Wednesday, September 16, 2015

Rising House Prices and Household Debt: A Twin Boom in Norway?

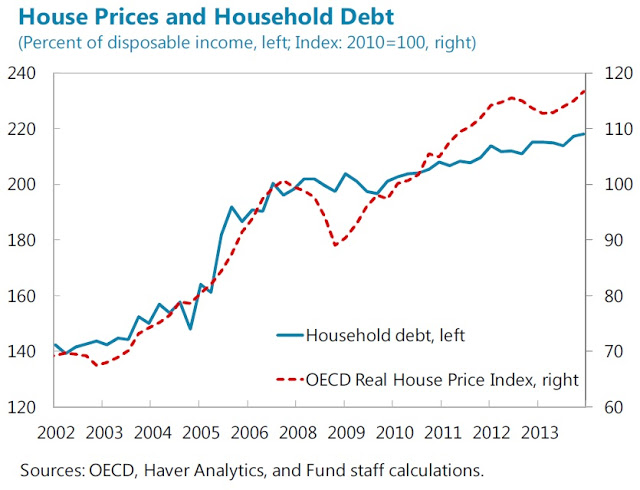

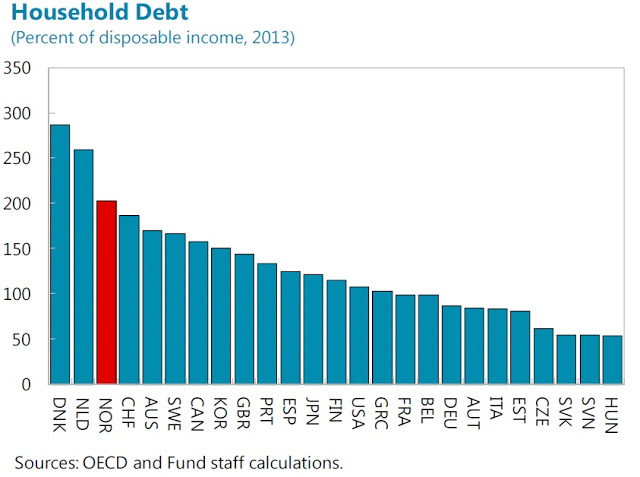

“The Norwegian housing market was only moderately affected by the global financial crisis, and the rising trend of house prices resumed shortly after the crisis. In the meantime, household debt reached more than 200 percent of disposable income, and it is expected to grow further”, a new IMF paper examines the characteristics of household debt and the factors driving the housing boom and debt accumulation. The paper also examines the potential macroeconomic impact of a possible house price correction. Read the report here.

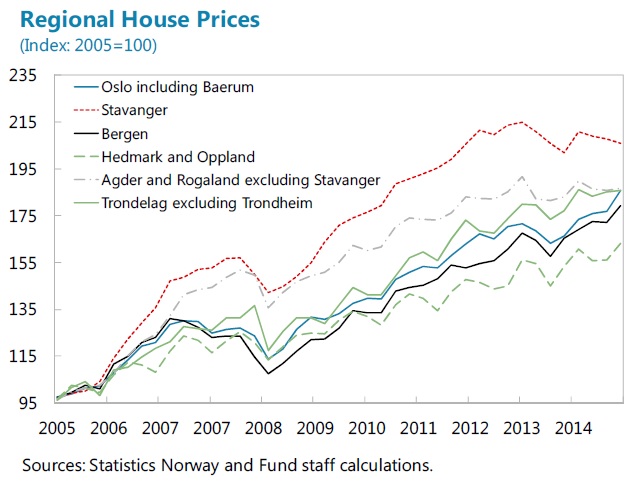

Moreover, a second report, notes that “House price developments vary considerably across regions, with the Oslo area recording relatively more robust price growth while the Stavanger area where petroleum activity is concentrated showing more subdued growth. (…) most estimates suggest that house prices are significantly overvalued.”

Finally, a third report takes a look at what could be the impact of a decline in house prices on the financial system. The report notes that “Stress tests suggest that under severe macroeconomic shocks banks and life insurers could face important but manageable capital shortfalls. A combination of severe shocks—including protracted low oil prices and a sharp contraction in house prices—could result in an aggregate capital shortfall for banks of up to 4.6 percent of GDP over five years.”

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts