Wednesday, May 9, 2018

Low Inflation in Asia

From the new IMF Regional Economic Outlook for Asia Pacific:

“The main findings are as follows:

- Recent low inflation has been driven mainly by temporary forces, including imported inflation. Phillips curve estimation indicates that weaker import prices, including low commodity prices, contributed to half of the undershooting of inflation targets in advanced Asia and most of the undershooting in emerging Asia in recent years. In addition, China seems to have played an important role in driving both global and regional inflation. More generally, an analysis looking at temporary and trend components suggests that temporary shocks have accounted for the bulk of the recent reduction in inflation.

- The inflation process has become more backward-looking. While inflation expectations are generally relatively well anchored, especially in advanced Asia and in economies with inflation-targeting frameworks, the importance of expectations in driving inflation has declined in recent years with past inflation playing a larger role.

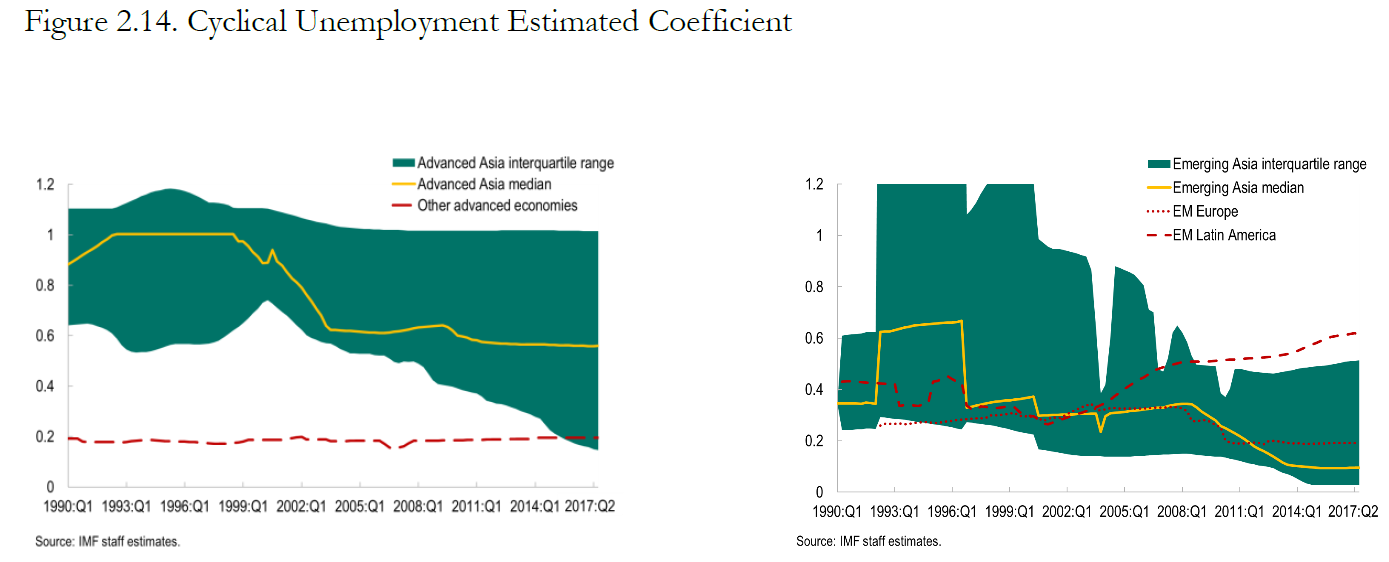

- The sensitivity of inflation to the unemployment gap has declined. There seems to be a flattening of the Phillips curve compared to the 1990s in advanced Asia and a similar but more continuous flattening in emerging Asia. Outside of Asia, the slope of the Phillips curve seems to have been more stable.”

“The main policy implications of the findings are:

- Central banks should be vigilant in responding to early signs of inflationary pressure, including from global factors. A sudden increase in inflation may then persist, and disinflating may be costly if sensitivity of inflation to the unemployment gap has declined.

- It will be important to strengthen monetary policy frameworks and improve central bank communications in order both to increase the role of expectations in driving inflation and to maintain expectations anchored to targets.

- To mitigate the role of imported inflation, exchange rates should be allowed to adjust more flexibly.

- In principle, the monetary policy response to commodity price shocks should be to accommodate first- round effects but not the second-round effects.”

Posted by at 3:38 PM

Labels: Inclusive Growth

Subscribe to: Posts