Thursday, January 16, 2020

House prices in Finland

From the IMF’s latest report on Finland:

“Finnish banks are highly exposed to real estate, but residential and commercial real estate markets are not obviously overvalued. The exposure of domestic banks to real estate market has grown significantly over the last 20 years. The total volume of credit issued by domestic banks to the real-estate and construction sectors stood at 48.5 billion euros in 2018 (above 20 percent of GDP and 50 percent of banks’ receivables from firms and housing corporations), but rates of non-performing real estate loans remain low. In addition, real estate markets do not seem overheated overall, although there are differences across regions and market segments:

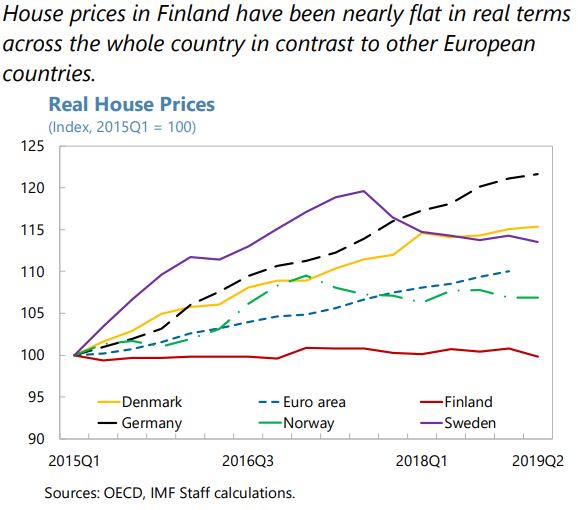

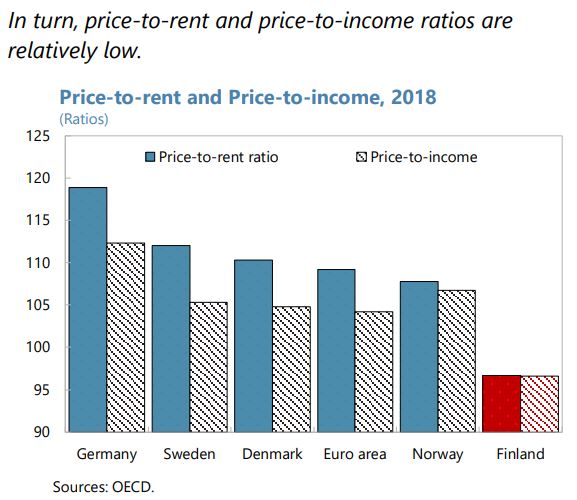

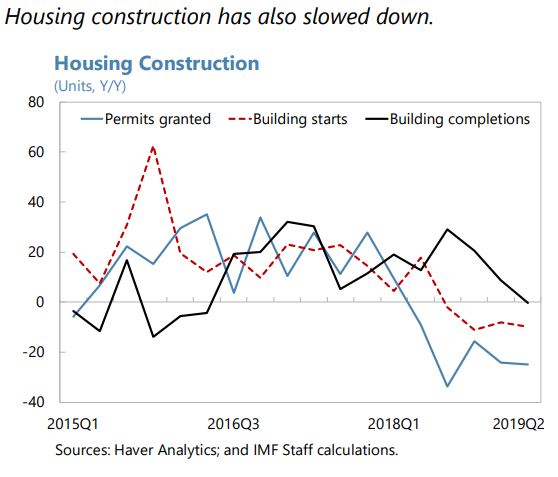

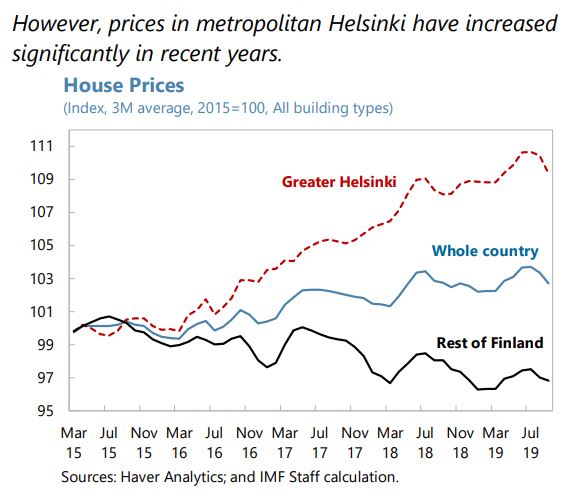

- Residential real estate prices have been nearly flat in real terms across the whole country, priceto-income and price-to-rent ratios are relatively low, and construction of new housing units seems to be slowing. However, housing prices in the Helsinki region have increased steadily while in most other parts of the country prices are falling (…).

