Sunday, March 11, 2018

Economic Forecasts with the Yield Curve

From the Federal Reserve Bank of San Francisco:

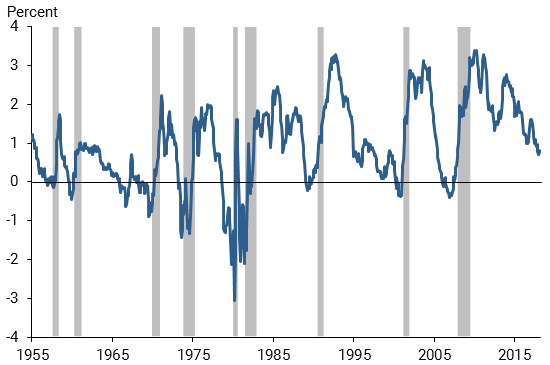

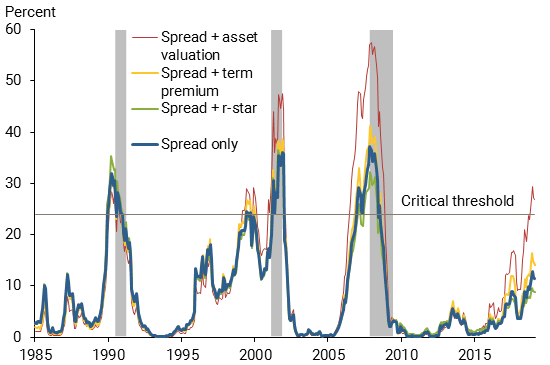

“Forecasting future economic developments is a tricky business, but the term spread has a strikingly accurate record for forecasting recessions. Periods with an inverted yield curve are reliably followed by economic slowdowns and almost always by a recession. While the current environment appears unique compared with recent economic history, statistical evidence suggests that the signal in the term spread is not diminished. These findings indicate concerns about the scenario of an inverting yield curve. Any forecasts that include such a scenario as the most likely outcome carry the risk that an economic slowdown might follow soon thereafter.”

Figure 1

The term spread and recessions

Note: Gray bars indicate NBER recession dates.

Figure 2

Estimated probabilities of recession based on term spread

Note: Gray bars indicate NBER recession dates.

Posted by at 9:46 AM

Labels: Macro Demystified

Subscribe to: Posts