Friday, January 18, 2013

House Prices in Hong Kong

Two different pricing models are examined, which provide some mild, but on balance inconclusive, evidence that prices are higher than suggested by current fundamentals.

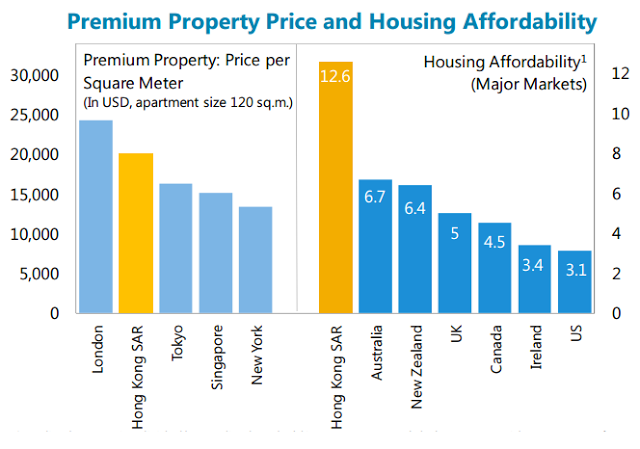

Housing in Hong Kong SAR is expensive. Compared to other regions, house prices in Hong Kong SAR are less affordable as measured by the ratio of median household income to median house price. In absolute terms, U.S. dollars per square meter, prices are also relatively expensive and premium real estate prices are on par or higher than in other high-cost housing.

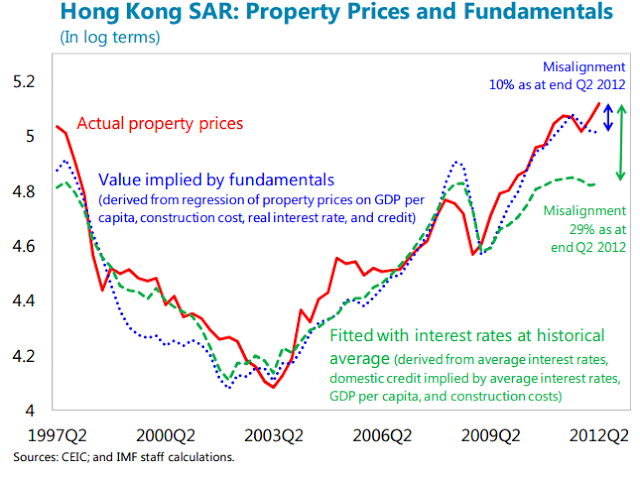

A regression-based approach indicates prices are about 10 percent above the level suggested by current macroeconomic fundamentals.However, the fundamentals themselves are in some sense abnormal, as loose global monetary conditions have pushed down considerably Hong Kong SAR’s real interest rate. The real interest rate, moreover, is a key driver of housing prices in the model. To illustrate the impact of the eventual normalization of global monetary conditions, the regression estimates were used to calculate the price that would prevail if the real interest rate was at its 2003–07 average, with a concomitant change to credit. This exercise suggests that housing prices are some 30 percent higher than they would be if Hong Kong SAR’s real interest rate returned to the 2003–07 average. An asset pricing model, however, finds that prices are broadly consistent with fundamentals. The model compares the market price with a benchmark based on an equilibrium relationship between prices, rents, and cost of ownership. The basis for assessing misalignment from fundamentals is that the cost of owning a house (imputed rent) should be the same as the cost of renting a similar house for the same time period. By this measure, smaller-sized flats are found to be some 7 percent above the benchmark while the luxury end of the market is found to be slightly below the corresponding benchmark.

Posted by at 12:41 PM

Labels: Global Housing Watch

Subscribe to: Posts