Thursday, June 17, 2021

Housing Market in Cyprus

From the IMF’s latest report on Cyprus:

“Nevertheless, challenges are building. Nearly half of legacy NPLs were terminated five years earlier, potentially requiring sizable write-downs (Annex VI). Foreclosures have been suspended until end-July for smaller, collateralized loans and proposals under discussion in Parliament are expected to weaken the framework (¶22, third bullet). More than 80 percent of bank loans are to highly leveraged households and SMEs, concentrated in sectors like accommodation, food and retail, implying a high risk of an escalation of default rates and lower recovery value of assets after the expiry of loan repayment and foreclosure moratorium (Box 1). Banks are also exposed to property market risks through real estate holdings and collateral valuation. Although regulatory forbearance and fiscal support have prevented an immediate surge in loan impairments, a new wave of defaults as loan repayment obligations resume amidst tapering fiscal support could quickly consume the capital buffers of banks. Based on a stylized scenario with a 10 percent increase10 in NPLs that would push the latter to some 19.5 percent of total loans from the current 17.7 percent, staff estimates that restoring capital and provisions to pre-pandemic levels would entail capital needs of 1.5 percent of GDP.

(…)

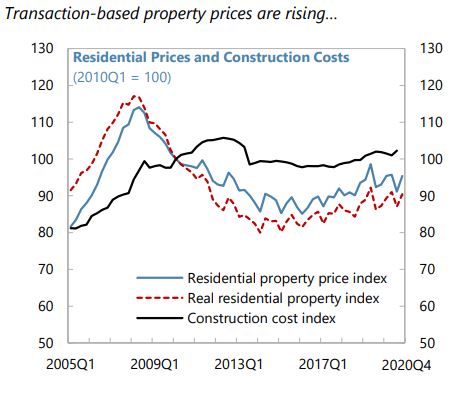

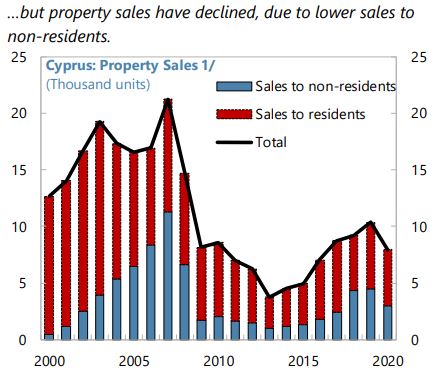

Macro-financial risks from possible declines in property prices should be closely monitored, especially given the continued active use of debt-to-asset swaps in NPL resolution by banks and CACs. Risks appear limited for now given stable residential price developments (Text Figure 5 and Figure 8) and limited size of commercial real estate transactions. To ensure proper collateral valuation, results of actual sales transactions of repossessed collateral properties should be used by banks and CACs to review adequacy of valuation methodologies of these assets. Supervisory guidance to prevent excessive holding of repossessed collateral assets by banks should be maintained.”

Posted by at 3:27 PM

Labels: Global Housing Watch

Subscribe to: Posts