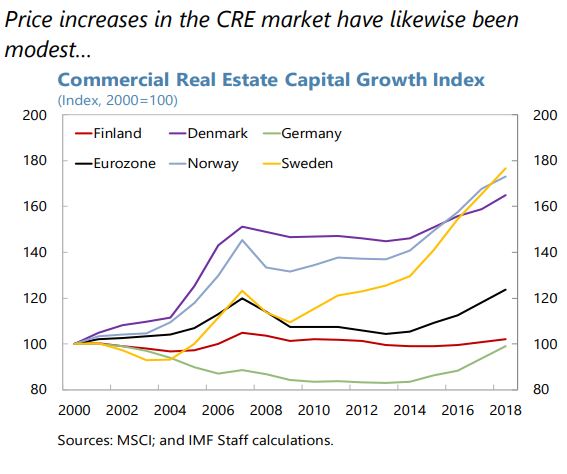

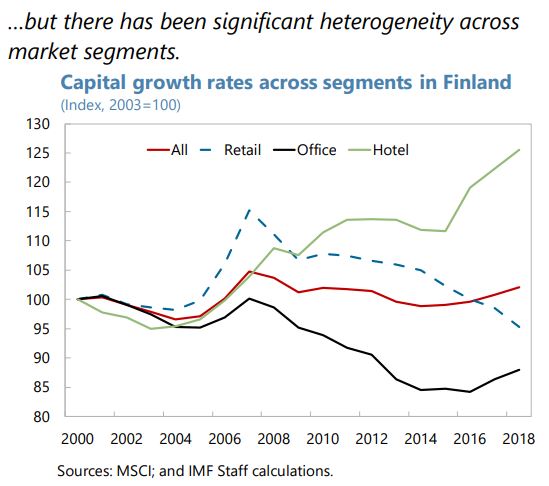

- Commercial real estate (CRE) valuations also do not appear stretched overall, but aggregate price dynamics mask significant differences across regions and submarkets. In the prime Helsinki office segment, limited supply means that rents are increasing, but they remain below the levels observed in other European capitals. By contrast, prices of retail properties have declined, given the brisk pace of growth in e-commerce and new supply in the Helsinki area. There are ongoing efforts to collect more data for a more precise assessment of CRE-related vulnerabilities in the financial sector, but data to monitor developments in CRE markets remain insufficient.

However, the increase and the composition of household debt create borrower-side vulnerabilities. While the debt-to-income ratio remains far below that of Denmark, Norway and Sweden, it has increased in recent years, driven by large annual increases in consumer credit and housing company loans. The share of highly indebted households is also elevated relative to levels observed in the past (although it has been stable in recent years). One concern is that financing the purchase of real estate through shares in a housing company masks risks to home owners and can make higher prices appear more affordable than they truly are.10 In addition, the majority of housing loans carry variable rates.

The authorities are taking steps to address these weaknesses. In particular, a government appointed working group has recommended a comprehensive cap on the debt-toincome (DTI) ratio, limits on the indebtedness of housing companies, and shortening the maximum maturity of mortgages and housing company loans. Crucially, the DTI limit would cover all borrower’s debts, including housing company loans. The working group proposes that the DTI limit be 450 percent; anticipating cases in which higher leverage could be affordable for some borrowers, it also proposes an exemption to allow banks a share of borrowers with higher debt ratios. These would be significant improvements and also in line with recent recommendations by the European Systemic Risk Board. The parliamentary discussions on these proposals are set to begin in 2020. In addition to the working group recommendations, an electronic registry of housing company shares is scheduled to be operational by the end of 2022. The registry will include full ownership information and will therefore make it easier to assess risks of investing in housing companies.”

Posted by at 9:44 AM

Labels: Global Housing Watch

Subscribe to: Posts