Wednesday, August 7, 2019

House Prices in Latvia

From the IMF’s latest report on Latvia:

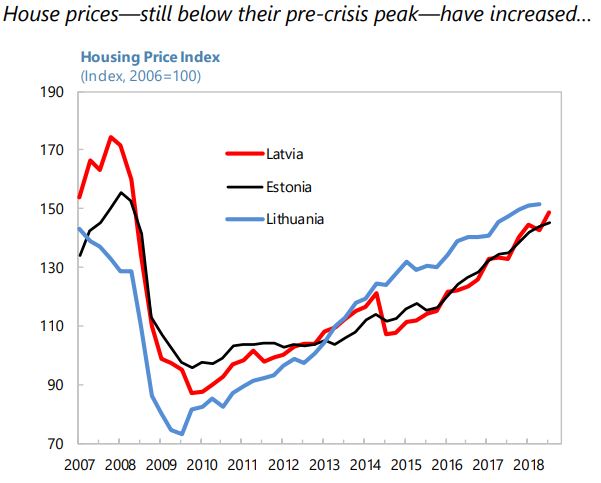

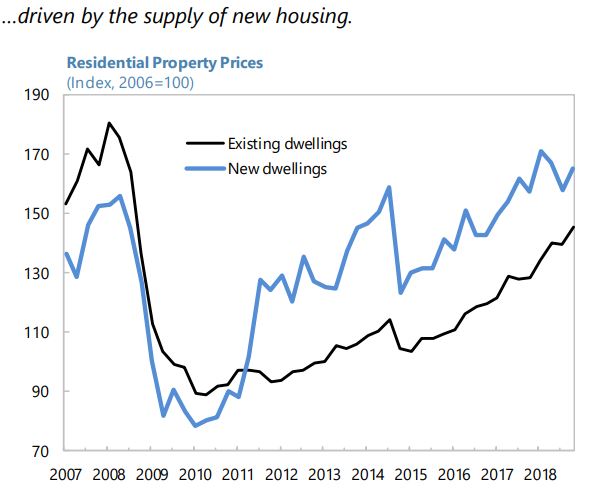

“The rapid rise in property prices merits attention. Despite a shrinking population, real house prices have increased by more than 7 percent per year over the last three years due to a surge in construction costs and prices of new dwellings. Current valuation indicators (price-to-income and price-to-rent ratios and deviations from long-term fundamentals) signal potential vulnerability to overvaluation of housing prices over the medium term. Yet, there are no acute financial imbalances, as the house price index is still about 20 percent below its pre-crisis peak in 2008, and aggregate house price developments have not been spurred by credit growth. Outstanding mortgage loans have dropped below 20 percent of GDP at end-2018, far below the euro area average of about 38 percent of GDP.

Timely adoption of precautionary macroprudential measures can help contain medium-term balance sheet risks. The high share of variable rate mortgages raises the risk to debt service capacity if household leverage increases, while a slowing wage growth could reduce debt affordability. BSFCs’ re-orientation may also result in a deterioration of borrower quality if they loosen credit standards and increase household lending to maintain profitability amid falling margins. Latvia’s macroprudential measures are relatively lenient compared to those in other EU countries and could be preemptively adjusted. Lowering the current LTV ratio limit of 90 percent to 80 percent (closer to other European peers) for residential mortgage lending, imposing restrictions on home refinancing, introducing a debt service-to-income (DSTI) limit, and limiting the maximum maturity of mortgages and consumer loans would mitigate vulnerabilities related to real-estate exposures. Higher provisions for loans with LTV ratios above the limit and regular assessments of collateral valuation standards would prevent excessively risky lending. Finally, macroprudential measures should apply to leasing companies to prevent potential regulatory arbitrage between them and banks.”

Posted by at 9:50 AM

Labels: Global Housing Watch

Subscribe to: Posts