Saturday, May 30, 2015

House Prices in Switzerland

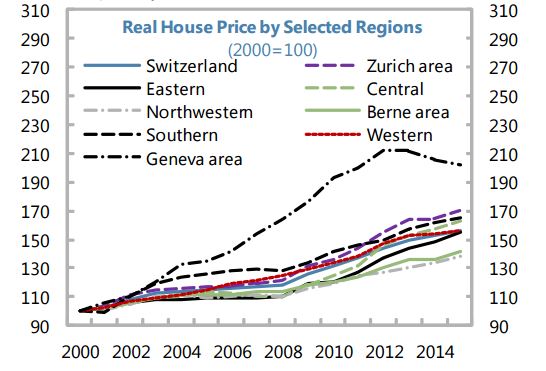

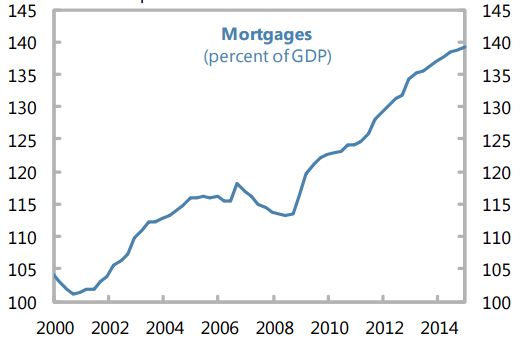

On the measures taken by the Swiss authorities, the report points out that the “(…) Swiss authorities have undertaken various prudential measures over the last three years aimed at reducing housing-related risks. Swiss household debt (mainly mortgages) is high by international standards, and mortgage debt has been rising steadily since 2008, in tandem with a buoyant housing market (…). To reduce related financial stability risks, the authorities have undertaken a number of prudential measures, including strengthened bank “self-regulation” standards approved by FINMA, effective September 2014 (…). These measures appear to have had some effect, as housing and mortgage markets show some signs of cooling. The growth rate of residential real estate prices has eased both for owner-occupied apartments and single family houses, including in areas, such as Lake Geneva, that previously saw rapid house price growth (…). Mortgage growth has also decelerated, although this effect is less pronounced (…). Similarly, price-to-rent and price-to-income ratios have started to stabilize (…). The percent of new mortgages for owner-occupied real estate with loan-to-value ratios exceeding 80 percent have also been on a declining trend. As the authorities have taken a range of measures to address the risk of a build-up of imbalances in the housing and mortgage markets, it is difficult to clearly disentangle which have been the most effective. However, the consensus view among the authorities and banks was that the required down payment from the borrower’s own funds (not funded by using pension savings) has perhaps been the most important measure.”

Posted by at 6:23 PM

Labels: Global Housing Watch

Subscribe to: Posts