Tuesday, March 8, 2022

Housing Market in Hong Kong

From the IMF’s latest report on Hong Kong:

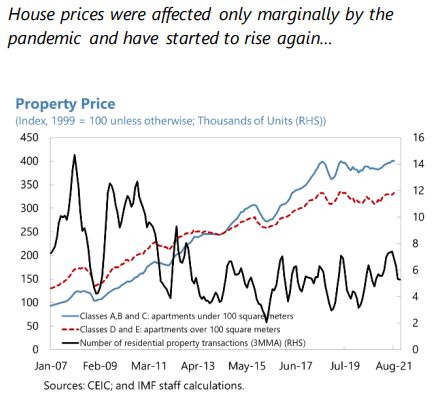

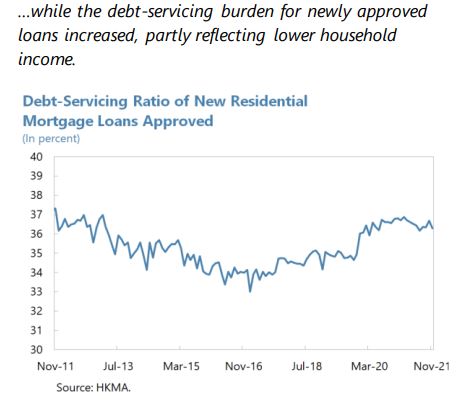

“Residential house prices are on the rise again, contributing to a further increase in the already elevated level of household debt. The average debt-servicing ratio for new mortgages increased to 36.9 percent at its peak in February 2021 from 36.0 percent in December 2019, partly driven by the decline in household income. While household assets are large in aggregate—as reflected by the high household net worth-to-liabilities ratio of 11.2 times and safe assets-to-liabilities ratio of 2.9 times in 2019—the wealth distribution is skewed towards high-income households.

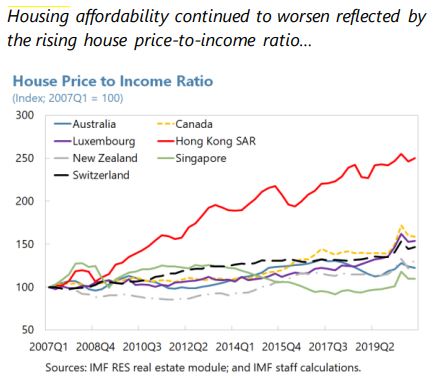

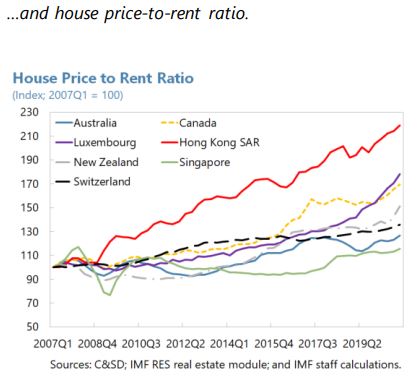

Given the stretched valuation, a disorderly adjustment in the property market could pose a risk to the economy. A sharp house price correction could trigger an adverse feedback loop between house prices, debt service capacity, household consumption, and growth, negatively affecting banks’ balance sheets. In addition, the FSAP analysis indicated that low-income households could be under significant financial stress when facing rising interest rates and falling income. To mitigate such risks, the authorities should continue to carefully monitor the household debt repayment capacity, particularly for low-income households.

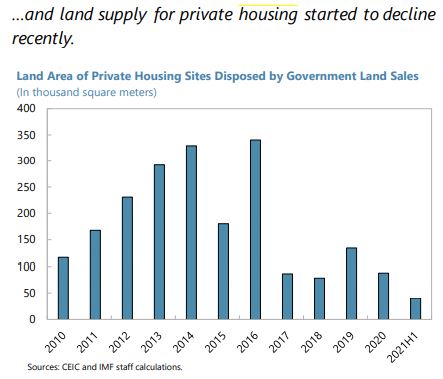

The three-pronged approach to increasing housing affordability and containing housing market risks remains valid, but more efforts are needed to raise housing supply.

*Increasing housing supply is critical to resolve the structural supply-demand imbalance. Housing supply has increased on average since 2015 with the implementation of the government’s Long-term Housing Strategy and the Hong Kong 2030+ Strategy, but has fallen short of target by about 30 percent on average. Staff welcomes the identification of the land to provide 330,000 public housing units within the next ten years and urges the authorities to bring the actual public housing production back to the target without further delays. To this end, a comprehensive approach is urgently needed, including increasing land supply for housing production (e.g., land resumption, reclamation, and re-zoning) while expediting and streamlining the process for land identification and production (e.g., environmental, transport, and other relevant assessments). The recently announced Northern Metropolis development strategy could boost housing supply over the longer-term period.

**The macroprudential stance for property markets should be maintained to safeguard financial stability. A series of macroprudential policies that have been introduced and tightened since 2009—such as ceilings on loan-to-value (LTV) ratio, caps on debt service-to-income ratio (DSR), and stress testing of the DSR against interest rate increases—have helped contain vulnerabilities in the banking system (…). Given resilient house prices and mortgage growth, the existing residential property-related macroprudential policies should be kept unchanged for now and any changes should be data-dependent with due attention to the emerging risk of regulatory leakages. Moreover, the Council of Financial Regulators (CFR) should take the lead in strengthening the regular surveillance and data collection on lending by non-bank lenders (e.g., property developers and non-bank financial institutions), and the authorities should regularly reassess the need to expand the regulatory perimeter to mitigate the leakages in macroprudential policies.

***Stamp duties have been effective in containing speculative activity and external demand. The government has introduced three types of stamp duties to curb excess demand by both residents and nonresidents. Although they have helped curb house price increases and contain household leverage and systemic risks, the New Residential Stamp Duty (NRSD) introduced since November 2016 (…) is a residency-based capital flow management measure and a macroprudential measure (CFM/MPM) levied at a higher rate on non-residents than on first-time resident home buyers. Therefore, staff recommends phasing it out once systemic risks from the non-resident inflow dissipate.

Authorities’ Views

The authorities agreed that increasing land supply remains the key to fundamentally resolving the structural imbalance between housing demand and supply. They emphasized that various measures had been taken to boost land supply for housing production, including by accelerating land resumption and expediting and streamlining the process of land production, and such efforts were starting to bear fruits. The authorities viewed the current tight macroprudential stance for housing market as appropriate given the elevated house prices, while noting that they will continue to closely monitor the housing market and stand ready to make necessary adjustments with a view to safeguarding financial stability. They noted that mortgage lending by non-banks has been closely monitored and has declined in recent years amid the authorities’ efforts to regulate banks’ lending to non-banks and the expansion in the mortgage insurance program.”

Posted by at 6:53 AM

Labels: Global Housing Watch

Subscribe to: Posts