Showing posts with label Energy & Climate Change. Show all posts

Wednesday, March 14, 2018

The Long-Run Decoupling of Emissions and Output: Evidence from the Largest Emitters

From my latest IMF working paper with Gail Cohen, Joao Jalles, and Ricardo Marto:

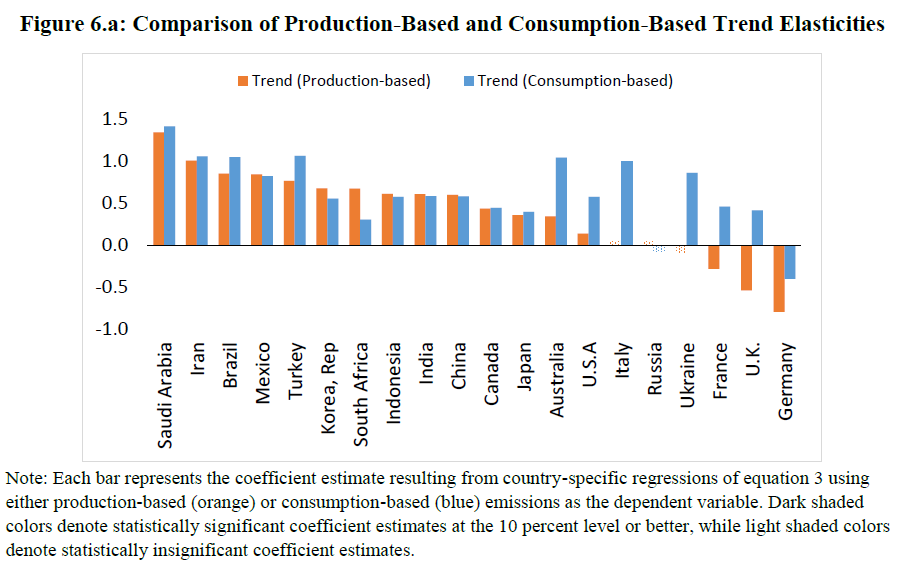

“For the world’s 20 largest emitters, we use a simple trend/cycle decomposition to provide evidence of decoupling between greenhouse gas emissions and output in richer nations, particularly in European countries, but not yet in emerging markets. If consumption-based emissions—measures that account for countries’ net emissions embodied in cross-border trade—are used, the evidence for decoupling in the richer economies gets weaker. Countries with underlying policy frameworks more supportive of renewable energy and climate change mitigation efforts tend to show greater decoupling between trend emissions and trend GDP, and for both production- and consumption-based emissions. The relationship between trend emissions and trend GDP has also become much weaker in the last two decades than in preceding decades.”

From my latest IMF working paper with Gail Cohen, Joao Jalles, and Ricardo Marto:

“For the world’s 20 largest emitters, we use a simple trend/cycle decomposition to provide evidence of decoupling between greenhouse gas emissions and output in richer nations, particularly in European countries, but not yet in emerging markets. If consumption-based emissions—measures that account for countries’ net emissions embodied in cross-border trade—are used,

Posted by at 4:35 PM

Labels: Energy & Climate Change

Saturday, March 3, 2018

Welfare Gains from Market Insurance: The Case of Mexican Oil Price Risk

From a new IMF working paper:

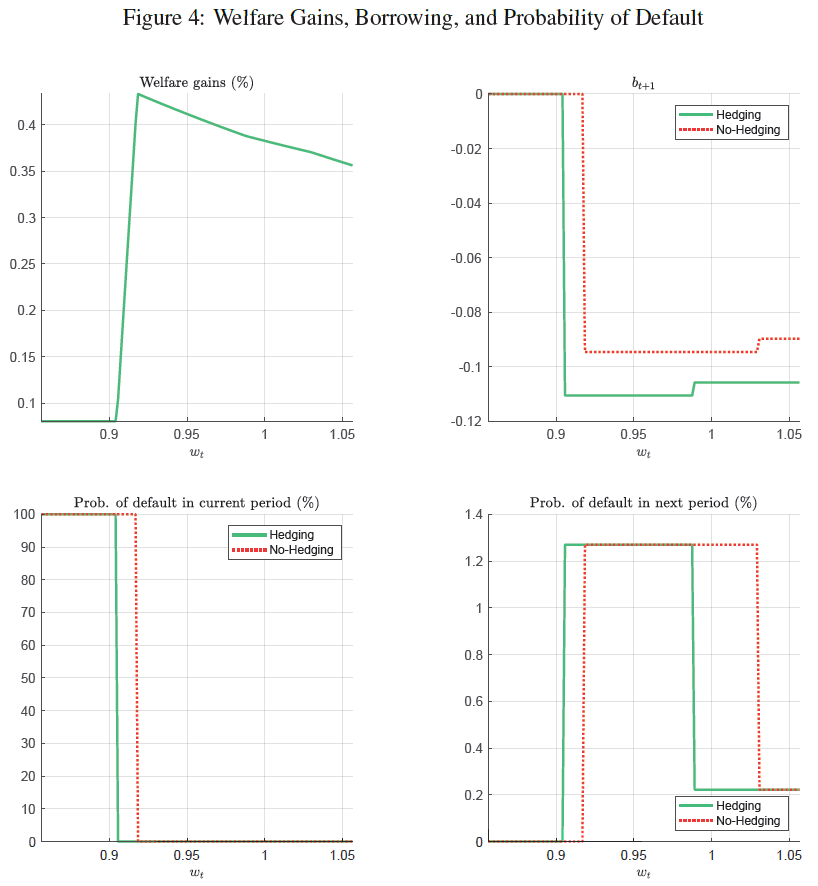

“Over the past two decades, Mexico has hedged oil price risk through the purchase of put options. We examine the resulting welfare gains using a standard sovereign default model calibrated to Mexican data. We show that hedging increases welfare by reducing income volatility and reducing risk spreads on sovereign debt. We find welfare gains equivalent to a permanent increase in consumption of 0.44 percent with 90 percent of these gains stemming from lower risk spreads.”

From a new IMF working paper:

“Over the past two decades, Mexico has hedged oil price risk through the purchase of put options. We examine the resulting welfare gains using a standard sovereign default model calibrated to Mexican data. We show that hedging increases welfare by reducing income volatility and reducing risk spreads on sovereign debt. We find welfare gains equivalent to a permanent increase in consumption of 0.44 percent with 90 percent of these gains stemming from lower risk spreads.”

Posted by at 9:13 AM

Labels: Energy & Climate Change, Inclusive Growth

Friday, February 2, 2018

Adapting to Climate Change: Pricing Right, Taxing Smart, and Acting Now

From a speech by IMF Deputy Managing Director Zhang Tao at the United Nations Investor Summit on Climate Risk

“We recently have seen the IMF appearing to step up its work on climate change. Why now?

The Short Answer: This is our response to the threat climate change poses to our planet—and the growing demand from our membership and the international community to respond.

The IMF has been involved in the climate change work for several years. Our recent work reflects compelling evidence that adapting to climate change is one of the most important challenges facing economic policy makers worldwide. The IMF also has an obligation as a member of international community to address the doubts about climate change with fact-based analysis.

The Long Answer: the Fund’s core mandate is to ensure economic stability and resilience. Climate change could prove to be a destabilizing force for the global economy if it is not addressed.

The macroeconomic impact of climate change was illustrated by the especially damaging hurricane season last year in the Caribbean and the U.S. We certainly will see more frequent and more damaging such natural disasters in the future.

So, the key question is what we can do—and do better—in helping policymakers confront the challenges of climate change?

Two key areas of work are: mitigation, which includes helping countries meet their commitments under the Paris Agreement to reduce emissions; and adaptation, which focuses on building resilience to climate change. Our general message to our membership with regard to meeting the goals of the Paris agreement to contain emissions is to “price it right; tax it smart; and do it now.” ”

Continue reading here.

From a speech by IMF Deputy Managing Director Zhang Tao at the United Nations Investor Summit on Climate Risk

“We recently have seen the IMF appearing to step up its work on climate change. Why now?

The Short Answer: This is our response to the threat climate change poses to our planet—and the growing demand from our membership and the international community to respond.

The IMF has been involved in the climate change work for several years.

Posted by at 1:30 AM

Labels: Energy & Climate Change

Saturday, January 20, 2018

2018 AEA Annual Meeting’s Papers on Climate Change and Energy

On climate change

- Expect Above Average Temperatures: Identifying the Economic Impacts of Climate Change – Paper

- The Impact of Weather on Local Employment: Using Big Data on Small Places – AEA

- Winter is Coming: The Long-run Effects of Climate Change on Conflict, 1400-1900 – Paper

- Regulating Mismeasured Pollution: Implications of Firm Heterogeneity for Environmental Policy – Paper

- Climate Change and Civil Unrest: Evidence From the El Niño Southern Oscillation – Paper – AEA

- Military Planning in a Context of Complex Systems and Climate Change – AEA

- Who Joined the Pigou Club? A Postmortem Analysis of Washington State’s Carbon Tax Initiative I-732 – Paper

- Decoupling Agricultural and Malarial Channels of Climate-driven Infant Mortality in Sub-Saharan Africa – AEA

- How Large is the Potential Economic Benefit of Agricultural Adaptation to Climate Change? – Paper and Presentation

- Firm and Household Responses to Climate Change Risks – AEA

- ACE – Analytic Climate Economy (with Temperature and Uncertainty) – Paper

- Expect Above Average Temperatures: Identifying the Economic Impacts of Climate Change – Paper

- Same Storm, Different Disasters: Consumer Credit Access, Income Inequality, and Natural Disaster Recovery – Paper

- Heterogeneous firms under regional temperature shocks: exit and reallocation, with evidence from Indonesia – Paper

- The Costs of Inefficient Regulation: Evidence from the Bakken – Paper

- Clean Energy Investments for New York State: An Economic Framework for Promoting Climate Stabilization and Expanding Good Job Opportunities – AEA

- Spatial Effects of Nitrogen Pollution on Drinking Water Production – Paper

- Regulating Mismeasured Pollution: Implications of Firm Heterogeneity for Environmental Policy – Paper

- Assessing the External Net Benefits of Wind Energy: The Case of Iowa’s Wind Farms – Paper

- Do HOV Lanes Save Energy? Evidence from a General Equilibrium Model of the City – Paper

On oil market

- Informing SPR Drawdown Policy through Oil Futures and Inventory Dynamics – Paper

- Measuring Leakage Risk – AEA

- How Trade-sensitive are Energy-intensive Sectors? – AEA

- Gasoline Savings From Clean Vehicle Adoption – Paper

- Response of Consumer Debt to Income Shocks: The Case of Energy Booms and Busts – Paper and Presentations

- Granger Causality of Real Oil Prices After the Great Recession – Paper and Presentation

- Did the Renewable Fuel Standard Shift Market Expectations of the Price of Ethanol? – Paper

- Evaluating a Discretionary Safety Valve: The Economic and Environmental Impacts of Waiving Fuel Content Regulations in Response to Supply Shocks – Paper

On shale gas

- Local Economic Shocks and Entrepreneurship: New Business Formation During the Shale Oil and Gas Boom – Paper

- Collateral Damage: The Impact of Shale Gas on Mortgage Lending – Paper

- The Local Effects of the Texas Shale Boom on Schools, Students, and Teachers – Paper

- Analyzing the Risk of Transporting Crude Oil by Rail – Paper

- Local Labor Market Shocks and Wage Differentials: Evidence From Shale Oil and Gas Booms – Paper

On carbon market

- Lessons From China’s Seven Regional Carbon Market Pilots – AEA

- China’s Rate-Based Approach to Reducing CO2 Emissions: Strengths, Limitations, and Alternatives – Paper

- Design Issues in China’s National Carbon Market – Paper

- Who Joined the Pigou Club? A Postmortem Analysis of Washington State’s Carbon Tax Initiative I-732 – Paper

- Do Carbon Taxes Kill Jobs? New Heterogeneous Evidence from British Columbia – Paper

- Emissions Containment in Response to Carbon Market Prices – Paper and Presentation

- Pigou Creates Losers: On the Impossibility of Pareto Improvements From Pigouvian Taxes – AEA

On solar energy

- Pass-Through as a Test for Market Power: An Application to Solar Subsidies – Paper

- What Drives Social Contagion in the Adoption of Solar Photovoltaic Technology? – Paper

- What Drives Social Contagion in the Adoption of Solar Photovoltaic Technology? – Paper

- Siting Solar PV Capacity to Maximize Environmental Benefits – Paper

On electricity

- What’s killing nuclear power in U.S. electricity markets? Drivers of wholesale price declines at nuclear generators in the PJM Interconnection – Paper and Presentation

- Who Pays In Deregulated Electricity Markets? – Paper

- Determinants of the Cost of Electricity Supply in India – AEA

On vehicle market

- Self-Driving Cars and the City: Long-Run Effects on Land Use, Welfare, and the Environment – Paper

- Attribute Substitution in Household Vehicle Portfolios – Paper

- Mind the Gap! Tax Incentives and Incentives for Manipulating Fuel Efficiency in the Automobile Industry – AEA

- Does an Energy Efficiency Gap Exist in the Light-duty Vehicle Market? Evidence From Fuel-saving Technology Adoption – Paper

On climate change

- Expect Above Average Temperatures: Identifying the Economic Impacts of Climate Change – Paper

- The Impact of Weather on Local Employment: Using Big Data on Small Places – AEA

- Winter is Coming: The Long-run Effects of Climate Change on Conflict, 1400-1900 – Paper

- Regulating Mismeasured Pollution: Implications of Firm Heterogeneity for Environmental Policy – Paper

- Climate Change and Civil Unrest: Evidence From the El Niño Southern Oscillation – Paper – AEA

- Military Planning in a Context of Complex Systems and Climate Change – AEA

- Who Joined the Pigou Club?

