Tuesday, October 27, 2015

On U.S. Labor Market Slack: Updated Estimates of the Impact of Uncertainty on Unemployment

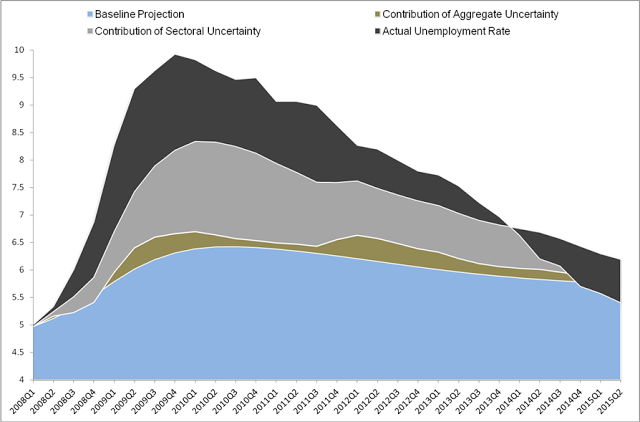

We find that aggregate uncertainty contributed a bit to unemployment in 2009 and again in 2012 (this is the portion of the chart shown in brown). Our aggregate uncertainty measure is the realized volatility of S&P 500 index returns, similar to Bloom (2009).

Our sectoral uncertainty measure is the cross-section dispersion in excess returns across various industries. We show in our paper that this measure of uncertainty tends to have more persistent impacts on unemployment than aggregate uncertainty. The contribution of sectoral uncertainty to U.S. unemployment was important in mid-2010—this was the result that Bob Samuelson cited in his column at the time. But the contribution of sectoral uncertainty has declined steadily ever since and is essentially zero at present. (This is the portion of the chart shown in grey.)

The main reason for the decline in unemployment is the resumption of growth and unemployment’s own dynamics; their contribution is shown as part of the other factors in the chart above (the portion shown in black).

Details are provided in our paper. Please note that as in other IMF working papers, the views expressed in this paper are those of the authors and should not be ascribed to the IMF.

Posted by at 12:00 PM

Labels: Inclusive Growth

Subscribe to: Posts