Monday, July 4, 2016

The Danish Housing Market: An Update

“Rapid house price increases call for early policy action—including loosening housing supply restrictions, eliminating adverse tax incentives, and developing and timely implementing well-targeted macro prudential tools”, says IMF’s latest report on Denmark. The report points out that “Following speculative pressures on the exchange rate in early 2015, Denmark’s Nationalbank (DN) lowered its deposit policy rate—which first broke through the zero bound in 2012—deeper into negative territory (…). In the resulting environment of historically low mortgage rates, real house prices rose over 6 percent in 2015.”

In two separate reports, Giang Ho (IMF) provides a deeper analysis on house price and supply developments in Denmark.

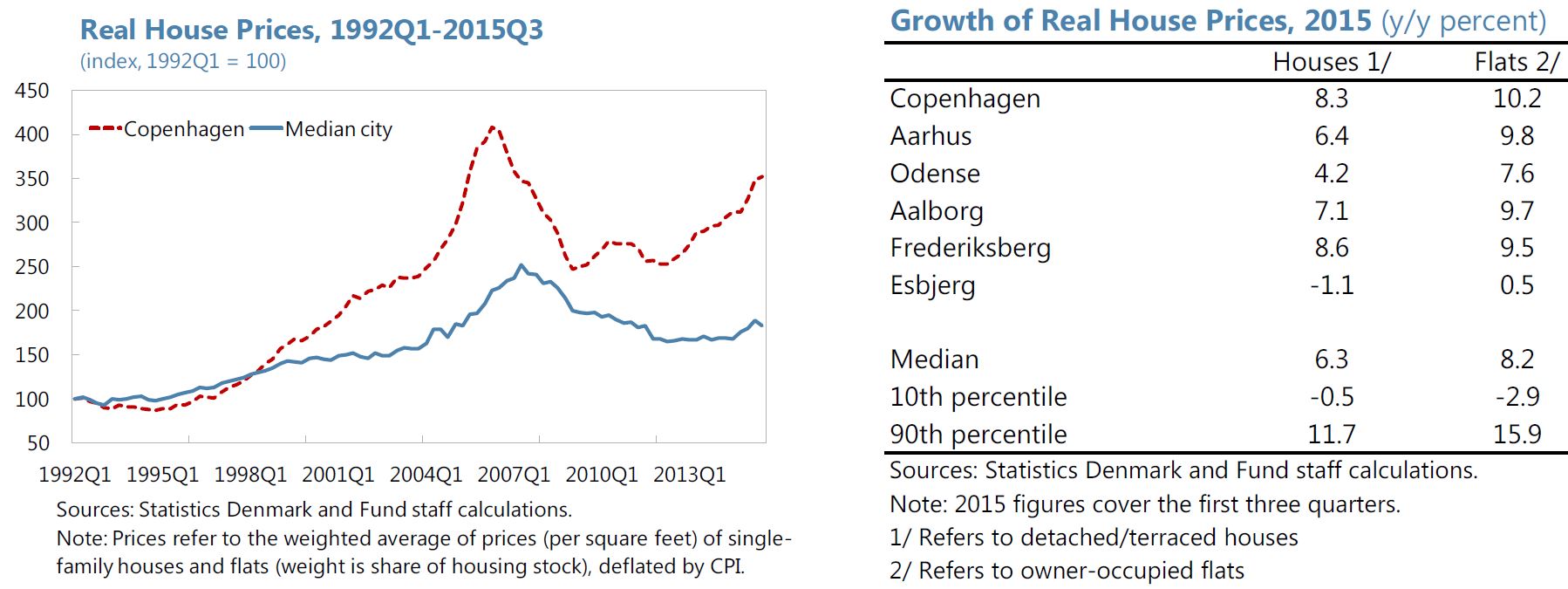

On house prices, Ho says that price developments have been characterized by a “growing divergence” between different parts of the country. Big cities such as Copenhagen has experienced much more rapid price increases than other parts. A similar development is also seen in the market for owner-occupied flats (experincing larger price increases) compared to single-family homes. These regional house price differences are explained by a number of demand and supply factors: demographic trends, rising income and employment, favorable user cost of housing, and housing supply lagging behind demand. Ho’s analysis also points to “emerging overvaluation in Copenhagen and Frederiksberg’s housing markets—particularly in the market for owner-occupied flats.”