Posted by at 7:19 PM

Labels: Energy & Climate Change

Tuesday, January 9, 2018

For Vietnam, Greener Growth Can Reduce Climate Change Risks

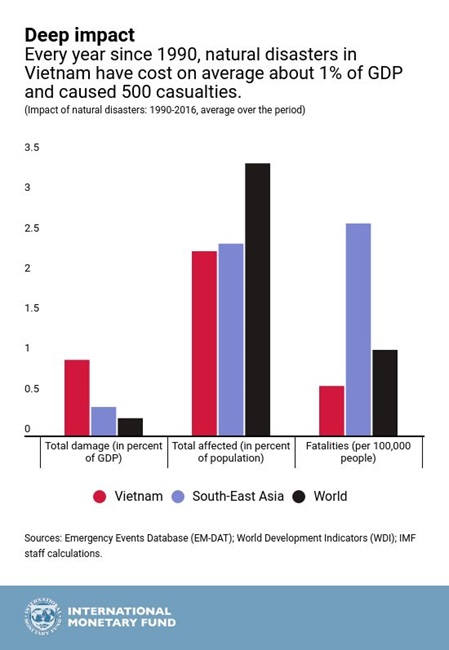

A new IMF report says that: “By 2100, climate change could impact more than 12 percent of the Vietnamese population and reduce growth by 10 percent. The Vietnamese government considers the response to climate change a vital issue and has implemented environmental policies to better cope with these risks.”

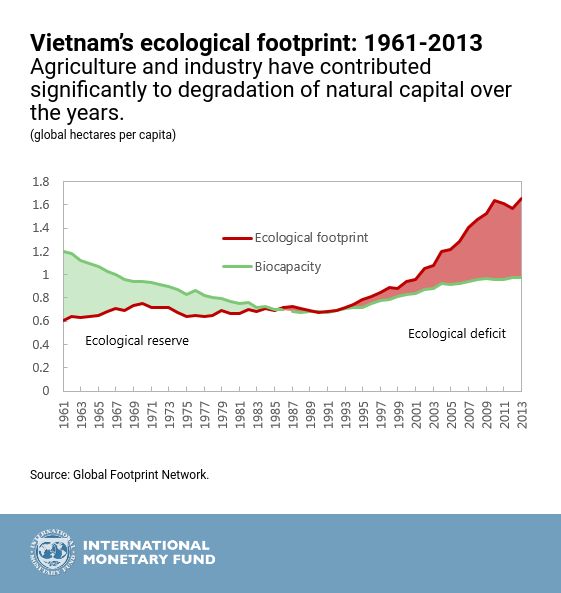

“But the country—which has relied heavily on fossil fuels and overexploitation of natural resources—needs to further adapt its economy toward a more sustainable and ecofriendly growth model.”

“Policies that can better prepare Vietnam for the future impact of climate change should focus on:

- Lowering the intensity of fossil fuels in Vietnam’s GDP: raising the contribution of renewable energy would help to break the link between greenhouse gas emissions and output.

- Providing stronger incentives for households, firms, and government to pursue green growth: taxation of fossil fuels that fully prices environmental and health externalities would nudge energy demand toward renewables and generate revenue to finance adaptation and mitigation plans.

- Investing in climate resilient infrastructure would help households and firms cope with storms. The expected cost of natural disasters could be usefully included in public debt sustainability analyses.

- Promoting research and development and other innovation policies can provide further incentives to investment in existing clean energy sources and improvements in clean technologies.

- Shifting to autonomous, electric, shared vehicles, as already planned in Singapore, would help reduce congestion and pollution in cities. Improved government capacity to coordinate technological change and promote innovation and green growth would be key.”

A new IMF report says that: “By 2100, climate change could impact more than 12 percent of the Vietnamese population and reduce growth by 10 percent. The Vietnamese government considers the response to climate change a vital issue and has implemented environmental policies to better cope with these risks.”

“But the country—which has relied heavily on fossil fuels and overexploitation of natural resources—needs to further adapt its economy toward a more sustainable and ecofriendly growth model.”

Posted by at 9:01 PM

Labels: Energy & Climate Change

Subscribe to: Posts