Wednesday, April 27, 2022

Lessons Learned from Housing Policy during COVID-19

From a new work at Brookings by Kris Gerardi, Lauren Lambie-Hanson, Paul Willen, Laurie Goodman, and Susan Wachter:

“Evidence on housing policy

- The national forbearance mandate, foreclosure moratorium, enhanced Unemployment Insurance (UI), and Economic Impact Payments (EIPs) aided in reducing financial distress for both owners and renters at the outset of the pandemic and prevented longer-run problems in mortgage and housing markets.

- Over 80 percent of borrowers who missed a mortgage payment in the first three months of the pandemic enrolled in forbearance. Although minority mortgage borrowers were much more likely to experience distress and miss mortgage payments, conditional on missing payments, forbearance uptake was similar across racial and ethnic lines.

- Low interest rates led to a wave of refinancing, but fewer Black borrowers benefited from refinancing than white borrowers.

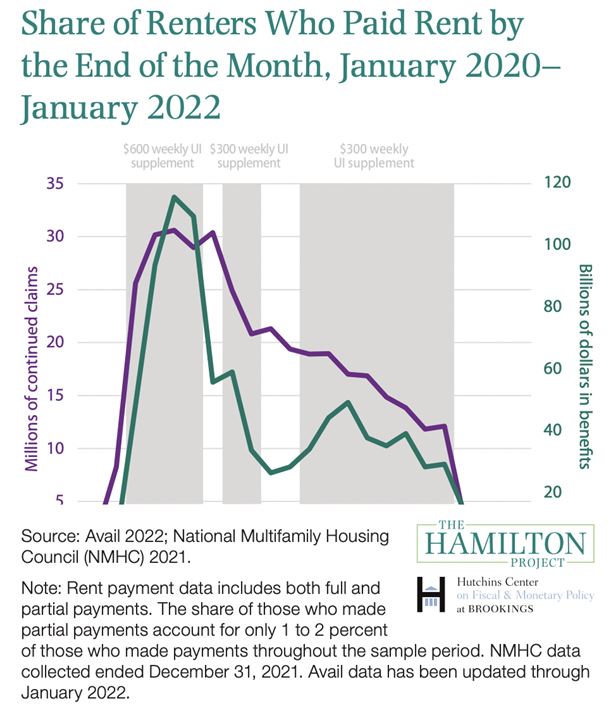

- The share of renters behind on rental payments has been above 2017 levels since 2020. Renter households who missed a rental payment were more likely to be lower-income households and were disproportionately minority households. Missed payments were most common among households who were struggling prior to the pandemic. The erratic rollout of the ERA, which was administered at the local level, prevented timely or easy access to these funds.

- Eviction moratoria resulted in a redirection of scarce household resources to immediate consumption needs and likely prevented homelessness. The decline in evictions during the pandemic is not solely the result of the eviction moratorium. The decline may also reflect the impact of ERA, greater access to legal aid, the impact of eviction diversion programs, and income replacement for households.”

Read the full chapter here.

Posted by at 10:16 AM

Labels: Global Housing Watch

Subscribe to: Posts