“The world is getting hotter, resulting in rising sea levels, more extreme weather like hurricanes, droughts, and floods, as well as other risks to the global climate like the irreversible collapsing of ice sheets.

Here are five ways the IMF helps countries move forward with their strategies as part of their commitment to the 2015 Paris Agreement on Climate Change.

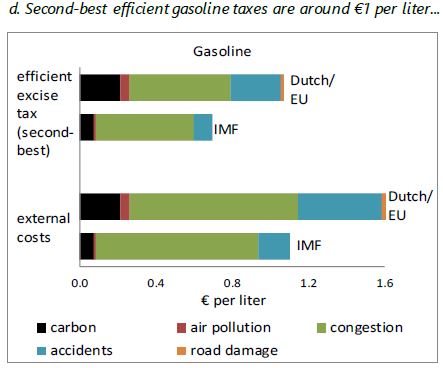

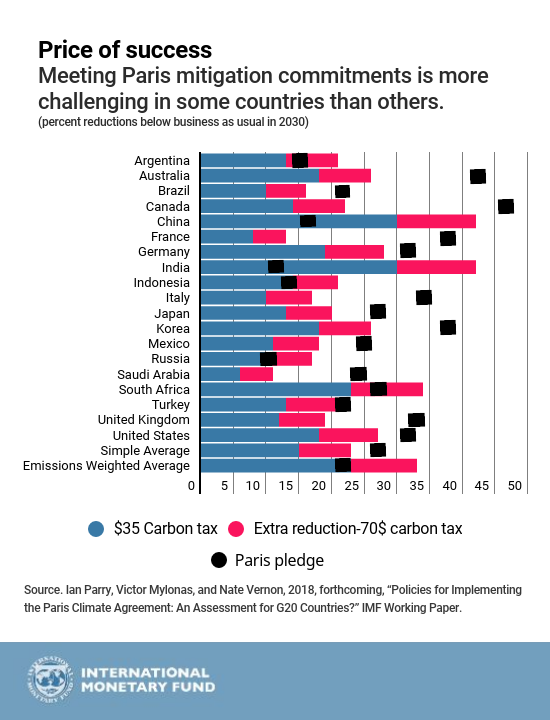

- Mitigate emissions. Carbon taxes, or similar charges for the carbon content of coal, petroleum products, and natural gas, are potentially the most effective instruments to reduce carbon dioxide emissions, the major source of heat-trapping gases. These taxes are straightforward to administer, for example, building off existing fuel excises, and can raise significant revenue for government that they might use to cut other burdensome taxes on the economy, or fund growth-enhancing investments.The IMF provides practical guidance on the design of fiscal policy to mitigate climate change. We are developing spreadsheet tools to help countries gauge the emissions, and broader fiscal and economic impacts of carbon pricing, and the trade-offs across alternative mitigation instruments like taxes on individual fuels, emissions trading, and incentives for energy efficiency.For example, our annual economic review for China showed that a carbon tax, or just a tax on coal use, would be significantly more effective at reducing carbon and local air pollution emissions than emissions trading systems which do not cover emissions from vehicles and buildings, and would also raise substantial revenue.And according to our forthcoming working paper, a $70 price per ton on carbon dioxide emissions in 2030, which would increase gasoline prices by about 60 cents per gallon, and more than triple coal prices, would be more than sufficient to meet mitigation pledges in some advanced and emerging market economies like China, India, Indonesia, and South Africa. That price would be nearly sufficient in some other countries like Turkey and the United States, but well short of what Australia, Canada, and some European countries need.These differences in the ability of the $70 price to meet mitigation pledges reflect both differences in the stringency of commitments, and in the responsiveness of fuels and emissions to pricing. For example, emissions tend to be more responsive to pricing in countries that use a lot of coal, like China, India, and South Africa.

- Energy subsidy reform. Pricing carbon should be part of a broader strategy to reflect the full range of social costs in energy pricing. This includes deaths from air pollution and other local environmental side effects from fuel use. A spreadsheet tool provides, for all member countries, estimates of the energy prices needed to reflect supply, and all environmental costs, as well as the implicit subsidies from underpricing fossil fuels.According to IMF estimates, efficient energy pricing would have reduced global carbon emissions in 2013 by over 20 percent, and fossil fuel air pollution deaths by over 50 percent, while raising revenues of 4 percent of GDP.

IMF case studies of numerous countries’ reforms distill the ingredients for successful reform. One especially important ingredient is compensation for low-income households, which generally requires only a small fraction of the revenues generated from reform. We discuss energy price reforms as part of our annual review of a country’s economy, as well as in our technical assistance work with countries like Saudi Arabia , Jordan, United Arab Emirates, and in our courses and workshops.”

Continue reading here.