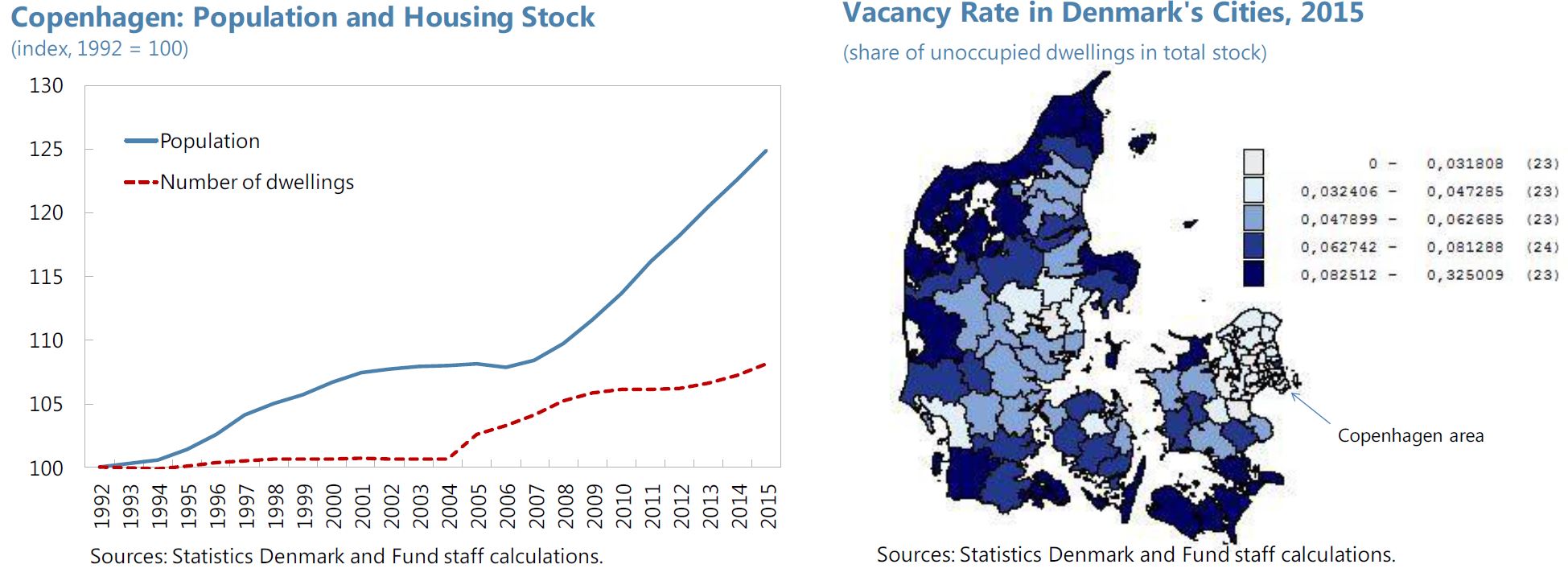

On housing supply, “Cities such as Copenhagen where the stock of housing is relatively inflexible and responds slowly to changes in housing demand could see higher price growth (…) the potential price impact of supply constraint can be economically significant”, says Ho. So how the supply constraints can be addressed? “While natural land constraints are difficult to overcome, distortions in the housing markets could be reduced to alleviate the supply shortage in high-stress urban areas such as Copenhagen. For example, there is scope for relaxing zoning regulations in certain areas. In addition, reducing rental controls to allow freely determined rents to apply to a larger fraction of the housing stock, and creating the incentives for municipalities and/or private developers to put land to good use would also be helpful. This is particularly relevant in the current juncture, given the low interest rate environment as well as the recent influx of asylum seekers putting additional pressure on the demand for housing”, according to Ho.

In another report on macroprudential policy, Jiaqian Chen (IMF), notes that given high household debt and other mortgage characteristics–like variable rates and interest only loans–financial stability concerns could emerge if house price growth continues. She estimates the potential effects of tightening macro prudential policies. She finds that “First, the overall impact from macroprudential policies on the real economy appears limited, while the effect on debt levels can be significant. Second, out of the various modeled policies, amortization requirements seem to have the strongest impact on household debt, suggesting the importance of limiting the growth of deferred amortization mortgages.”

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts