries.”

Continue reading here.

From a new IMF report:

“For the 2015 Paris Agreement on climate change, the European Union (EU) pledged to reduce greenhouse gas (GHG) emissions by at least 40 percent below 1990 levels by 2030. Policies envisioned to achieve this goal include: tightening the Emissions Trading System (ETS) covering large emitting firms; requirements for energy efficiency, vehicle CO2 emission standards, and renewables; and policies to meet national-level targets for small-scale emissions sources outside of the ETS.

Posted by at 1:34 PM

Labels: Energy & Climate Change

Wednesday, July 5, 2017

Environment and Climate Change in Vietnam

A new IMF report finds:

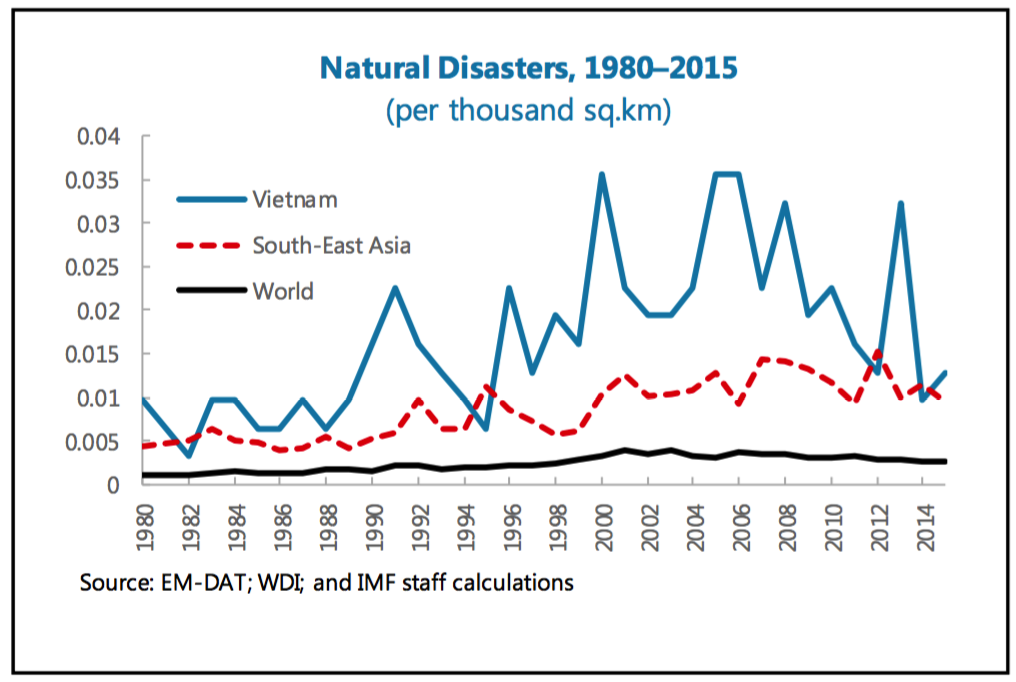

“Vietnam is highly affected by climate change. Its long coastline, geographic location, and diverse topography and climates contribute to Vietnam being one of the most hazard-prone countries in the Asia-Pacific region. Given the high concentration of the population and economic assets in coastal lowlands and the significant role played by agriculture and fisheries in the economy, Vietnam is ranked among the five countries likely to be most affected by climate change. Over the last 50 years, temperatures have increased twice as fast as the global average, the sea level has risen by 20 centimeters and the frequency and intensity of extreme weather events (drought, flood, salinization) have risen sharply. Natural disasters result in 470 fatalities and cost 0.8 percent of GDP (annual average between 1990 and 2016).

Climate risks pose immense challenges. Based on the authorities’ climate change scenarios, by the end of the century, sea levels are expected to rise by up to a meter. Sea waters would then cover 40 percent of the Mekong Delta area (where half of the country’s rice is produced), 3 percent of coastal provinces and 20 percent of Ho Chi Minh City, impacting directly 10–12 percent of the population and reducing GDP by 10 percent. The sectors most affected will be agriculture, aquaculture, energy transportation and tourism.”

Continue reading here.

A new IMF report finds:

“Vietnam is highly affected by climate change. Its long coastline, geographic location, and diverse topography and climates contribute to Vietnam being one of the most hazard-prone countries in the Asia-Pacific region. Given the high concentration of the population and economic assets in coastal lowlands and the significant role played by agriculture and fisheries in the economy, Vietnam is ranked among the five countries likely to be most affected by climate change.

Posted by at 11:27 PM

Labels: Energy & Climate Change

Wednesday, March 15, 2017

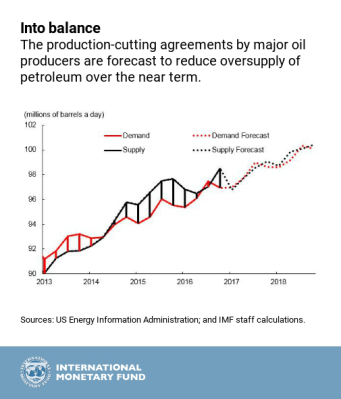

OPEC’s Rebalancing Act

From iMFdirect by Rabah Arezki and Akito Matsumoto:

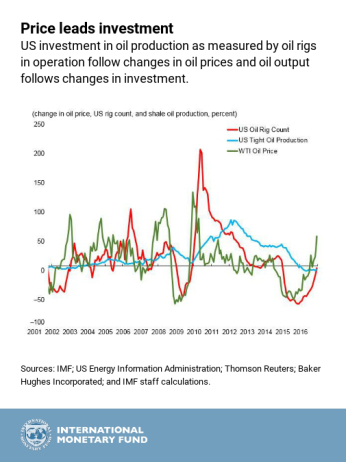

In November 2014, the Organization of Petroleum Exporting Countries (OPEC) decided to maintain output despite a perceived global glut of oil. The result was a steep decline in price.

Two years later, on November 30, 2016, the organization took a different tack and committed to a six-month, 1.2 million barrel a day (3.5 percent) reduction in OPEC crude oil output to 32.5 million barrels per day, effective in January 2017. The result was a small price increase and some price stability.

But the respite may be temporary, because the price increase is likely to stimulate other oil production that can come on line quickly. A recent sharp decline in prices because of higher than expected oil inventories in the United States underlines the temporary nature of the respite the OPEC agreement provides.

Continue reading here.

From iMFdirect by Rabah Arezki and Akito Matsumoto:

In November 2014, the Organization of Petroleum Exporting Countries (OPEC) decided to maintain output despite a perceived global glut of oil. The result was a steep decline in price.

Two years later, on November 30, 2016, the organization took a different tack and committed to a six-month, 1.2 million barrel a day (3.5 percent) reduction in OPEC crude oil output to 32.5 million barrels per day,

Posted by at 1:54 PM

Labels: Energy & Climate Change

Monday, January 30, 2017

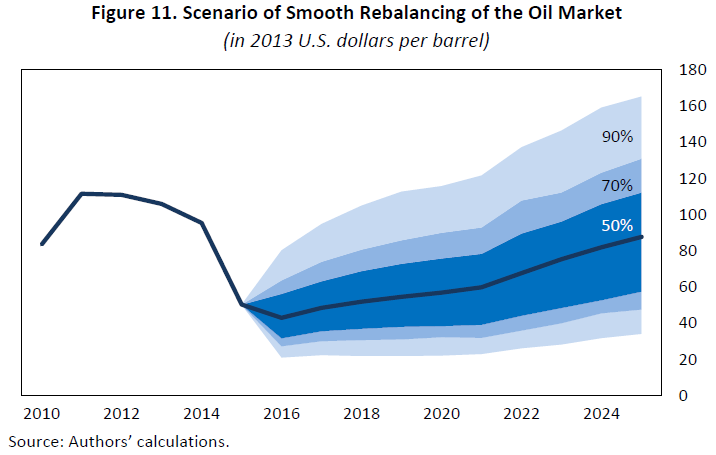

Where are Oil Prices Headed?

This paper by my IMF colleagues presents “a simple macroeconomic model of the oil market. The model incorporates features of oil supply such as depletion, endogenous oil exploration and extraction, and features of oil demand such as the increase in demand from emerging markets, usage efficiency, and endogenous demand responses. The model provides, inter alia, a useful analytical framework to explore the effects of: a change in world GDP growth; a change in the efficiency of oil usage; and a change in the supply of oil. The model shows that small shocks to oil supply or demand can result in large movements in the price of oil over time. It would not take a large shock for oil prices to return to significantly higher levels, and the long lags between oil price changes and the response of oil supply and demand to those changes can lead to cycles in oil prices in the future.”

Continue reading here.

This paper by my IMF colleagues presents “a simple macroeconomic model of the oil market. The model incorporates features of oil supply such as depletion, endogenous oil exploration and extraction, and features of oil demand such as the increase in demand from emerging markets, usage efficiency, and endogenous demand responses. The model provides, inter alia, a useful analytical framework to explore the effects of: a change in world GDP growth;

Posted by at 12:10 PM

Labels: Energy & Climate Change

Subscribe to: Posts