Wednesday, February 13, 2019

Housing Market in Croatia

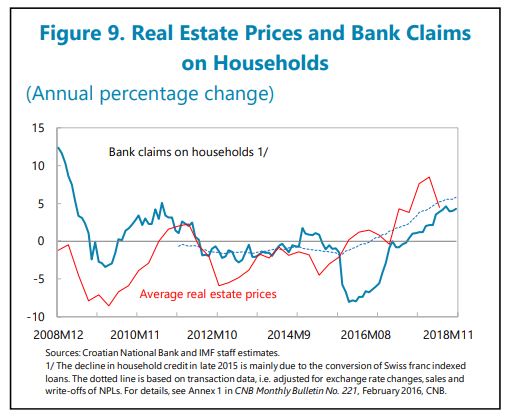

From the IMF’s latest report on Croatia:

“The real estate market is also picking up, albeit from a low base and the recovery is rather segmented. Should both household borrowings and real estate prices further accelerate, additional macro prudential measures may need to be considered, including a comprehensive debt-service-to-income ratio capturing all debts, not just debts related to housing loans. Since May 2018, new loans are no longer reported to the credit register run by the Croatian Banking Association due to concerns of some banks about the implementation of the General Data Protection Regulation (GDPR). Staff recommended to shortly resolve these legal issues.”

“Macroprudential policies can contain possible pressure points. If real estate prices accelerate or high growth of cash loans persists, authorities could consider the introduction of additional measures to prevent excessive household borrowing (e.g., more comprehensive use of debt-service-to-income limits). Enhancements to the efficiency of bankruptcy procedures (e.g., by facilitating out-of-court settlements) would help further private sector deleveraging. Despite recent changes in the bankruptcy legislation, a comprehensive review to ensure that the insolvency framework aligns with best practices merits strong consideration.”

Posted by at 9:40 AM

Labels: Global Housing Watch

Subscribe to: Posts